GBP/USD Summary

GBP/USD’s rally has largely tracked stronger UK data relative to the US, but with expectations reset and key events ahead—including U.K. inflation, the BoE and Fed—the risk of reversal is building. Momentum is fading, and sterling may soon face a turning point.

Divergent Data Surprises Underpin Stirling Rally

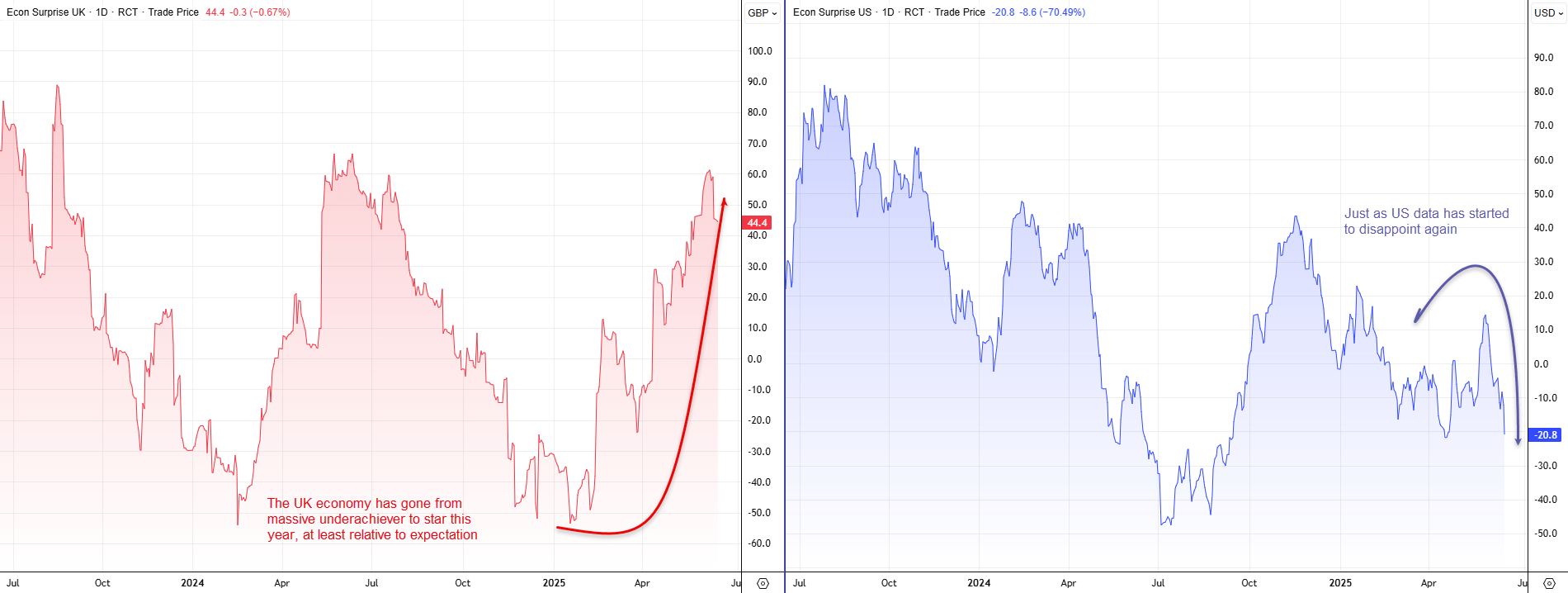

While unpredictable foreign policy is often cited as a factor behind recent weakness in the U.S. dollar, when it comes to GBP/USD, a sizeable part of the rally this year can be explained by economic performance relative to expectations. The first chart bolsters that view, showing Citi’s economic surprise indices for the U.K. in red and the U.S. in blue. If you haven’t come across this indicator before, it tracks how economic data prints relative to economist expectations. It gives greater weight to more timely data to provide a measure of positive or negative economic surprises.

Source: LSEG

A positive reading—such as the U.K. right now—indicates most indicators are topping expectations. A negative reading—as we see for the United States—points to most data undershooting on the downside.

Following a horrible end to 2024, data in the U.K. has improved noticeably compared to expectations this year, the exact opposite of the U.S. When you then take a glance at the GBP/USD chart over the same period, it’s almost a mirror image, with the pound continuing to strengthen against the dollar.

