Key points for the Euro 2025 Q4 outlook

- Euro breakout extends more than 17% off the yearly lows- rallies seven of the past eight-months

- FOMC cuts rates for the first time since December amid elevated inflation & softening employment

- ECB nearing end of easing cycle as inflation approaches 2% target- remains ‘data dependent’

- EUR/USD breakout exhausts into technical resistance into the close of Q3

- Correction risk rises into the close of the year- broader outlook constructive while above 2024 highs

Euro has rallied more than 13% since the start of year with EUR/USD marking the largest single-year range since 2022 and the largest yearly advance since 2017. Price has seen just one monthly-decline this year (July) and while a breakout of a multi-year downtrend keeps the broader focus higher, the advance may be vulnerable into the close of the 2025 as price struggles at a key technical resistance.

Federal Reserve Spotlight

The Federal Reserve cut interest rates by 25 basis points for the first time this year in September as concerns over a softening labor market began to mount. In the latest FOMC rate decision, Chair Powell cited that, “There is No Risk-Free Path,” as the risks to inflation are to the upside, while the risks to employment are to the downside. Powell specifically noted that the decision to cut rates was largely an “insurance” against the potential of a sharper slow down rather than a full pivot to stimulate the economy.

The comments suggest that the Fed’s dual mandate of maximum employment and stable prices remain at odds with inflation still running well-above the central bank’s 2% target. In fact, the latest read on Core Personal Consumption Expenditures show prices up 2.9% y/y in August and with equity markets at all-time highs and unemployment at 4.3%, one could make the argument that the Fed should be on hold, if not raise rates. Historically, inflation is a harder beast to tame than employment and in the current environment, the Fed does risk losing inflation-fighting credibility should prices continue rise; a risk the market has yet to appreciate.

One of the ‘X’ factors for inflation remains the potential impact of tariffs. In his most recent press conference, Chair Powell noted that the “reasonable base case” scenario is that tariffs will be a one-time shift in prices that is likely to occur over several quarters. What that means for policy remains to be seen and despite the inflation risk, market participants are still pricing in another 25 basis point cut in October and December.

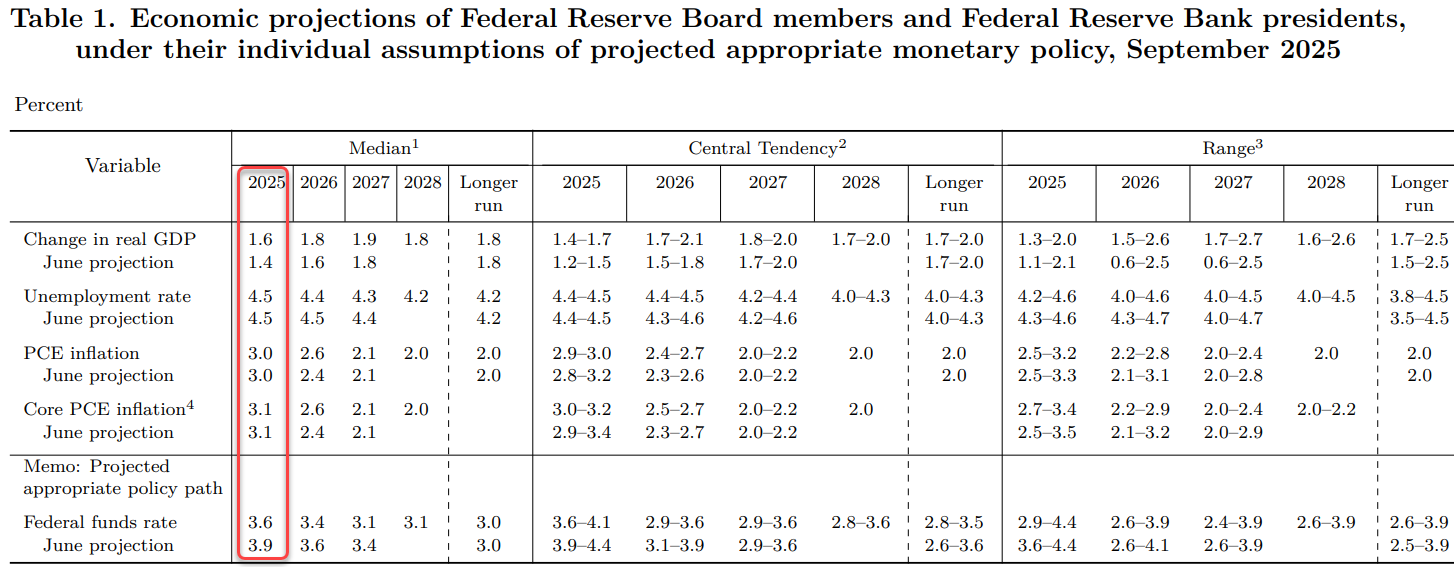

FOMC Summary of Economic Projections

Source: FOMC

The latest Summary of Economic Projections showed an improving growth outlook for 2025 with the committee revising real GDP to 1.6%, up from 1.4% in June. Despite core PCE still expected to end the year above 3%, the updated interest rate dot plot continues to suggest many committee members see scope for at least one more rate cut this year. It’s worth noting that the distribution has widened out considerably and shows that committee members remains split on the appropriate stance for monetary policy.

