The US dollar is quietly regaining favour among futures traders, but this isn’t a classic “risk-off” move.

Instead, the latest COT data suggests a broader clean-up of positioning, with traders reducing exposure across FX markets as geopolitical risks and volatility rise.

View related analysis:

- Australian Dollar Outlook: Strait of Hormuz Risk Clouds AUD/USD Rally

- FX Futures Positioning: USD, EUR, GBP, JPY | COT report

- US Dollar Rallies Post Fed, USD/JPY Eyes 160, USD/CHF Breaks Higher

COT Report Shows USD Rebound as EUR Weakens and AUD Sentiment Peaks

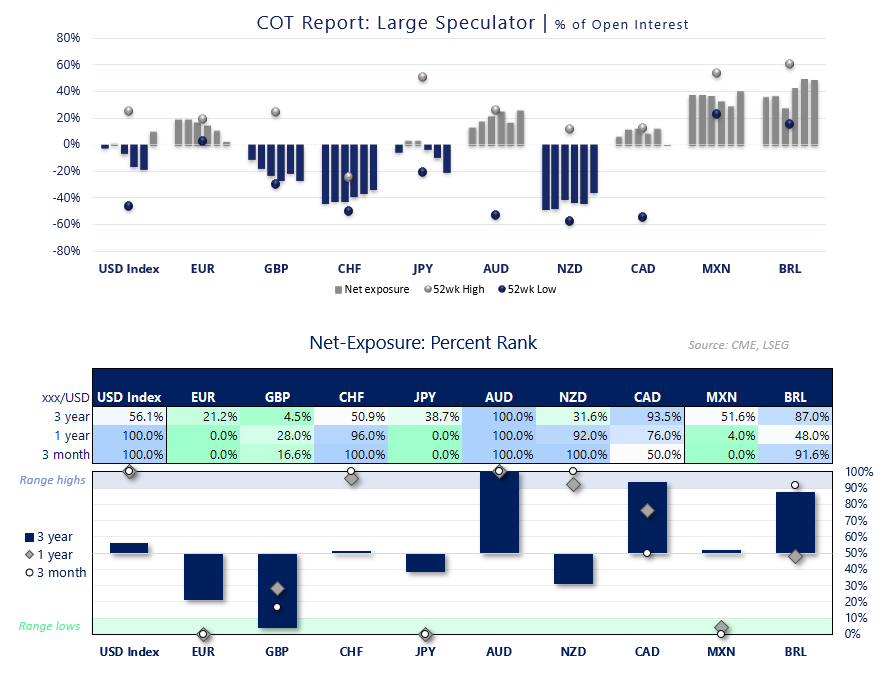

Large Speculator Positioning from the COT report

Source: CFTC (COT), LSEG

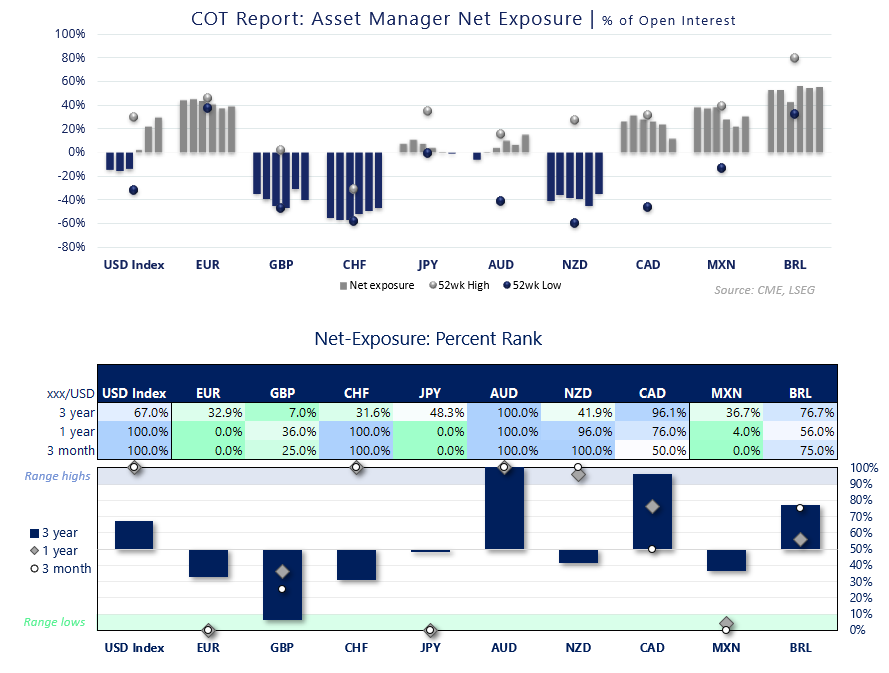

- US Dollar: Large speculators flipped to net-long exposure on the US dollar index, while asset managers pushed their net bullish exposure to a fresh one-year high.