But will that continue now that expectations for both economies have been reset? One thing the U.K. measure shows is that economic beats of this frequency rarely last long. Nor has U.S. data underwhelmed for lengthy periods of time coming out of the pandemic era. That alone should have markets on alert for a potential reversal of the moves seen this year—an outcome that may work against continued GBP/USD upside if it were to play out.

U.K. Inflation Pulse in Focus

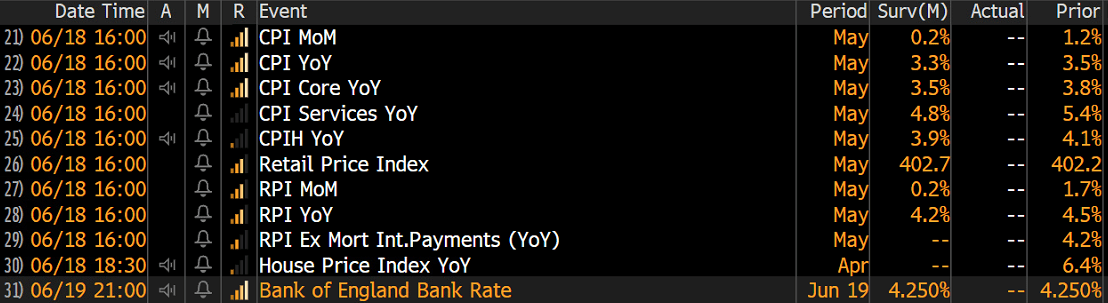

Traders won’t have to wait long to see the next set of U.K. data hit the wires, with key inflation figures released on Wednesday just before the Bank of England (BoE) announces its June monetary policy decision on Thursday.

