USD, EUR/USD, USD/JPY Talking Points:

- Tomorrow brings a quarterly rate decision from the Federal Reserve at which the FOMC will provide updated guidance and projections.

- The big question is whether the Fed is still expecting to cut rates 50 basis points this year as they had last said in their projections in March. Since then, inflation has fallen more than they had expected but labor markets have remained stronger, thereby removing some of the possible motivation to cut. The tariff topic continues to loom large as multiple members of the bank fear of a supply shock, which could lead to higher inflation.

- This is an archived webinar and you’re welcome to join the next live event. Click here to register.

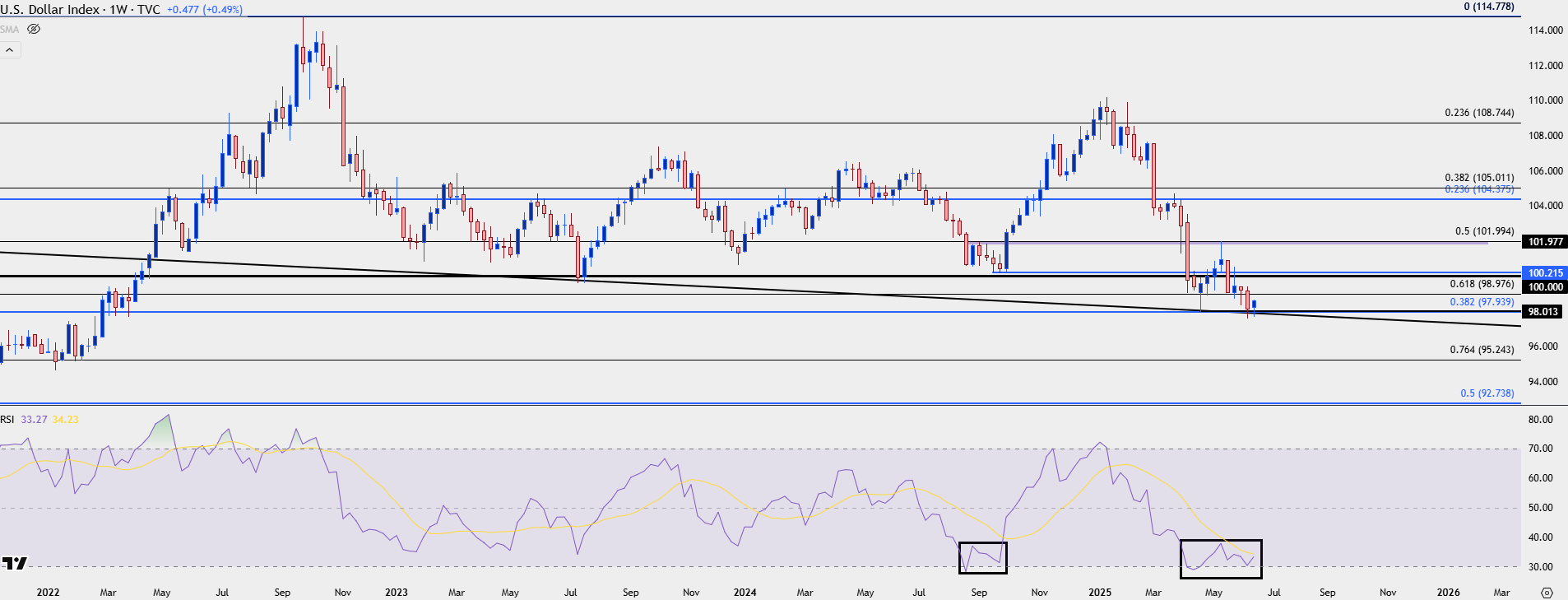

Markets continue to expect the Fed to cut by 50 basis points or more into the end of the year and this pretty much aligns with the bank’s forecasts from the March meeting when they last issued updated projections. With the ECB sounding finished with rate cuts, this has helped to push additional USD weakness as the Dollar has broken down to fresh three-year-lows.

