GBP/USD Summary

GBP/USD traders will soon have to decide whether to extend the bullish move that started in early January, with the pair capped beneath 1.3600 while simultaneously squeezing up against uptrend support. While interest rate differentials and sentiment towards the U.S. fiscal outlook have been factors behind Sterling’s impressive run—emphasising the importance of upcoming top-tier U.S. and U.K. economic data—don’t discount the ability for Thursday’s European Central Bank (ECB) meeting to shake things up.

U.K Economy Perks Up

Relative economic performance has undeniably been a factor behind the rally in GBP/USD this year, as evidenced by the increasingly divergent picture from Citi’s Economic Surprise Index (CESI) for the U.S. and U.K.

Source: LSEG

For those who haven’t come across the index before, it looks at how economic data fares relative to forecast, placing greater weighting on recent data to provide a broader picture of how individual economies are performing versus expectations. It’s useful for traders as this—rather than levels—typically drives market moves. A reading above 0, which the U.K. version is right now, indicates more data than not is surprising to the upside. The opposite applies when the CESI is below 0, as the U.S. is marginally now.

U.K.-U.S. Yield Differentials Widen

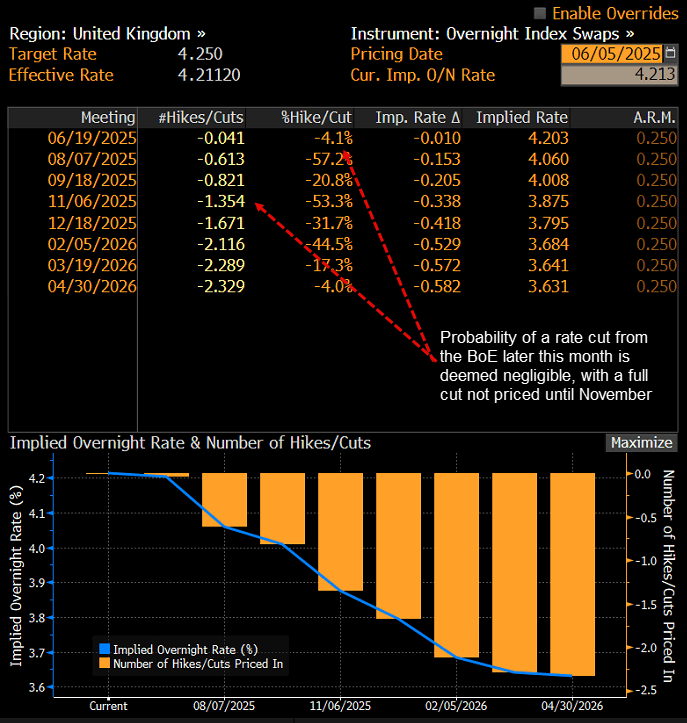

With U.K. data topping forecasts at rates not seen since the middle of last year, pricing for Bank of England (BoE) rate cuts has dwindled. A rate cut later this month is seen as a long shot, with a full cut not priced until November where a second move is deemed a one-in-three chance.

Source: Bloomberg

While not dissimilar to pricing for the Federal Reserve—which looks for two 25bp cuts this year—the direction for pricing has been shifting in opposite directions, helping to push near-dated interest rate differentials in favour of the U.K.

