US futures

Dow futures 0.02% at 42,555

S&P futures 0.16% at 5980

Nasdaq futures 0.14% at 21687

In Europe

FTSE 0.3% at 8811

DAX 0.24% at 24202

- US stocks are muted despite weak jobs data

- ADP payrolls rose just 37k

- US ISM services PMI is expected to rise to 52

- Oil rises despite weak China data

Stocks are muted despite ADP payrolls at the weakest level in 2 years

U.S. stocks are rising cautiously higher despite signs of weakness in the US labour market, raising concerns about the Trump administration's erratic trade policies on the economy.

ADP private payrolls showed that just 37,000 jobs were added in May, well below expectations of 120,000, the lowest level in over two years. The data suggests that hiring is losing momentum. However, wage growth remains strong, with annual pay growing at 4.5% for those remaining in the position and 7% for job changes. These levels are little changed from April.

The data comes after job openings unexpectedly increased 7.39 million yesterday, up from 7.2 million.

These figures paint a mixed picture ahead of Friday's nonfarm payroll report.

Meanwhile, ISM services data is expected shortly, and investors will be watching to see whether activity expands to 52 in May, which is in line with expectations, up from 51.6 in April. Any sign of weakness in the data could raise concerns over the economic outlook for the US as businesses struggle to keep up with Trump's erratic trade policies.

On the trade front, yesterday, Trump's doubling of aluminium and steel tariffs came into effect. The market is also waiting for news regarding a phone call between Trump and Chinese President Xi Jinping, which is expected to happen sometime this week.

Corporate news

Dollar Tree is falling 3.1% after the discount retailer declined to lift its full-year guidance, unlike its rival Dollar General, and despite posting stronger-than-expected net sales.

CrowdStrike is falling over 6% after the cybersecurity firm posted revenue guidance for the current quarter that was below expectations. This has overshadowed fiscal Q1 earnings that beat forecasts.

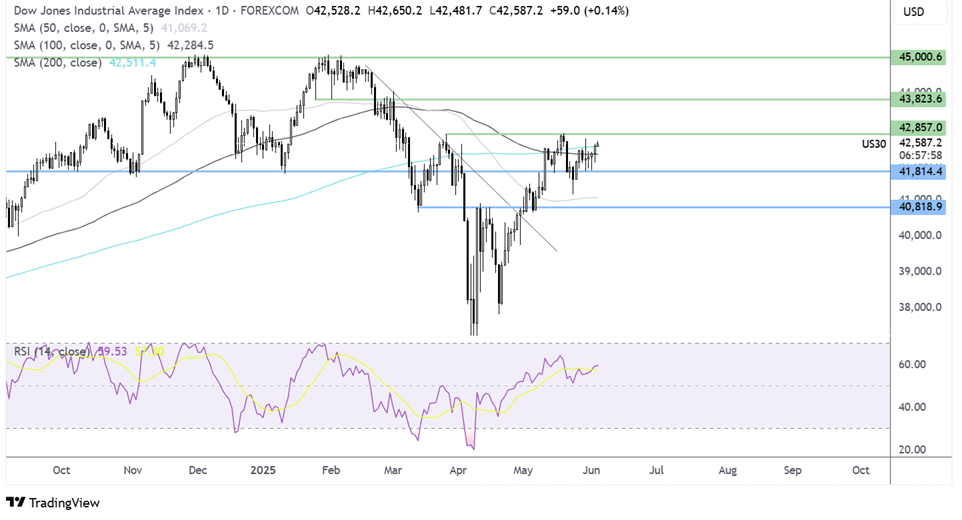

Dow Jones forecast – technical analysis.

The Dow Jones’ recovery has stalled at the 200 SMA at 42,500. A breakout of this dynamic resistance and 42,850 is needed to create a higher high and bring 45,000 the ATH into play. Sellers will need to take out 41,800 to gain traction towards 40,800.

FX markets – USD falls, EUR/USD rises

The USD is falling, giving back some of yesterday's gains after weaker-than-expected jobs data ahead of Friday's closely watched nonfarm payroll report. The weak ADP report offset optimism following yesterday's job openings.

The EUR/USD is rising after the eurozone composite PMI was upwardly revised to 50.2 from 49.5 in the preliminary reading. The services sector PMI fell to 49.7 from April’s 50.1. Gains in the EUR could be limited amid expectations that the ECB will cut rates and then on Thursday.

GBP/USD is my day after the UK services PMI returned to expansion in May. The PMI varies to 50.9, up from 49 in April, and an output revision from 50.2 in the preliminary reading. Concerns over US tariffs are easing, helping support output growth.

Oil holds steady ahead of EIA stockpile data.

Oil prices are holding steady on Wednesday amid global trade tensions open class increases and lower Canadian supply due to wildfires.

While OPEC+'s plans to increase output by 411k bpd are adding pressure to the oil market, this is being offset by a reduction in Canadian production by around 344,000 barrels per day, according to Reuters.

Attention is on Trump and President Jinping, who is expected to speak this week after Trump ramped up rhetorically against China for violating the Geneva deal. The upside in oil prices appears limited given output increases and concerns over the demand outlook.

EIA inventory data is due shortly, and it comes after API inventory data yesterday showed crude stockpiles falling by 3.3 million barrels.

Latest market news

Yesterday 11:00 PM

Yesterday 07:48 PM

Yesterday 06:55 PM

Yesterday 02:00 PM

June 3, 2025 01:56 PM

June 2, 2025 12:32 PM

May 30, 2025 01:37 PM