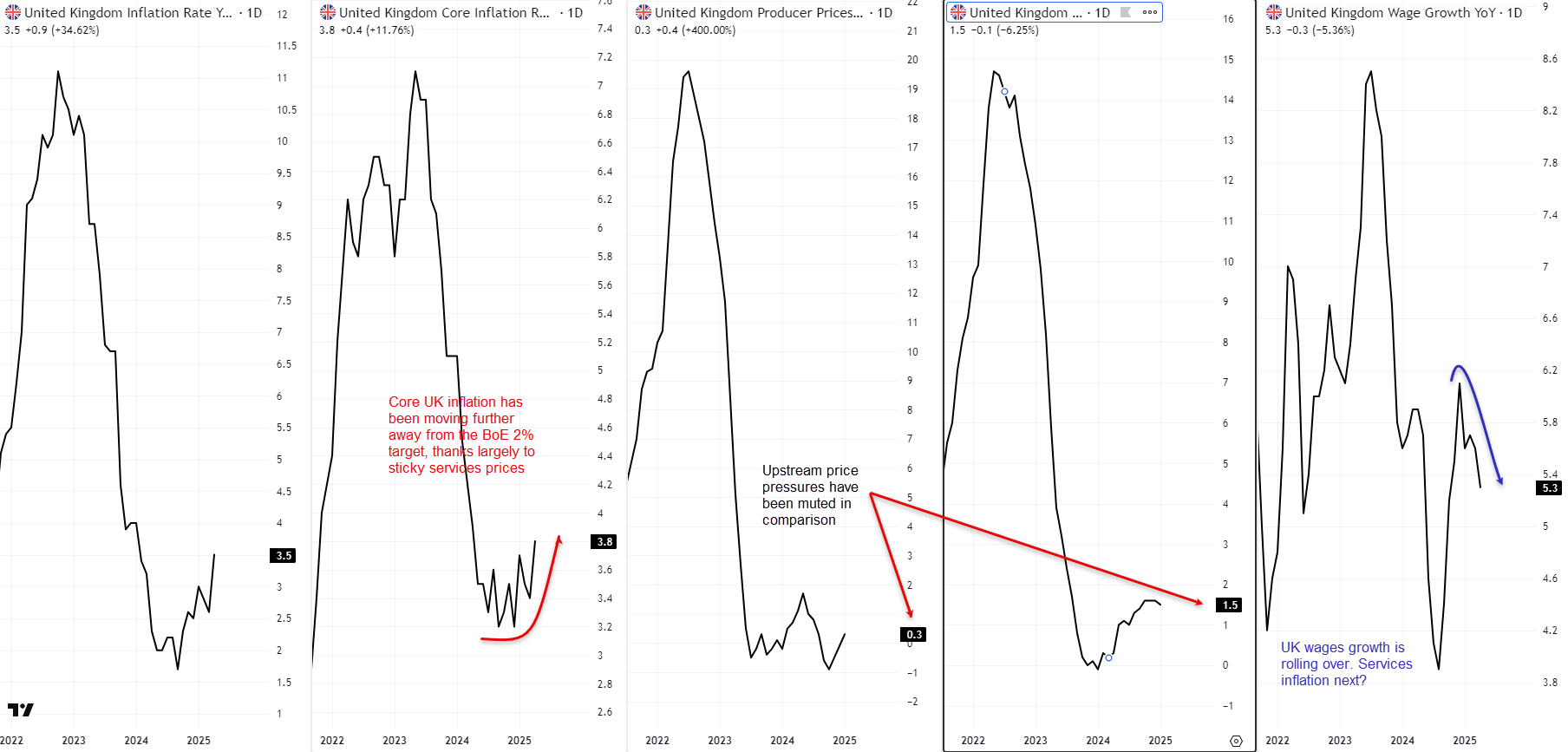

One thing that’s been persistent in the U.K. economy in recent years is sticky inflationary pressures, especially for services prices which can be heavily influenced by wage growth. Even though upstream inflation has been soft, for prices linked more to the domestic economy, upside pressures have been relentless, with annual wages growth topping 5%+ for over half a year. That’s seen core consumer prices—which strip out food and energy—lift 3.8% in the 12 months to April, nearly double the BoE’s 2% target. Services prices—which account for most of the U.K. inflation basket—remain far above 5%.

Source: TradingView

However, downside risks for services inflation may be brewing with wages growth decelerating noticeably in the latest figures for May. Given the linkages between the two, markets see services inflation easing to 4.8% in May, down from 5.4% in the 12 months to April. As such, core inflation is forecast to step down to an annual pace of 3.5% over the same period—still far too hot, but an improvement nonetheless if realised.