As shown in the video, USD is testing some pretty big support on a bigger picture basis, and the potential for a turn still remains – but for that to come to fruition we’re likely going to need to hear the Fed push rate cut expectations towards 2026 or 2027.

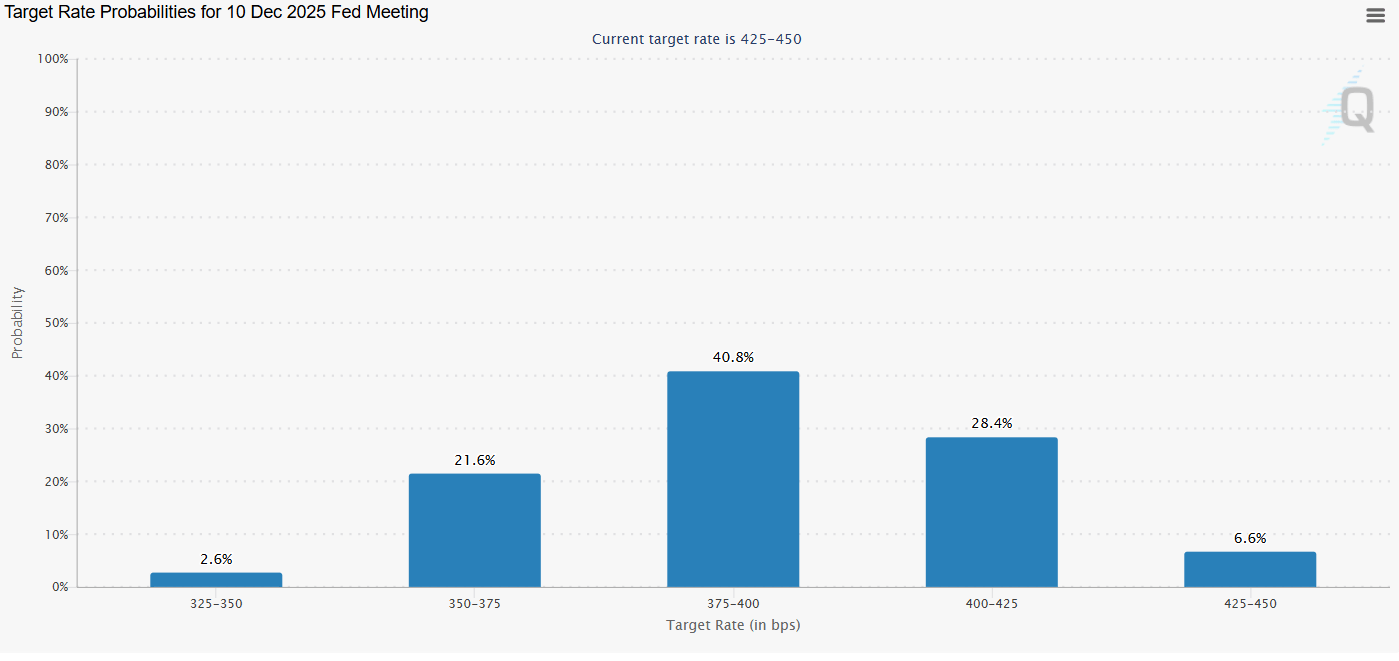

As of this writing, markets are expecting the FOMC to cut rates by 50 basis points by the end of the year to a 65% probability.