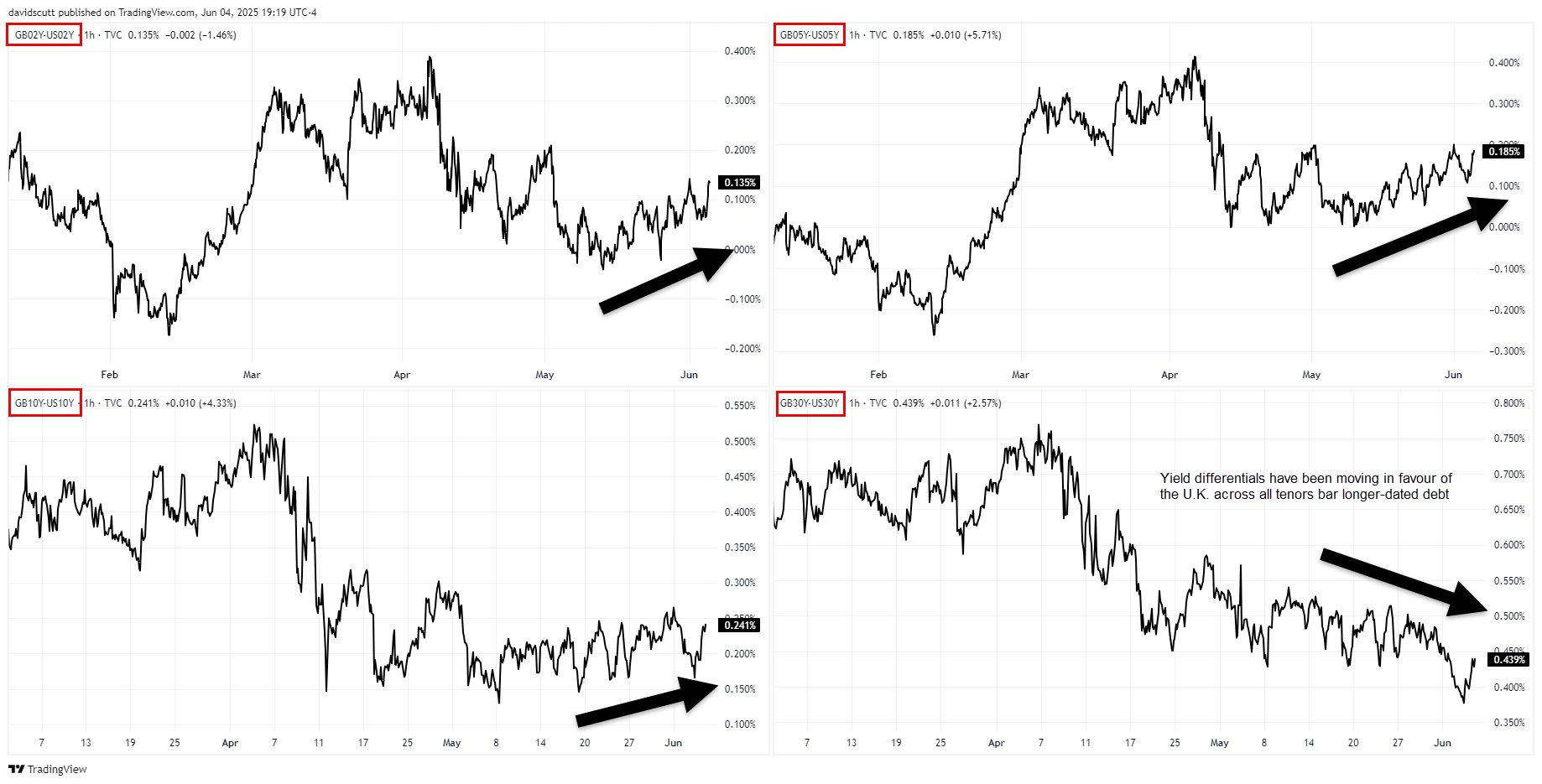

You can see that in the chart below, with yield differentials for two, five and 10-year terms either flipping positive or widening in favour of the U.K. just as the positive domestic data surprises began to lift. While the relationship between yield differentials for two and five-year tenors and GBP/USD has not been overly strong over the past month—sitting with scores of 0.56 and 0.64 respectively—the correlation has been strengthening, hinting that rates have been part of the stronger GBP story.

Source: TradingView

Interestingly, while short-dated yield differentials have moved in favour of the U.K., the opposite applies for 30-year differentials which have shifted in favour of the U.S. While the U.K. has its own fiscal challenges, it suggests concerns about the U.S. budget deficit have played also part in the GBP/USD rally, eroding the appeal of the USD against most major currencies.