Source: Bloomberg

Inflation Detail to Impact BoE Rates Outlook

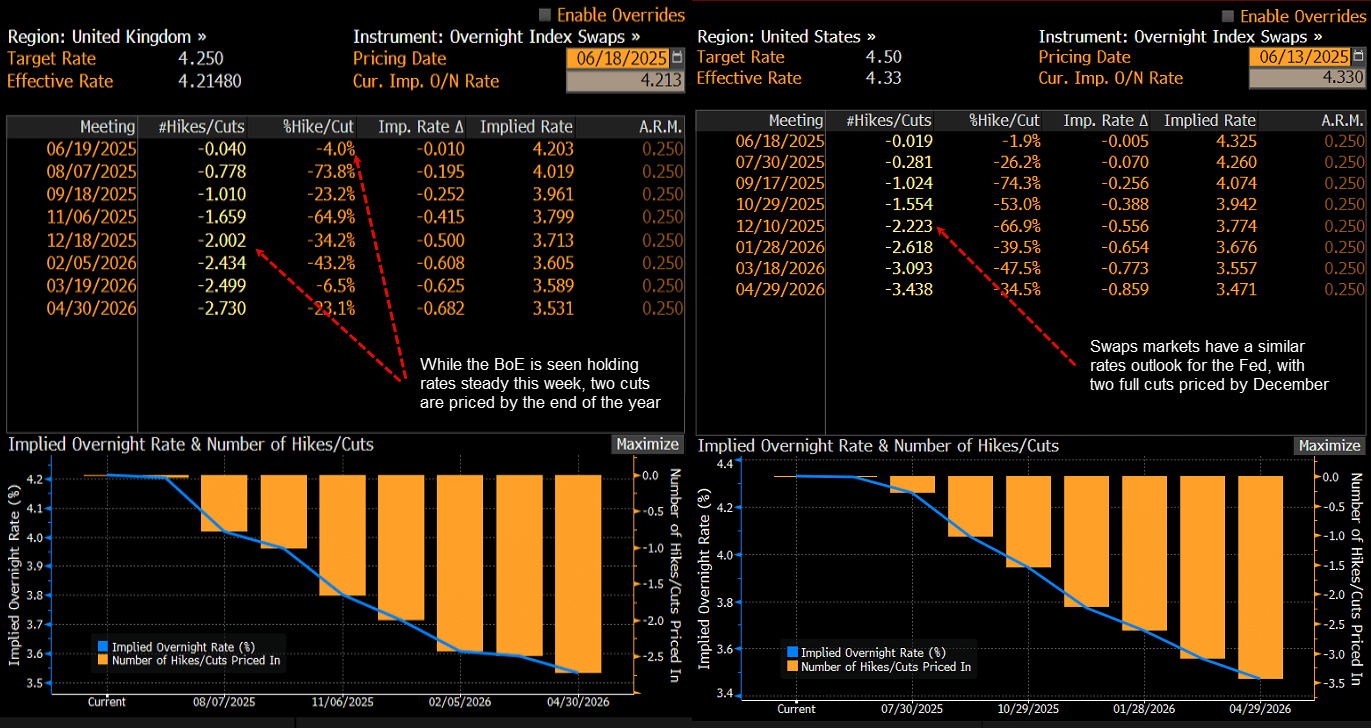

Depending on the details, the data could influence market timing for the next rate cut from the BoE. While another move on Thursday is deemed the longest of long shots at just 4%, a full 25bp move is priced by September, with a second expected by December. The May inflation print has the power to shift those expectations forward or back, and influence whether the BoE may be forced to shift policy settings into outright stimulatory territory beneath 3%.

Source: Bloomberg

Complicating matters for GBP/USD traders, the Federal Reserve’s FOMC rate decision for June will be released between the U.K. inflation report and BoE announcement, creating an environment conducive to volatility—even before Middle Eastern tensions are considered.

As discussed in a separate note, markets are confident the Fed will leave policy rates unchanged in a range between 4.25–4.50% on Wednesday, with two cuts priced by year-end. That means the performance of the USD will be driven by what Fed officials signal when it comes to the rates outlook, outside of a shock move.

Most recent commentary has focused on hawkish risks that may see the median Fed forecast trimmed from two to one 25bp cut this year, citing inflationary threats stemming from higher import tariffs and energy prices.

While such a view seems fundamentally sound, it ignores the wave of inflation undershoots seen in the United States recently, including during the period since higher tariffs were introduced. Sure, the influence on prices may yet be seen, but there was scant evidence in the latest producer price inflation or import price data to suggest an imminent inflationary pulse is heading toward consumers.

With U.S. labour market conditions showing signs of softening, limiting the inflationary threat from accelerating wage pressures, it seems far more likely the Fed will continue to signal two cuts this year rather than turning hawkish. The breakdown of individual forecasts will also be interesting—don’t be surprised to see a greater dispersion in views compared to three months ago, including a potential tilt towards an imminent resumption of the easing cycle, given activity does not scream the need for restrictive policy settings right now.