- EUR/USD: Long positions continued to fall while shorts rose among both groups, with large speculators on the cusp of flipping to net-short exposure.

- GBP/USD: Short bets declined by 17% and 18% among large speculators and asset managers, respectively.

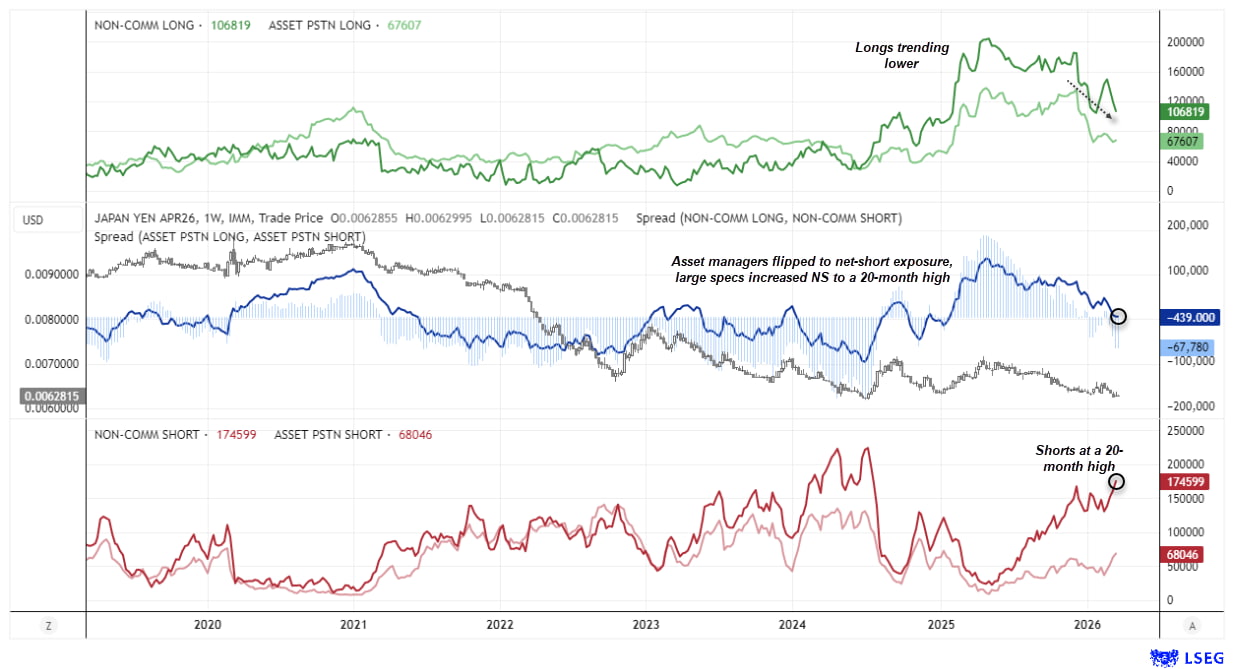

- USD/JPY: Asset managers flipped to net-short yen futures, large speculators increased net-short exposure to a 20-month high.