Macro Event Risk Lifts

Given the strengthening relationship with yield differentials, volatility in GBP/USD looks set to increase over the next week as we approach what is undeniably the most important part of the month for macro news.

Source: LSEG

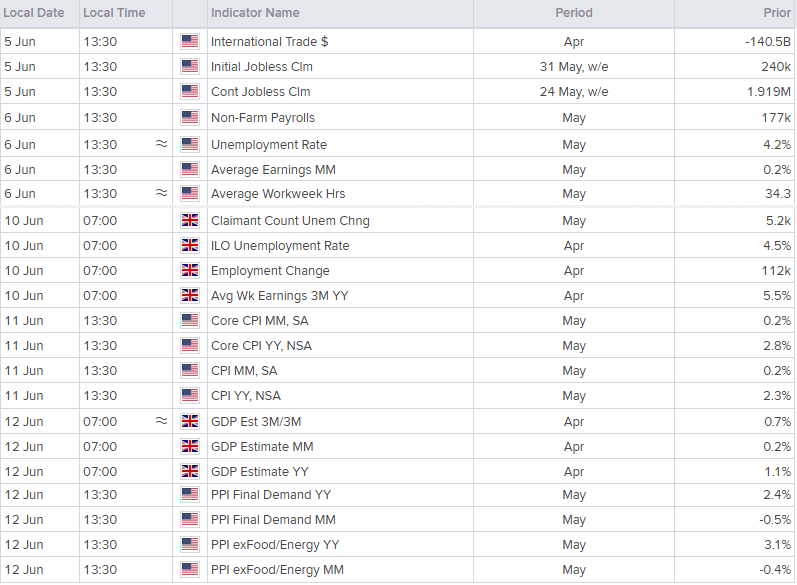

Not only will markets receive U.S. non-farm payrolls this week, but also U.S. CPI and PPI data next week. In the U.K., wages data is also important for BoE policymakers given concerns over the veracity of other labour market releases. Therefore, the confluence of these major releases assures increased volatility, even before trade and fiscal-related concerns are taken into consideration.

Nearer-term, you can’t escape that GBP/USD and EUR/USD have been essentially joined at the hip over the past month, sitting with a correlation coefficient score of 0.96. That means how the euro reacts in response to the ECB interest rate meeting on Thursday may impact Sterling—even though they’re separate monetary jurisdictions.

With a 25 basis point rate cut all but priced, it will come down to what the ECB signals on the rate outlook that drives EUR direction. Heading into the meeting, markets are pricing in a second 25bp move by October, with another cut by year-end deemed a slight possibility. How the ECB shifts that pricing will influence EUR movements into the North American session.