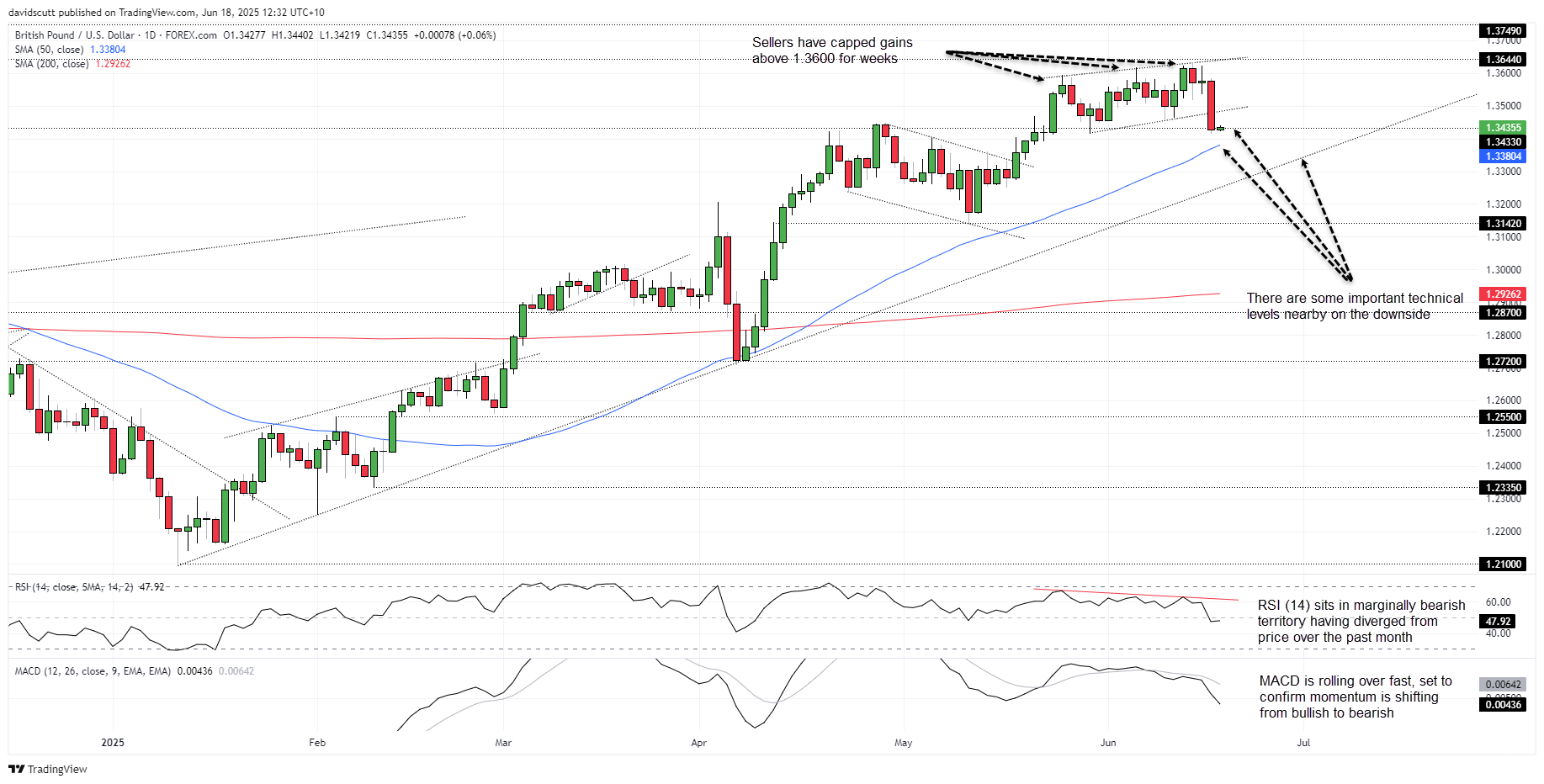

GBP/USD Tumbles as Event Risk Ramps

Source: TradingView

Heading into this cluster of major market events, GBP/USD was hammered on Tuesday, breaking out of the rising channel it had been trading in over the past month, eventually finding support beneath 1.3433—a level it has done ample work either side of over recent years.

With bearish divergence between price and RSI (14) now resolved, and with the latter sitting beneath 50, the bullish momentum picture is quickly shifting from neutral to borderline bearish. MACD remains in positive territory, but having already crossed the signal line from above, it too looks like it may soon confirm the bearish tilt.

Outside of big figures which GBP/USD tends to gravitate towards within a broader trend, downside levels to watch include the important 50-day moving average, January 2025 uptrend, along with horizontal support at 1.3142. A breach of the latter would increase the risk of a venture beneath 1.3000 towards more substantive support levels, including the 200-day moving average.

On the topside, former channel support may now revert to offering resistance. Above, sellers have been parked above 1.3600 for weeks, with the March 2022 double-top of 1.3644 another level of note.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

September 18, 2025 02:48 PM

June 23, 2025 01:22 PM

June 23, 2025 10:39 AM

June 20, 2025 05:23 PM

June 20, 2025 04:46 PM

June 20, 2025 03:35 PM

February 10, 2025 08:45 PM

February 1, 2025 02:00 AM

January 1, 2025 07:30 AM

December 23, 2024 02:45 PM