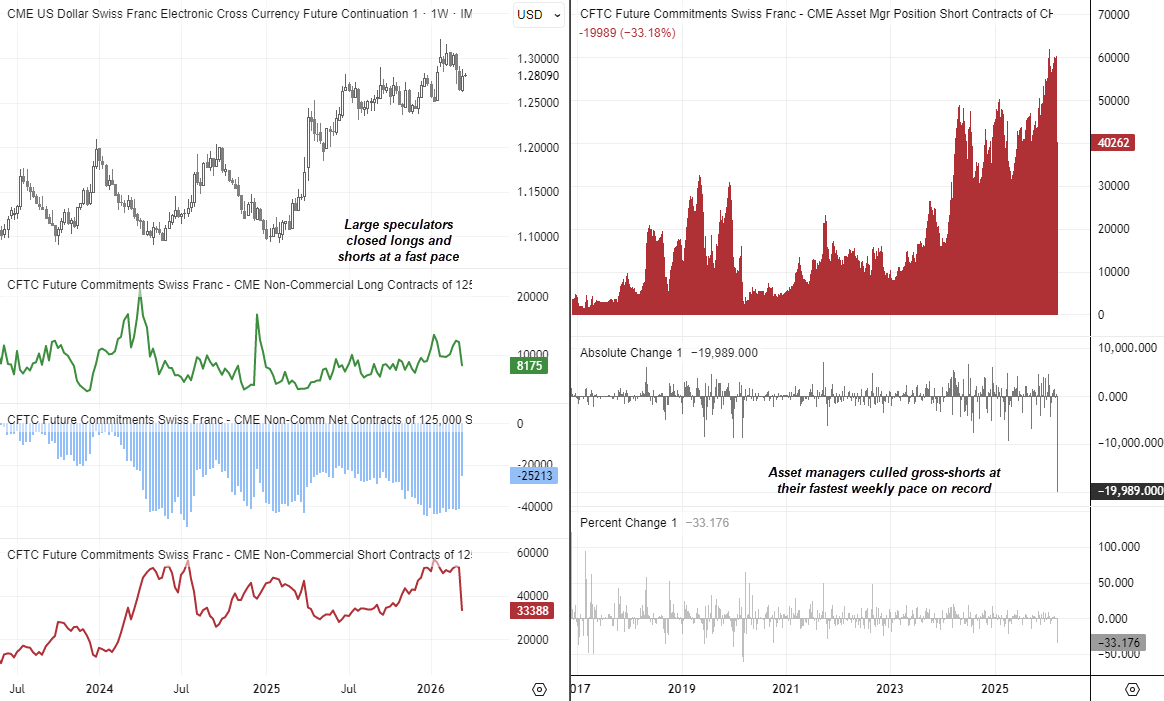

- USD/CHF: Gross short positions fell by 37% among large speculators and 33% among asset managers last week.

- USD/CAD: Large speculators were on the cusp of flipping to net-short Canadian dollar futures, while gross longs fell notably among asset managers.

