US futures

Dow futures 0.06% at 42,094

S&P futures 0.03% at 5880

Nasdaq futures -0.05% at 21220

In Europe

FTSE -0.29% at 8772

- DAX 0.72% at 24182

- Trump postpones EU 50% trade tariff until July 9

- Fed speakers in focus

- Nvidia rises ahead of earnings tomorrow

- Oil holds steady with OPEC in focus

Trump delays EU 50% tariffs until July 9

U.S. stocks are set to open higher on Tuesday, the first day back after the long weekend, as investors cheer President Trump's postponing plans to impose 50% tariffs on the European Union, averting a costly trade war.

On Sunday, Trump said he'd agreed to postpone the steep tariffs on goods from the EU until July 9 following a call with EU president Ursula von der Leyen. The US and the EU will begin serious trade talks amid improving relations between the two regions. These developments brought some relief to the markets, which were unnerved on Friday by Trump threatening tariffs not only on the EU but also on Apple. This sent US indices sharply lower at the end of last week.

The deadline for Trump’s reciprocal tariffs is July 9, and the market is watching closely to see whether close trading partners can reach an agreement in time.

The latest U-turn by Trump highlights the unpredictability of his trade policies, undermining investor confidence in the US.

The market will listen closely to comments from Fed speakers, as well as digest smaller than expected fall in durable goods orders at -6.3% down from 8.6%. Consumer confidence is also due later.

Corporate news

Nvidia is rising 2.5% higher, ahead of quarterly earnings on Wednesday, with investors looking for clues over the impact of US chip curbs on China will cost.

Apple is rising after data showed that US iPhones shipped from India reached 3 million last month, up 76% this year.

Tesla is rising 2.2% despite data showing that European sales nearly halved last month, falling for a fourth straight month amid a backlash against CEO Elon Musk's political views.

Salesforce is rising 1.5% after the WSJ reported that the software company is nearing an agreement to buy Informatica in a deal worth $8 billion.

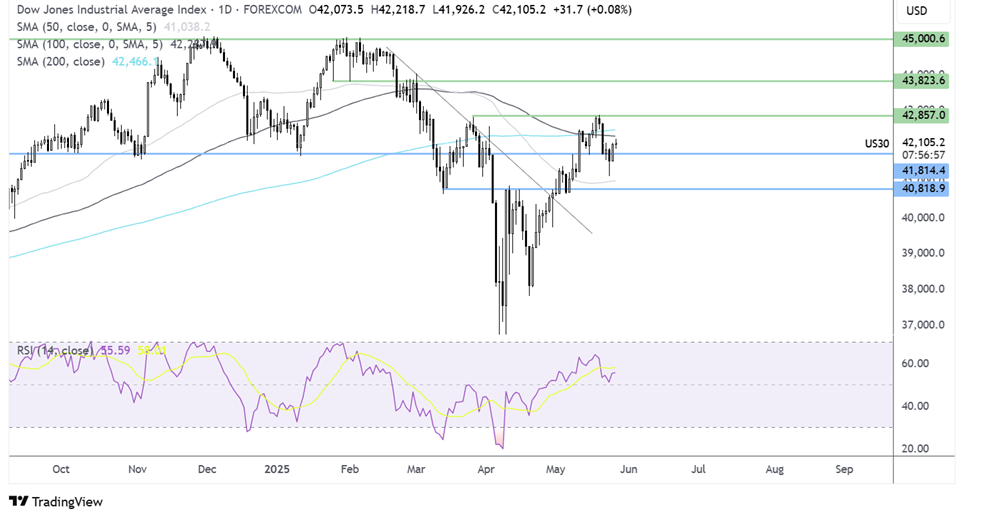

Dow Jones forecast – technical analysis.

The Dow Jones extended its recovery to 42,880 before turning lower, taking out the 200 SMA and spiking to a low of 41,163, before recovering back above the 42,000 round number. This combined with the RSI above 50, keeps buyers hopeful of further gains. Buyers would need to rise above the 200 SMA to bring 42,880 back into focus. A rise above here creates a higher high. Sellers would need to break below 42k and 41,000 the round number and 50 SMA. Below here and 40,880 could see sellers gain traction.

FX markets – USD rises , EUR/USD falls

The USD is rising after last week’s losses and after a long weekend, as the focus shifts to mid-tier data. The improved mood is helping the USD as the EU and the US are keen to progress trade talks.

The EUR/USD is falling amid a stronger USD and after cooler than forecast French CPI will ease to 0.6% YoY, its lowest level since December 2020. The data adds to expectations the ECB will cut rates again in June highlighting the divergence between the ECB and the Fed.

GBP/USD is easing back from a fresh 3-year high reached overnight. Strong retail sales and sticky inflation data last week support the view that the BoE will not cut rates at the coming meeting and will adopt a cautious stance to further cuts until further disinflation is seen.

Oil holds steady with OPEC in focus

Oil prices are little changed at the start of the week after losses last week and amid a cautious mood ahead of the OPEC+ decision on Saturday.

The OPEC JMMC will meet tomorrow ahead of the June 1st full meeting, at which the group will discuss an output hike three times the originally scheduled monthly increase.

The oil cartel is expected to agree to further production increases of 411,000 borrowed barrels per day, which could cap any gains in the oil price.

News that Trump will extend trade talks with the EU until July 9th has eased fears of tariffs suppressing fuel demand, supporting oil prices.

Latest market news

September 18, 2025 02:48 PM

June 23, 2025 01:22 PM

June 23, 2025 10:39 AM

June 20, 2025 05:23 PM

June 20, 2025 04:46 PM

June 20, 2025 03:35 PM

June 18, 2025 07:38 PM

June 18, 2025 03:24 PM

June 16, 2025 03:30 PM

June 12, 2025 04:08 PM