Rate Probabilities into End of 2025

Data derived from CME Fedwatch

Data derived from CME Fedwatch

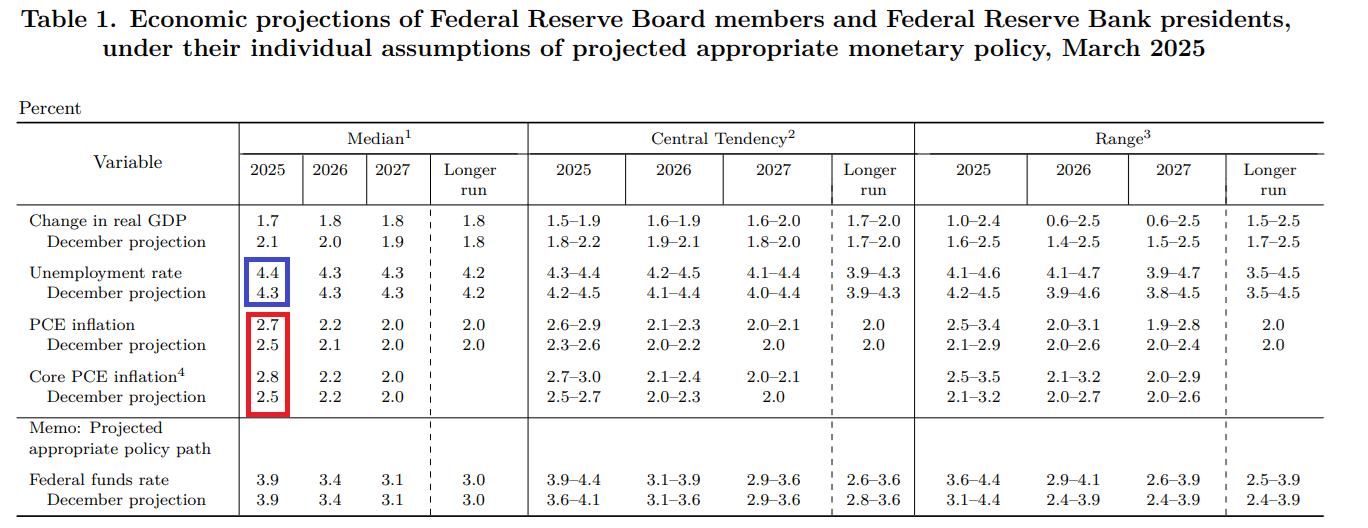

Supporting the argument for FOMC cuts is the fact that inflation is well-below what the Fed was last projecting. In the March update, the FOMC said that they were looking for PCE at 2.7% this year, with Core PCE at 2.8%.

At the last update of that data point the numbers were far below that, with PCE at 2.1% and Core PCE at 2.5%. So, from that perspective, the Fed has an open door to cut rates as inflation isn’t as problematic as they were expecting.

On the other side of the argument, however, the labor market has held up a bit better than they were expecting, with the unemployment rate most recently printing at 4.2% and the Fed was looking for that to go up to 4.4% this year. So, the perceived need for rate cuts isn’t as high as the labor market has held up a bit better.

The outside addition to the argument and something we’ve heard multiple Fed members opine on recently is the impact of tariffs. This has seemed to be an overriding concern around the FOMC as the tariff topic remains a very big part of President Trump’s administration, and while some progress has been made on some fronts, it continues to add a healthy amount of uncertainty to the equation.

So the big question here is whether the Fed forges ahead with their 50 bp expectation for rate cuts this year despite the labor market not looking especially bad, and with the risk of additional inflation as produced by tariffs.

FOMC Data Projections from the March Meeting

Data derived from The Federal Reserve; data derived from Tradingview

Data derived from The Federal Reserve; data derived from Tradingview

USD

The US Dollar is grasping on to some long-term supports and chasing the Dollar lower could be a challenge here. I think for bearish outcomes the Fed would need to lean pretty heavily in setting the stage for rate cuts in September when they next provide updated guidance.

The tariff risk could complicate that but with inflation coming in relatively low and recent dimming of data points like retail sales, this has to be entertained a possibility.

There’s also the USD/JPY element, from which the long-term carry trade continues to drive flows around the USD and I’ll look at that a little lower in this article.

Also of note is the RSI divergence showing on the weekly, where last week’s lower-low on price matches with a higher-low via RSI.

