Apple enters Q4 earnings with expectations anchored around stability rather than upside surprise. Hardware demand remains mixed, China risks persist, and the stock is no longer priced for aggressive growth. This release is about execution, margins, and Services resilience — not headline-grabbing innovation.

That framing matters given Apple now trades on a premium multiple relative to its history. Against that backdrop, guidance tone and margin performance will be key in determining whether the current valuation remains justified.

View related analysis:

- Tesla (TSLA) Earnings Preview: Q4 Margins in Focus

- Nvidia (NVDA) Earnings Stats for Nasdaq 100 Traders

- Trade to Watch 2026: Nasdaq 100 Correction Risk Before New Highs

- Nasdaq 100 Lags Dow Jones: Divergent Signals Among Nvidia, Apple, Meta

- Dead Cat Bounce Explained: How False Rallies Form in Downtrends

Apple (AAPL) Earnings Preview: What the Market Is Watching

- iPhone revenue trend – stabilisation vs outright decline

- Services growth rate – mid-teens growth is the minimum bar

- Gross margins – especially Services vs Products

- China exposure – demand and regulatory tone

- Guidance tone – conservative or quietly confident

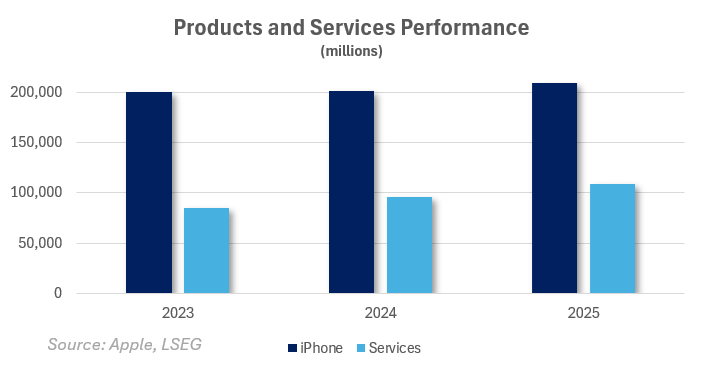

Revenue Breakdown: Hardware vs Services (Apple Earnings)

Source: Apple, LSEG.

While iPhones still account for around half of Apple’s revenue, Services remain the only clear source of structural growth heading into this earnings report. Mac and iPad revenues are cyclical and largely secondary, offering little in the way of a sustained growth narrative.

Investors will be watching whether Services growth holds at a healthy pace, as this segment increasingly shapes the durability of Apple’s earnings. Strong Services momentum can help offset hardware volatility; any slowdown would be harder for the market to ignore.

The iPhone cycle still sets the tone for headline numbers, but at this stage it is the direction of demand that matters more than the magnitude. Apple can live with modest growth or mild softness — it just can’t afford a sharp miss.

What to watch:

- Services revenue growth YoY and as a share of total revenue

- Whether iPhone demand stabilises or shows signs of a sharper slowdown

Margins: Where the Real Signal Lies in Apple Earnings

Margins provide the clearest confirmation of how well Apple is managing its revenue mix. Services carry materially higher margins than hardware, meaning even modest Services growth can have an outsized impact on profitability.

Stable or improving margins would suggest pricing power and effective cost control, even if revenue growth remains uninspiring. By contrast, any meaningful margin compression would raise questions around demand conditions, competitive pressure, or Apple’s ability to pass through costs.

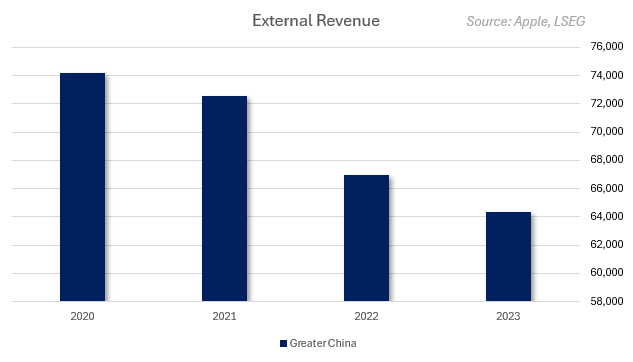

China Risk and Regional Demand

China remains Apple’s largest external risk, not because of tariffs or supply chains, but due to demand sensitivity and geopolitical optics. iPhone sales in the region are increasingly exposed to local competition, national sentiment, and regulatory undercurrents, making China the most unpredictable variable in Apple’s otherwise stable regional mix.

Investors will be listening closely to how management talks about China, rather than any single revenue figure. If conditions are framed as stable or improving, concerns fade quickly. A more defensive tone, however, would see the China risk premium re-emerge — even if reported revenues hold up.

Source: Apple, LSEG

Watch for:

- Explicit China commentary

- Regional revenue breakdowns

- Management tone (defensive vs constructive)

Capital Returns: Buybacks as the Backstop

Apple has leaned heavily on share buybacks since 2012. While this provides a tax-efficient boost to earnings per share and underpins valuation, it also highlights the company’s growing reliance on capital returns as organic growth becomes harder to generate at scale.

Investors will want reassurance that free cash flow continues to comfortably support ongoing buybacks, even if no change in policy is announced.

Guidance and Outlook: Apple Earnings Reaction

As with much of this release, the tone of management’s guidance is likely to matter more than the headline figures. Confident language around demand, Services momentum, margins and capital allocation would reinforce the current narrative, while a cautious or guarded outlook would quickly refocus attention on valuation and downside risks.

This is the real event. Investors will be listening for whether Apple frames demand as stable or challenged, whether Services momentum is described as durable or moderating, and whether there is any hint of acceleration heading into 2026.

- Neutral guidance with stable margins likely sees the market shrug.

- Cautious guidance alongside margin pressure would raise downside risk.

Apple (AAPL) Technical Analysis

The weekly chart shows Apple’s share price topping in December with a shooting star candle just below the 290 level. While volume was below average that week, the subsequent sell-off has been more decisive, with three high-volume bearish candles forming during Apple’s 11.7% decline.

This alone does not determine whether Apple is undergoing a routine retracement or the early stages of a broader bearish reversal. However, with markets entering a bout of risk-off at the time of writing, the near-term bias likely remains skewed to the downside.

Apple’s decline has so far stalled around the 255.53 high-volume node (HVN). Even so, momentum had already begun curling lower on the daily chart, and the risk of a further gap lower remains elevated.

The 250 level is the next key test for bears. A break below there would bring the October low near 244 into focus, close to the 50-week EMA at 242.13. Whether a deeper pullback unfolds may depend on whether geopolitical tensions trigger a broader global risk-off move. Failing that, Apple could stabilise and bounce into earnings, with price action then taking its cue from the results.

Source: Apple, TradingView

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade