AUD/USD heads into Q4 at a crossroads, with Australia’s economy showing early signs of slowing, the labour market softening, and the RBA under pressure to ease further. Seasonality is generally supportive of the Australian dollar in Q4, but subdued volatility and dovish policy expectations suggest rallies may be capped without a fresh macro catalyst.

View related analysis:

- Australian CPI Data Supports RBA’s Cautious Approach on Rate Cuts

- ASX 200 Outlook: RBA to Stay Cautious After Softer Employment Report

- AUD/USD H2 Outlook: Can the Australian Dollar Keep Rebounding?

- Q2 2025 AUD/USD Outlook: Is a Weaker Yuan the Final Blow for Aussie Dollar Bulls?

AUD/USD Q4 Forecast: Growth Risks and Policy Shifts Shape Outlook

Key themes for traders in Q4:

- US jobs market expected to weaken, opening the door for more dovish Fed pricing in 2026

- Seasonal strength in October, but limited upside in November–December

- Options market signals subdued volatility, though AUD downside may be contained

- RBA and Fed both likely to cut once, leaving rate differentials largely unchanged

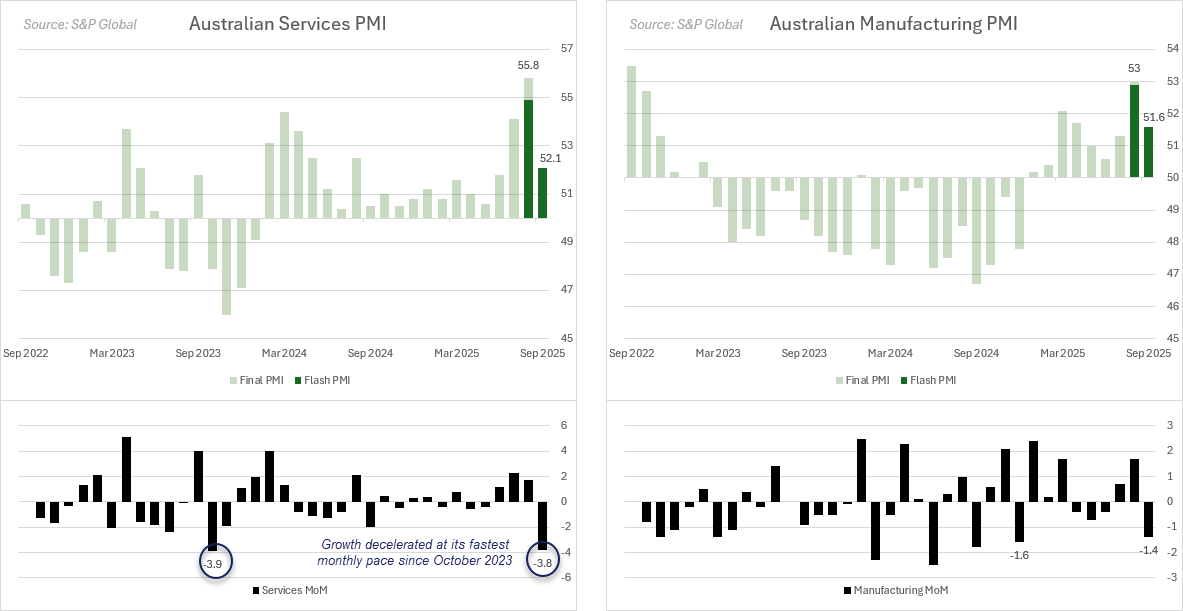

Australian PMIs and Consumer Confidence Signal Softer Growth in Q4

Australia’s latest PMI data from S&P Global suggests growth momentum could soften further heading into Q4. The services PMI dropped sharply from 55.8 to 52.1 in September, a -3.8 point month-on-month fall that marks the steepest decline since October 2023.

Meanwhile, the manufacturing PMI slipped from 53.0 to 51.6, its sharpest monthly decline since December, with a -1.4 point drop.

The survey highlighted weakening market conditions, with both manufacturers and service providers reporting softer demand and reduced optimism about growth prospects over the next 12 months.

A separate consumer sentiment survey from ANZ-Roy Morgan revealed that confidence fell to its lowest level since the Albanese government took the helm, with 4% of respondents saying their financial situation was “worse off” than 12 months ago, with 32% saying they expect to be “worse off” in a year.