U.S. Dollar Weekly Price Chart

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

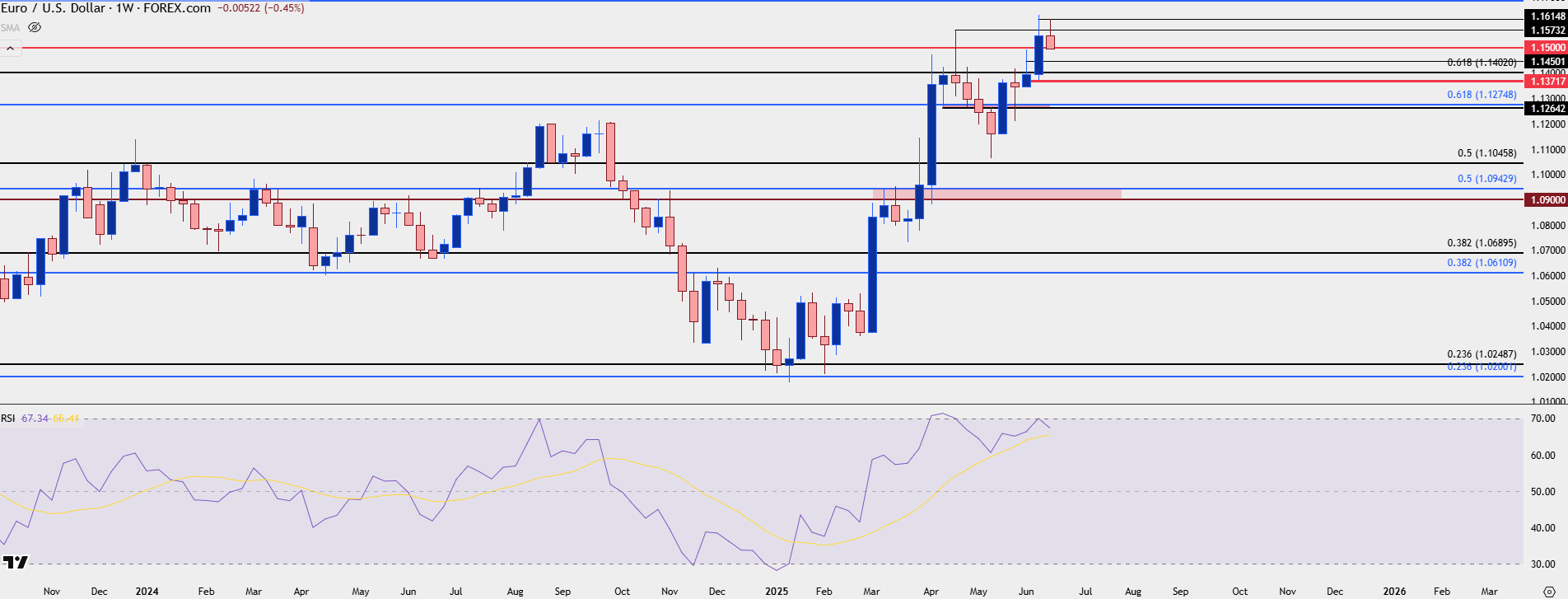

EUR/USD

EUR/USD continues to hold on to short-term bullish price action, and in the webinar I went over scenarios on either side of the matter, highlighting 1.1373 and 1.1275 as supports below the 1.1500 level that’s currently being tested.

Of note, RSI on the weekly has just left overbought territory and the indicator has shown divergence after the prior overbought reading in April.

For USD turns, EUR/USD remains of attraction.