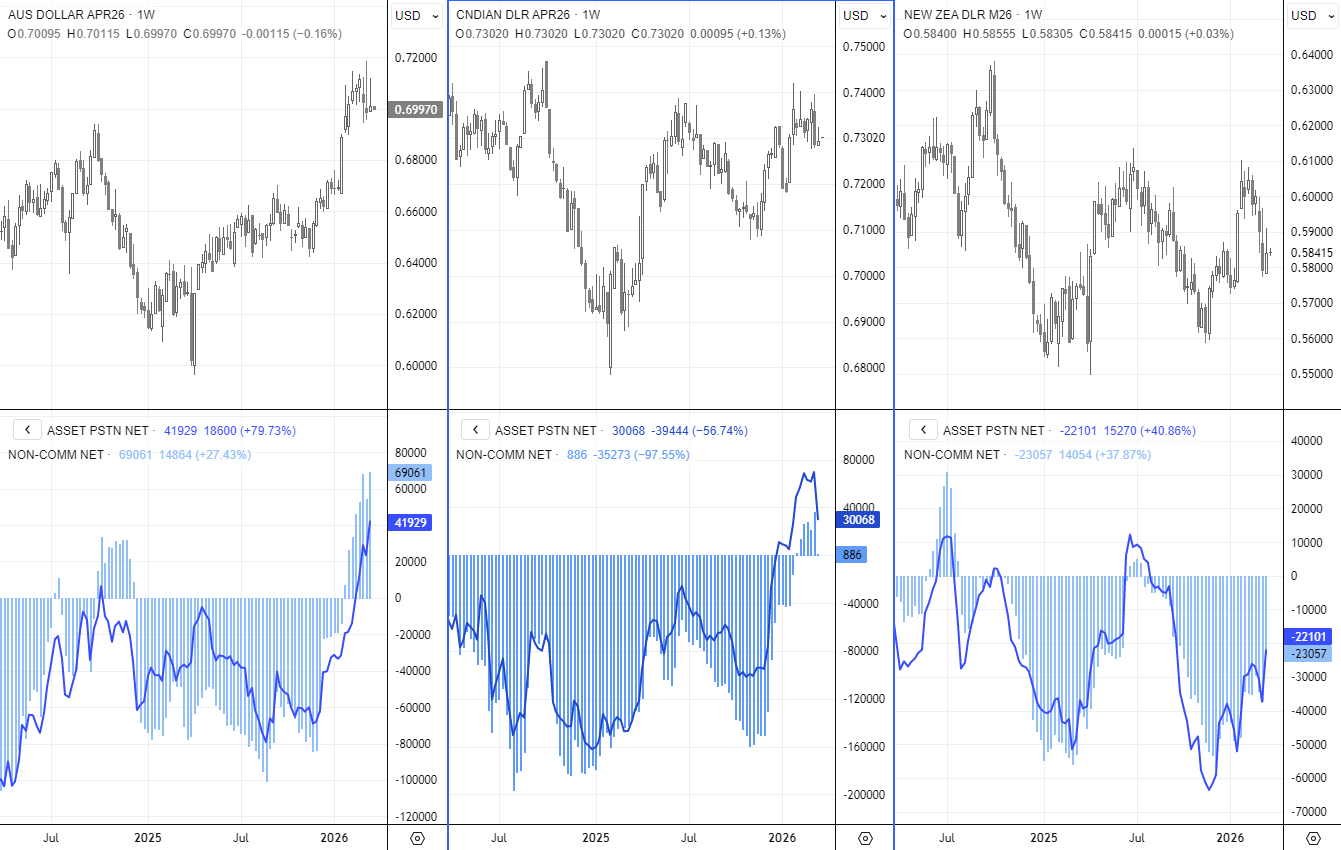

- AUD/USD: Adjusted for open interest, the percent rank for Australian dollar futures points to a bullish sentiment extreme across the 3-month, 1-year, and 3-year timeframes among both groups.

- NZD/USD: Net-short exposure declined to a five-month low among both groups.

Asset Manager Positioning | COT Report

Source: CFTC (COT), LSEG

FX Futures Positioning | COT Report (IMM Data)

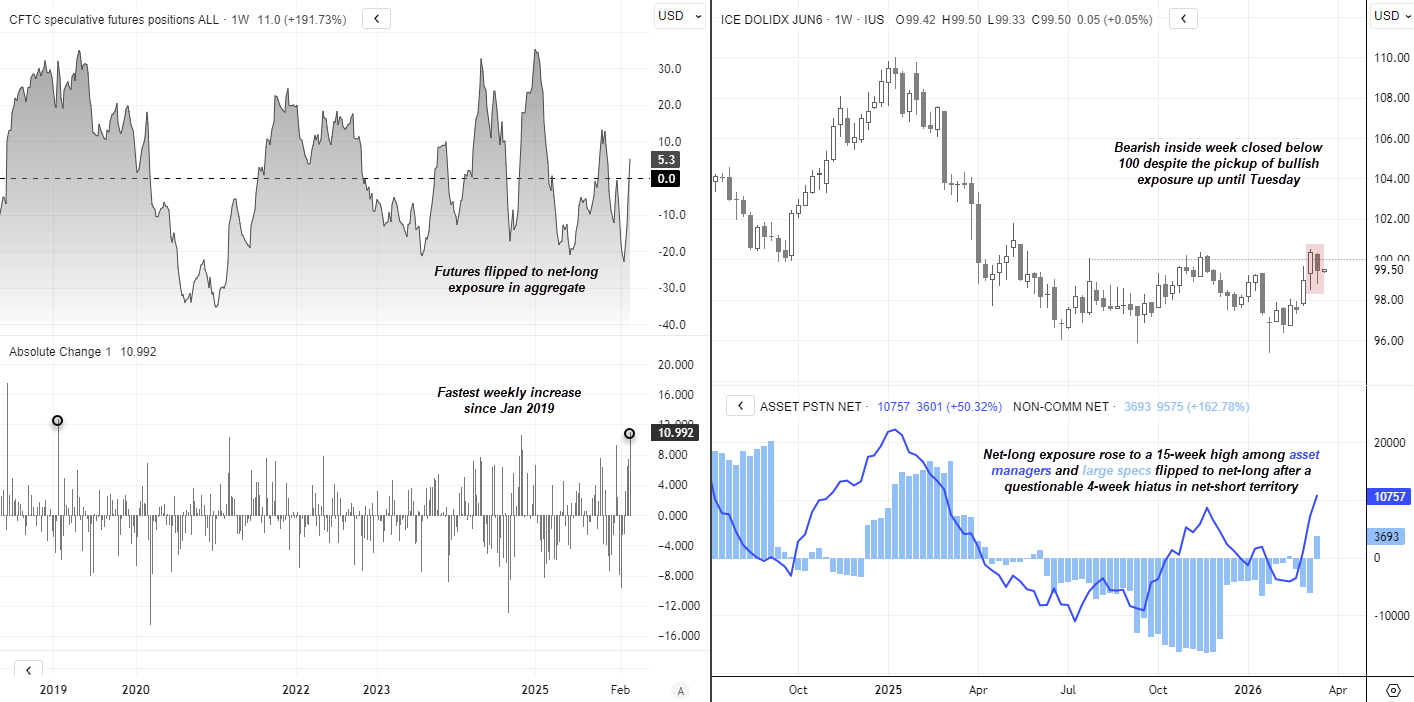

US Dollar Index (DXY) Futures Positioning | COT Report

Futures traders flipped to net-long US dollar exposure last week. Their $10.9 billion weekly increase marked the fastest rise since January 2019, lifting net-long exposure to a 15-week high of $5.4 billion.