Data source: S&P Global, LSEG

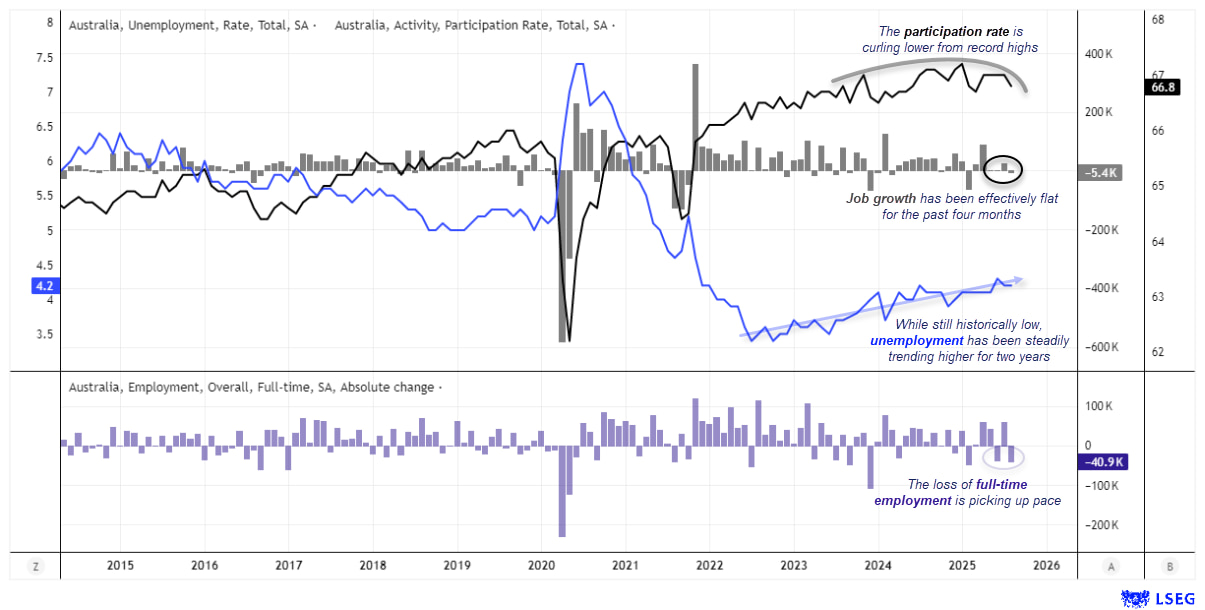

Australian Jobs Market Weakens as Full-Time Employment Falls

The labour market is not signalling a recession just yet with the unemployment rate holding at 4.2%, but signs of slack are emerging. The unemployment rate has been trending higher for two years, while the participation rate is edging lower from record highs. The headline job growth figure has also been close to zero for the past four months, two of which has seen full-time employment slashed by around 40k jobs.

While the jobs market is softening, conditions are not weak enough to justify drastic policy action from the RBA at this stage, though it could pave the way for a cut or two.

Data source: ABS, LSEG

RBA and Fed Policy Outlook: Rate Cuts Likely in Q4

A recent Reuters poll shows that 35 out of 38 economists expect a single 25bp RBA cut by December. Meanwhile, RBA cash rate futures are projecting a terminal rate of 3.125% by July 2026, implying around 47.5bp of easing by the start of H2 2026.

In my view, the RBA could act as early as November, with trimmed mean inflation now sitting comfortably inside the 2–3% target band and the labour market gradually weakening. The timing of a further 25bp cut will depend on how quickly conditions deteriorate, though Q1 2026 looks possible, with Q2 more likely.

For the Fed, futures currently imply an 85% chance of a November cut, but the odds of a December move have diminished after Q2 GDP was revised higher to 3.8%. While the US labour market is softening, inflation is also ticking higher, making it harder for the Fed to commit to further easing. This has seen the US dollar rebound from key support levels, as markets reduce expectations of a second December cut. This leaves the RBA–Fed interest rate spread anchored at -90bp, assuming both central banks deliver just one cut in Q4.