EUR/USD Weekly Chart

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

USD/JPY

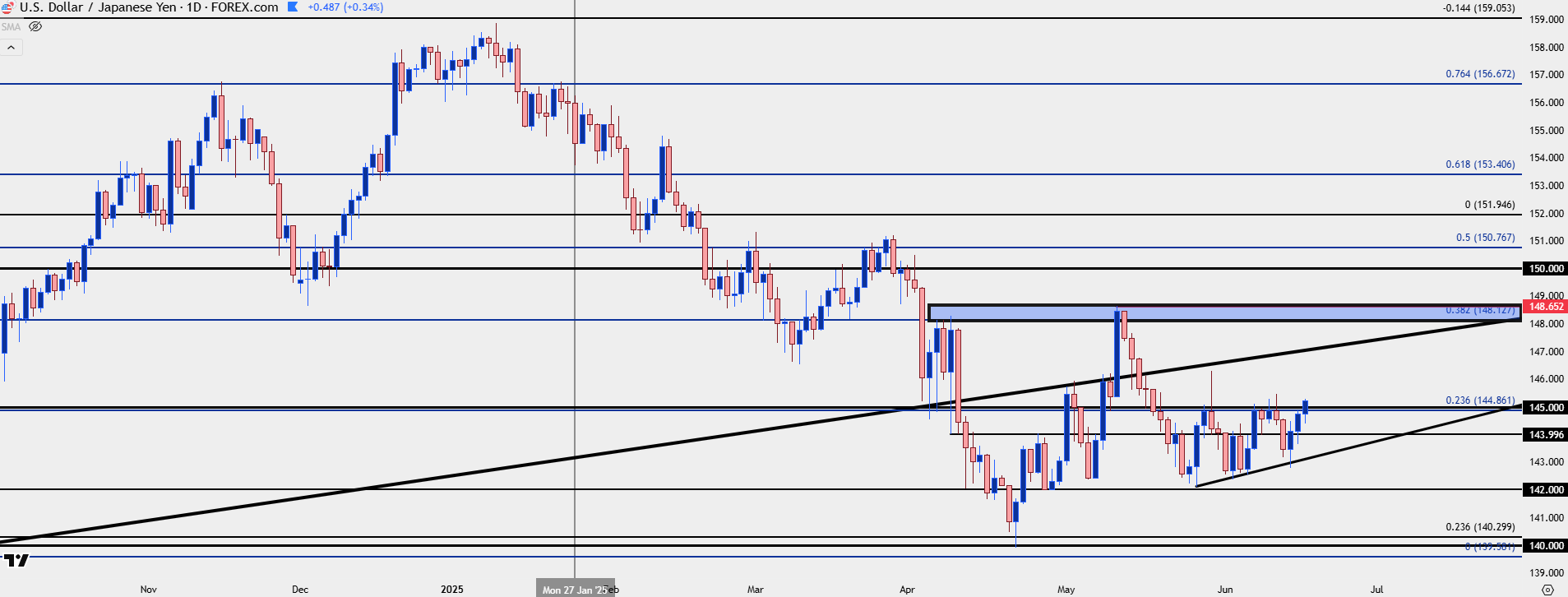

I continue to think that USD/JPY is exhibiting enormous sway over the USD, perhaps more than the 13.6% allocation of JPY in the DXY basket normally would. This dials back to the long-term carry trade and the fact that USD/JPY is still about 40% above early-2021 lows.

The 140 area has held three rigid bounces since December of 2023 and signs of the Fed readying for rate cuts could cause more motivation of unwind as hedges come off. But, if we do see the Fed lean a bit more hawkish, driven by fear of inflation around tariffs, that could produce a short squeeze scenario in both the USD and USD/JPY and that could help to reinforce the USD turn thesis.

USD/JPY is currently pushing through the 145.00 level and that’s been a big spot of late, as looked at in yesterday’s and last week’s articles. Overhead, 145.92 and 146.54 show before the key decision point around the 148.00 handle that caught the highs back in May.

USD/JPY Daily Chart

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

--- written by James Stanley, Senior Strategist

Data derived from

Data derived from Latest market news

September 18, 2025 02:48 PM

June 23, 2025 01:22 PM

June 23, 2025 10:39 AM

June 20, 2025 05:23 PM

June 20, 2025 04:46 PM

June 20, 2025 03:35 PM

June 20, 2025 04:46 PM

June 20, 2025 03:35 PM

June 20, 2025 02:18 PM

June 20, 2025 12:21 PM