The markets remain largely in a risk-on mode, even though we've had some weaker-than-expected US economic data this week. Yesterday saw both the ADP private payrolls report and the ISM services PMI missed expectations, adding to the disappointing manufacturing PMIs we saw on Monday. The weakness in data has raised hopes for a sooner-than-expected rate cut by the Fed. But it is all about optimism about a potential call between leaders of the world’s two largest economy to resume trade negotiations. Here, in Europe, sentiment remains positive. Earlier, we saw the German DAX hit yet another fresh all-time high, with all eyes are on the ECB, widely expected to cut interest rates yet again—a move that’s been well telegraphed and thus unlikely to jolt sentiment. Sentiment has also been boosted by a stronger-than-feared 30-year debt auction in Japan, providing some welcome calm after recent volatility there. The drop in Japanese yields served to soothe nerves and lent a modest boost to risk assets. The FTSE forecast thus remains positive, with the UK index supported today by a rallying Fresnillo stock, which was shining along with precious metals, with silver breaking $35 for the first time since 2012 – before quickly racing to near the $36 handle – while gold was above the $3400 level again.

ECB set to cut rates but will Lagarde be more dovish thane expected?

Attention now turns to the European Central Bank rate decision tomorrow. A 25 basis point rate cut is expected, but the focus will be on what ECB President Christine Lagarde signals regarding future policy moves. Weakness in Eurozone inflation data has supported equity markets in the region but hasn’t significantly weighed on the euro just yet. The single currency is holding up well today, largely due to the softness in US data, which is putting pressure on the US dollar.

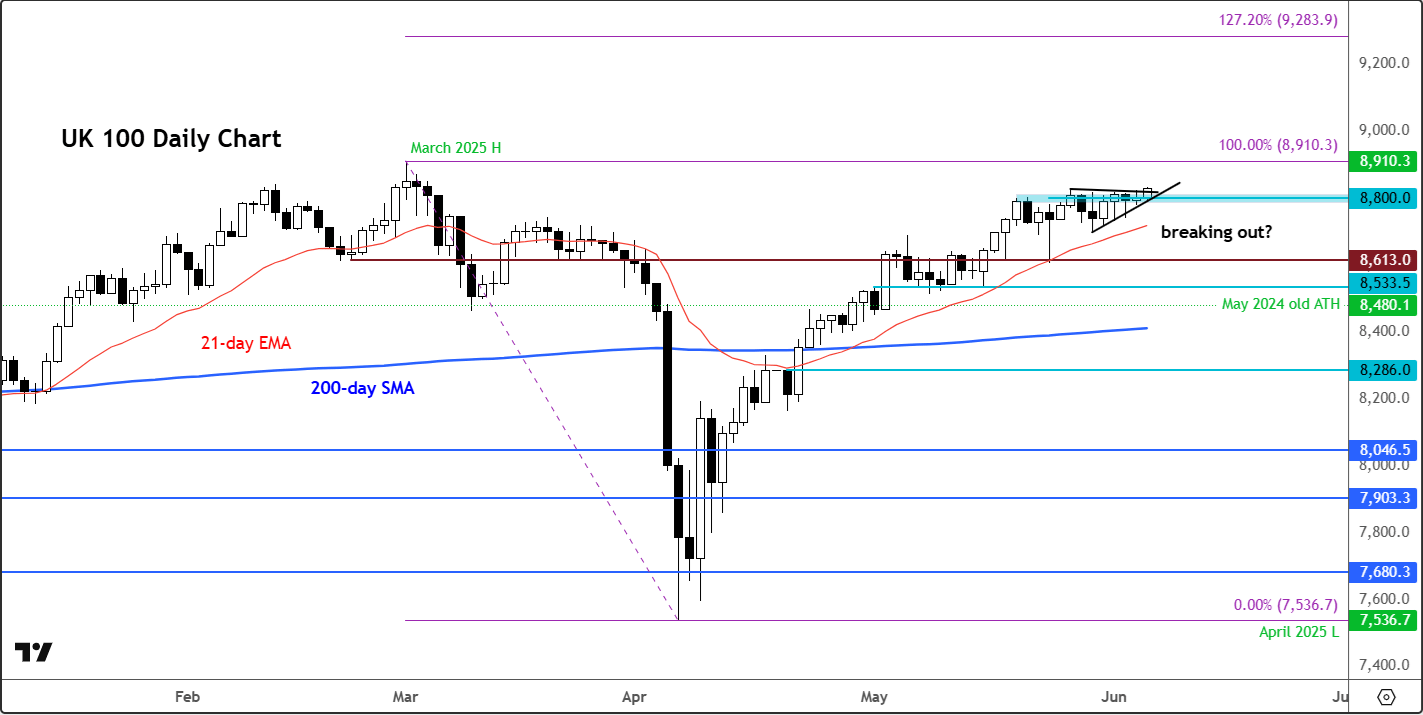

Technical FTSE 100 forecast: break out on the cards?

Global indices like the FTSE 100 are nearly all in the positive territory today, buoyed by optimism that the US and China will resume trade talks and potentially reach an agreement. This optimism is helping to support the FTSE, which continues to consolidate in a tight range, awaiting a possible breakout above its March 2025 high of 8,910. That’s the next key target for the bulls.

Above that, the psychologically important 9,000 level comes into view, and beyond that it’s anyone’s guess how far it might rise. The key question is whether the FTSE can break away from the current congestion zone around 8,810. Based on current price action, it looks like a potential breakout could happen later today or in the next day or two—unless, of course, US-China trade talks collapse and no agreement is reached between the world’s two largest economies.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

September 18, 2025 02:48 PM

June 23, 2025 01:22 PM

June 23, 2025 10:39 AM

June 20, 2025 05:23 PM

June 20, 2025 04:46 PM

June 20, 2025 03:35 PM

February 10, 2025 08:45 PM

February 1, 2025 02:00 AM

January 1, 2025 07:30 AM

December 23, 2024 02:45 PM