Data source: RBA, Fed, LSEG

RBA, Fed/FOMC Meetings in Q4

- 20 October 2025: Fed Interest Rate Decision

- 4 November 2025: RBA Cash rate Decision

- 9 December 2025: RBA Cash rate Decision

- 12 December 2025: Fed Interest Rate Decision, FOMC Projections

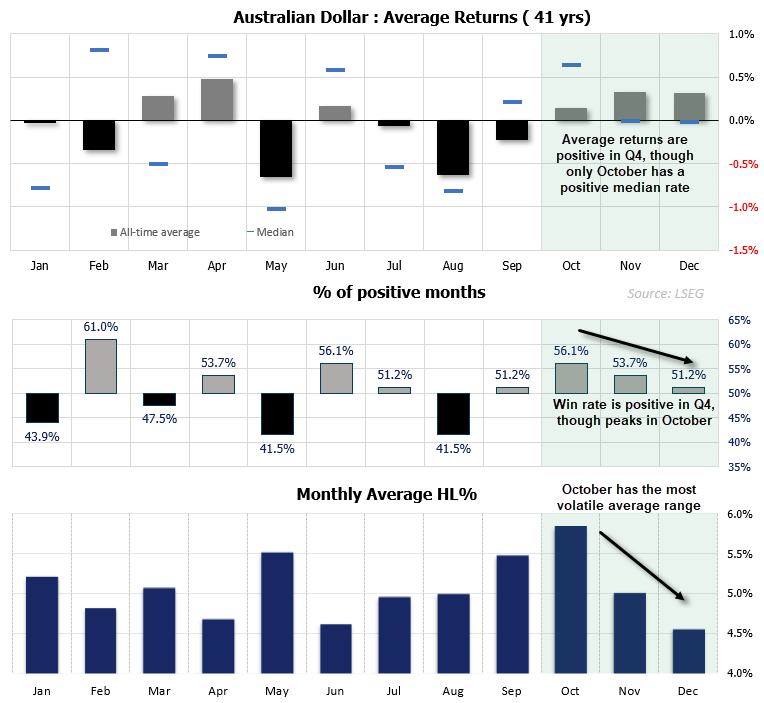

AUD/USD Seasonality Trends in Q4 2025

Seasonality patterns suggest a broadly supportive backdrop for the Australian dollar in the fourth quarter. Looking back over 41 years since the float of the AUD in December 1983, AUD/USD has delivered an average quarterly return of +0.15% with a 56.1% win rate.

October stands out as the strongest month historically, with a median return of +0.64% and the widest trading range, averaging 5.83% high-to-low volatility. This makes October a key month for AUD/USD bulls, as seasonal strength has often coincided with higher risk appetite at the start of Q4.

However, seasonal tailwinds moderate in the later months. November and December both show small positive average returns (+0.33% and +0.32%), though their median returns are flat, with win rates easing to 53.7% and 51.2% respectively. This suggests that while Q4 is generally constructive for AUD/USD, much of the upside tendency is historically concentrated in October.

Data source: LSEG

AUD/USD Options Market Points to Low Volatility, Limited Downside

Q3 is shaping up as the least volatile quarter for AUD/USD in more than a decade, with a high-to-low range of just 4.4%. The quarterly candle is also on track to print a small doji, offering little directional guidance for Q4. Options markets suggest volatility may remain subdued, with limited room for large moves in either direction.

The 1-month implied volatility (IV) has been trending lower since the Trump tariff shock of 2024, now sitting near 7.5% – its lowest level since July 2024. Realised volatility has followed the same downtrend, reinforcing the view that without a new macro catalyst, Q4 could remain range-bound.

However, the 3-month risk reversal remains elevated relative to spot price action, indicating that option traders are still paying a premium for calls over puts. This skew suggests investors expect any AUD/USD pullback to be shallow, leaving the Australian dollar supported into Q4.

Data source: RBA, Fed, LSEG

Conclusion: AUD/USD Outlook for Q4 2025

AUD/USD enters the final quarter of 2025 facing competing forces. Seasonal patterns and options positioning suggest that downside risks are limited, particularly in October when the Australian dollar has historically delivered its strongest returns.

However, a weakening domestic economy, falling consumer confidence, and cracks in the labour market point to softer resilience as the year progresses. These headwinds may temper enthusiasm for sustained rallies.

With both the RBA and the Fed expected to deliver one more 25bp cut in Q4, the policy rate differential is likely to narrow to around -65bp. This should help limit downside pressure on AUD/USD and could even provide scope for recovery into year-end.

Overall, volatility is expected to remain subdued. Dips may be cushioned by supportive options positioning, but rallies are likely to be restrained without a fresh macro catalyst. Traders should remain alert to October’s seasonal strength while cautious of broader economic headwinds that may limit follow-through.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade