US futures

Dow futures -0.4% at 42800

S&P futures -0.15% at 5898

Nasdaq futures -0.4% at 21376

In Europe

FTSE 0.99% at 8770

DAX 0.66% at 24064

- Stocks hold steady amid a quiet economic calendar

- Moody’s cut the US credit rating

- US debt in focus ahead of Trump’s tax cut vote this week

- Oil steadies amid multiple influencing factors.

Stocks are muted ahead of Fed speakers.

U.S. stocks are heading for a quiet open as investors await further commentary from Federal Reserve officials to assess the potential impact of Trump's tariffs in the coming months.

Seven Federal Reserve officials are due to speak later today. The market is currently expecting two 25 basis point rate cuts from the US Federal Reserve this year.

Yesterday, Fed officials highlighted the ramifications of Moody's credit rating cut and uneasy market conditions. While stocks initially fell and government bond yields jumped as investors considered the implications of Moody's downgrade, the main indices ended the session modestly higher.

However, concerns surrounding the mounting U.S. debt pile remain in focus, particularly with a vote on Trump's sweeping tax cut bill in the House of Representatives expected this week. Some economists warn that such a bill could add $3 to $5 trillion to the deficit.

U.S. stocks have recovered sharply from the April low, when markets were hit hard by Trump's Liberation Day reciprocal tariffs. Opposing tariffs, a tariff reduction between the US and China, and some weaker-than-expected inflation data have helped the market recover.

The US economic calendar is quiet. PMI figures are due on Thursday.

Corporate news

Home Depot is rising 2% after the world's largest home improvement retailer posted Q1 results that exceeded revenue expectations, although they fell short on earnings. The firm reiterated its full-year outlook.

Apple is falling after Chinese shipments of the flagship iPhone and other mobile devices fell in April to the lowest level since 2011. This could be a sign of the impact of trade tensions between the US and China.

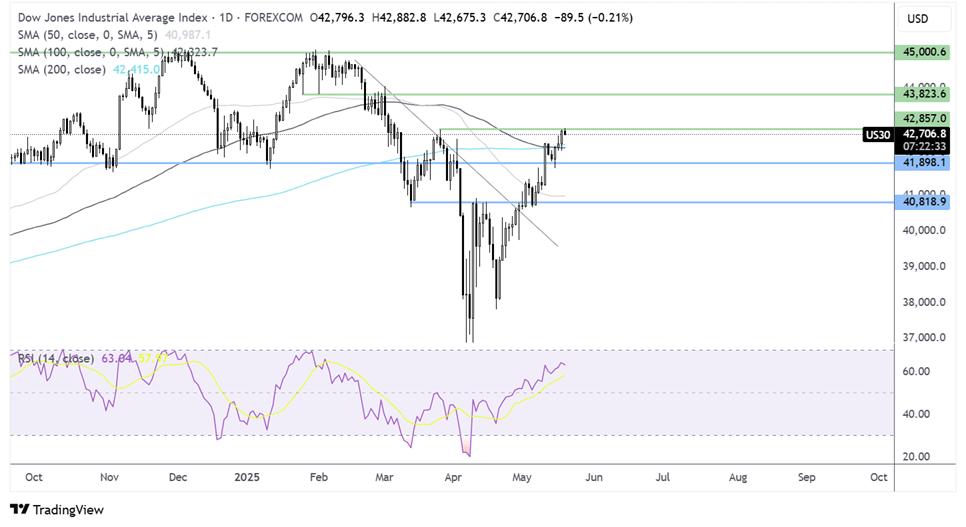

Dow Jones forecast – technical analysis.

The Dow Jones has recovered from the 36,550 low, rising to 42,900, its highest level since early March. The rise above the 200 SMA and the RSI above 50 keep buyers hopeful of further gains. Buyers will look to rise above 43,000, to extend gains towards 43,850 and on to 45,000. Immediate support is seen at the 200 SMA at 42,415. Below here 42,000 comes into play.

FX markets – USD flat, EUR/USD falls

The USD is flat, holding onto yesterday’s losses amid caution regarding the outlook for the US economy and as investors considered whether US—Japan trade talks would include discussions on FX.

The EUR/USD is falling after yesterday's gains and after Eurozone PPI data showed that inflation at the factory gate level cooled by more than expected -0.9% YoY, adding support to the view that the ECB will cut rates again in June.

GBP/USD is slipping after two days of gains amid a quiet day for economic data as traders continue to digest the EU-UK reset trade deal that was agreed yesterday. The pound is brushing off comments by the BoE chief economist who said that the rate cuts were too fast.

Oil holds steady as investors weigh up multiple factors

Oil prices are steadying on Tuesday amid uncertainties surrounding the US-Iran negotiations and the Russia-Ukraine peace talks.

Some doubts were emerging over whether nuclear talks with the US would lead to an agreement, as Tehran considered a proposal to hold a fifth round of negotiations. Should sanctions be eased, a deal between the US and Iran would raise the latter's oil exports by 300,000 barrels to 400,000 barrels a day.

Meanwhile, Putin has agreed to meet with Ukraine for ceasefire talks immediately; however, a resolution right now looks unlikely.

Separately, decelerating industrial output growth and retail sales in China raised concerns over the oil demand outlook.

Latest market news

Yesterday 06:26 PM

Yesterday 04:30 PM

Yesterday 02:42 PM

Yesterday 12:42 PM

May 22, 2025 01:42 PM

May 21, 2025 01:05 PM

May 20, 2025 01:35 PM