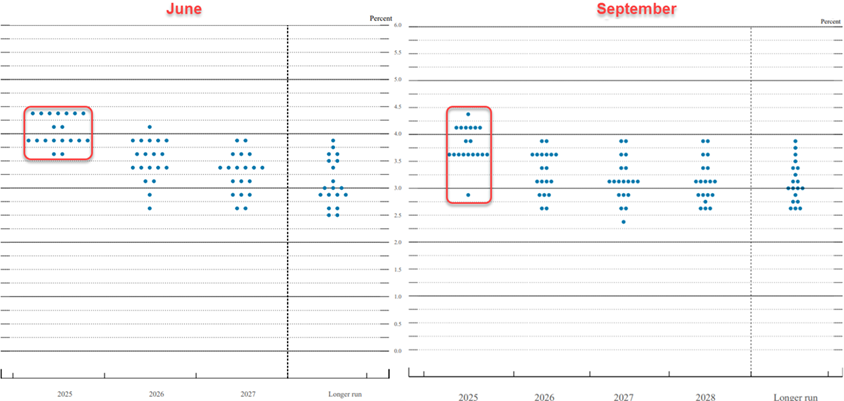

FOMC Interest Rate Dot Plot

Source: FOMC

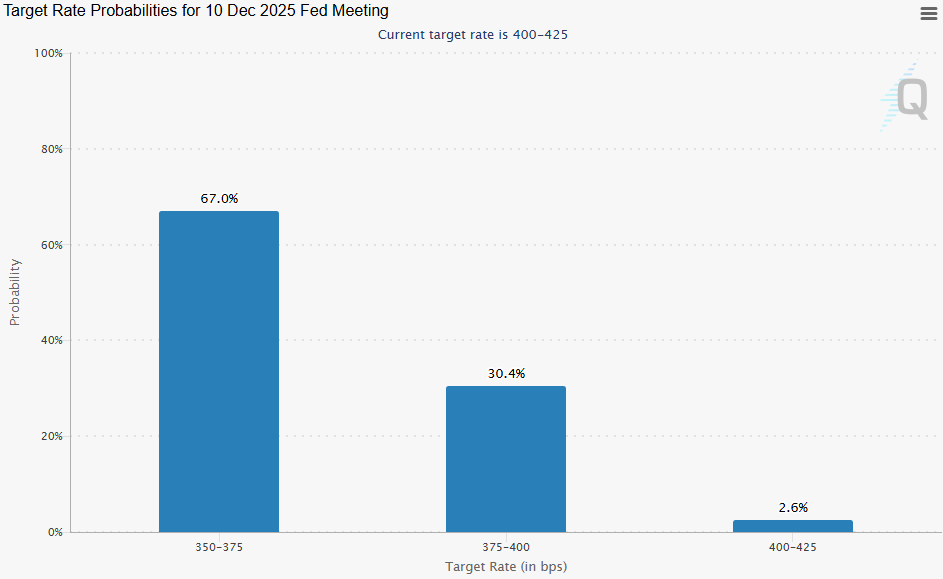

As of late-September, Fed Fund Futures continue to price a 67% chance the central bank will cut another 50 basis points by the end of the year. With investors still insisting lower rates are on the horizon, the risk is for the Fed to disappoint markets- especially if tariffs begin to put further upward pressure on prices and thwart future cuts. For the US Dollar, this could offer a reprieve from the recent selling pressure we’ve seen throughout 2025.

Source: CME

ECB Nearing End of Rate-Cut Cycle?

In June, the European Central Bank cut interest rates by 25 basis points with the central bank signaling it will remain ‘data-dependent’ in the months ahead as inflation in the Euro area approaches the 2% target. In her last press conference, ECB President Christine Lagarde noted that ‘the disinflation process is over’ and the market census has begun to shift with numerous big banks now suggesting the MPC may be done cutting this year.

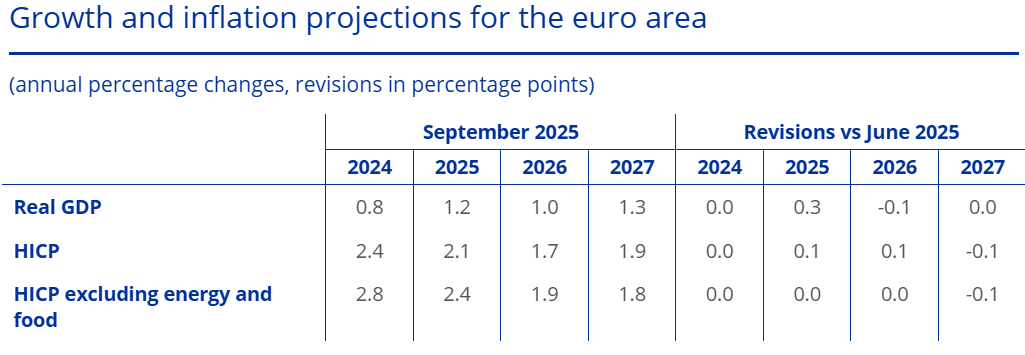

Source: ECB

The ECB growth and inflation projections echoed this sentiment with read GDP revised up 0.3% for 2025 alongside a slight uptick in inflation. This tug-of-war between optimism on growth and slowing disinflationary pressure has market participants (via OIS markets) pricing a near 55% chance we will get further easing by the end of the year. As always, the devil will be in the data here.