GBP/USD: Bullish Bias if Uptrend Holds

Source: TradingView

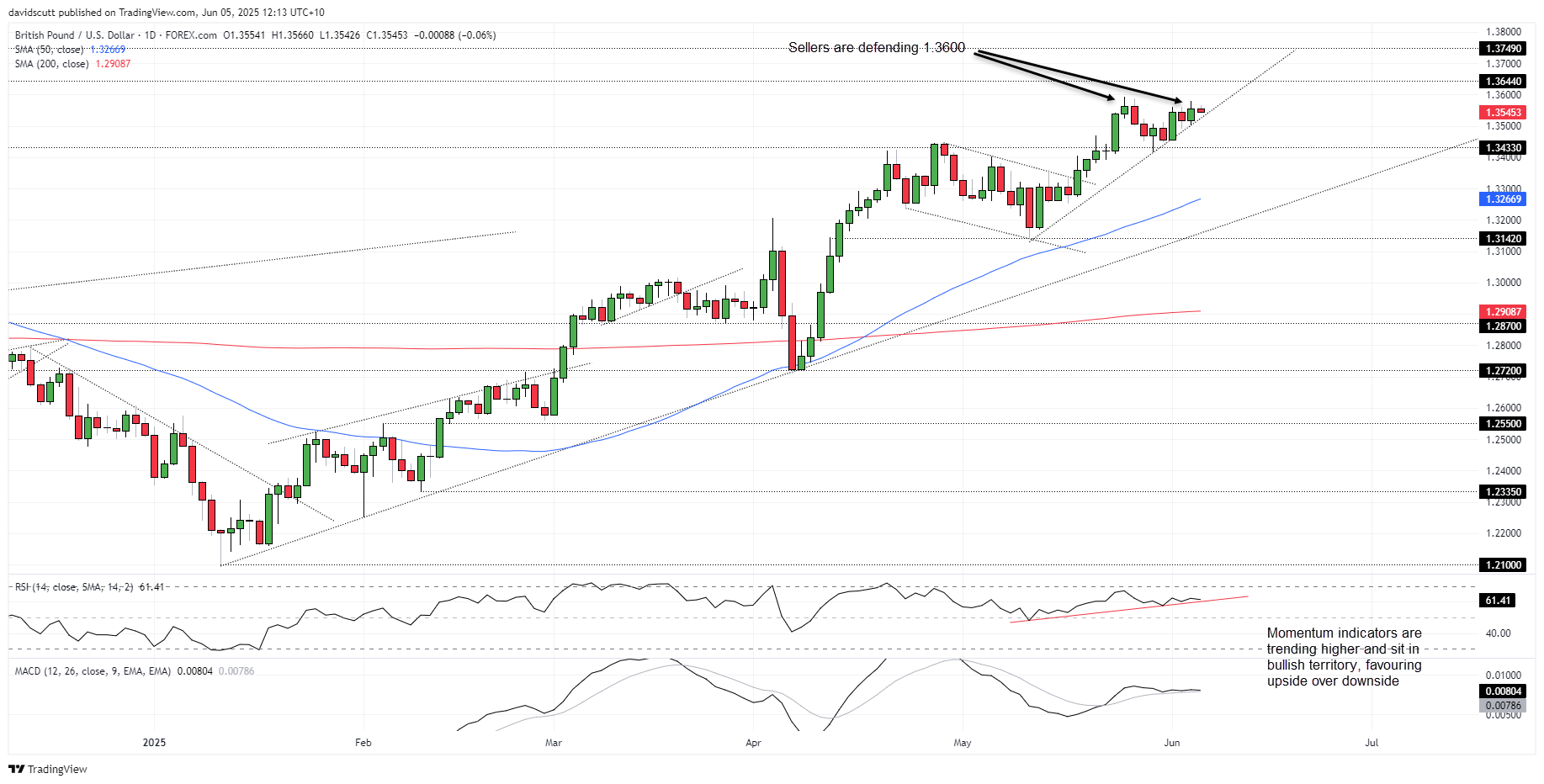

GBP/USD finds itself wedged against uptrend support on the downside and capped beneath 1.3600 on the topside entering this volatility-rich period, giving the sense that when we see a definitive move, it could be a meaningful one. The long topside wicks on the daily candles this week suggest there are plenty of willing sellers around these levels, giving dip buyers at uptrend support plenty to think about.

As long as the pair continues to hold the uptrend, the preference remains to buy dips—especially with momentum indicators continuing to offer bullish signals. To get excited about a resumption of the broader rally, bulls will need to see 1.3593 taken out—the high set on May 26. That would open the door for a possible run towards former market peaks at 1.3644 and 1.3749.

If the uptrend were to be breached, it would shift near-term directional risks sideways to lower, putting 1.3433 into play. That’s a level the pair has done a lot of work either side of in recent years, sitting near the 78.6 Fib level of the 2021–2022 bear move.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Yesterday 11:00 PM

Yesterday 07:48 PM

Yesterday 06:55 PM

Yesterday 11:00 PM

Yesterday 04:47 AM