Euro Price Chart – EUR/USD Monthly

Chart Prepared by Michael Boutros, Sr. Technical Strategist; EUR/USD on TradingView

Euro rallied into a bottom of a critical resistance zone in September with the advance exhausting post-FOMC at 1.1917-1.2020- a region defined by the 100% extension of the 2022 advance and the 38.2% retracement of the 2008 decline. The focus heading into Q4 is on a reaction off this key pivot zone with the broader outlook constructive while above 38.2% retracement of the 2022 rally / 2020 low-month close (LMC) at 1.1009/33.

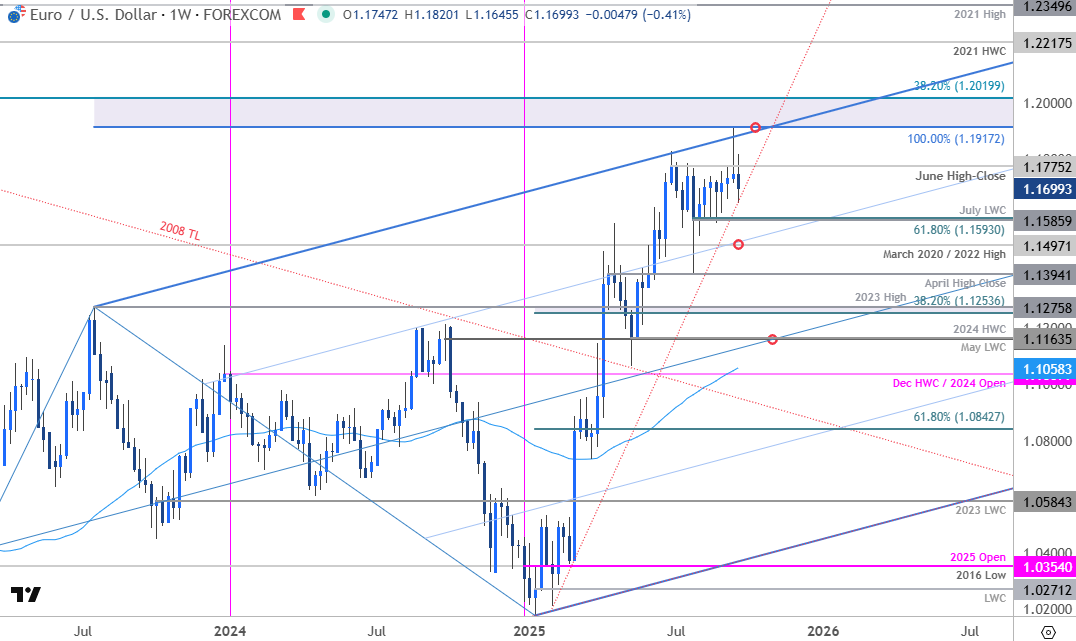

Euro Price Chart – EUR/USD Weekly

Chart Prepared by Michael Boutros, Sr. Technical Strategist; EUR/USD on TradingView

A closer look at the weekly chart shows EUR/USD snapping a three-week rally into the close of September with post-Fed reversal testing the yearly uptrend ahead of the Q4 open. Initial weekly support rests with the July low-week close (LWC) / 61.8% retracement of the July rally at 1.1586/93 and is backed by the March 2020 / 2022 high at 1.1497- note that the 75% parallel rests just lower and a break / close below this slope would be needed to suggest a more significant high is in place / a larger correction is underway. Subsequent support objectives rests with the April high-close at 1.1394 and 1.1253/76- a region defined by the 38.2% retracement of the yearly range and the 2023 swing high (area of interest for possible downside exhaustion / price inflection IF reached).

Key resistance remains unchanged at 1.1917-1.2020 – note that the upper parallel converges on this threshold into the close of the year and a breach / weekly close above this trendline would threaten another bout of accelerated gains for the Euro. Subsequent resistance objectives eyed at the 2021 high-week close (HWC) at 1.2217 and the 2021 swing high at 1.2350.

Bottom Line: Euro rallied into uptrend resistance in September and while the breakout of the 2008 downtrend does keep the broader outlook constructive, the advance is vulnerable into the close of the year while below this critical resistance zone. From a trading standpoint, a good zone to reduce portions of long-exposure / raise protective stops- losses should be limited to 1.1253 IF price is heading for a breakout higher on this stretch with a close above 1.2020 needed to fuel the next major leg of the advance.

--- Written by Michael Boutros, Sr Technical Strategist with FOREX.com

Follow Michael on X @MBForex