Importantly, this still falls short of a sentiment extreme when viewed against the multi-year range.

Asset managers are now at their most bullish on the US dollar index in a year, while large speculators have reverted to net-long exposure after a questionable four-week stint in net-short territory.

However, the weekly US dollar index chart shows a bearish inside week that closed back below 100. I suspect this is a temporary setback within an otherwise firm bullish trend on the daily chart, with dips likely to remain attractive for a move towards 102.

Source: CFTC (COT), ICE, LSEG

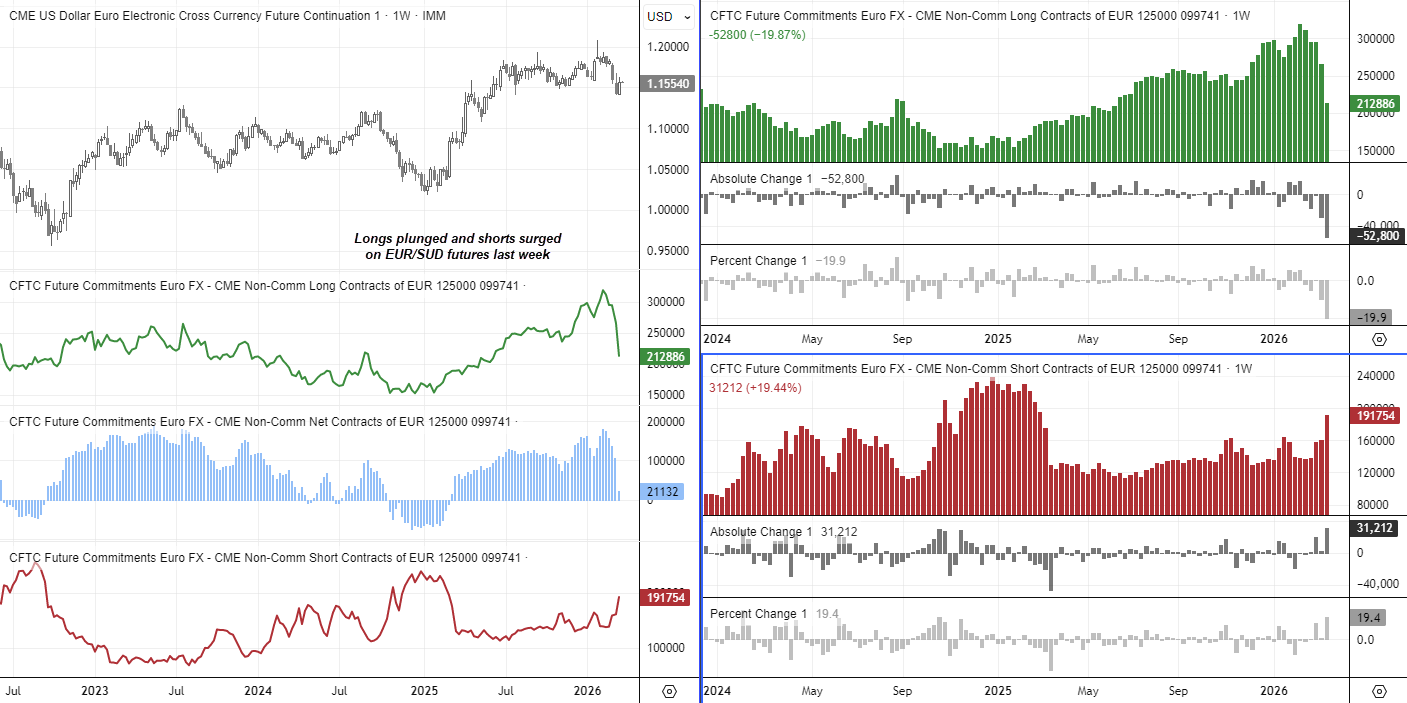

EUR/USD Futures Positioning | COT Report

Long positions on the euro plunged while shorts accelerated last week among asset managers and large speculators. By Tuesday’s close, EUR/USD futures traders held just 21.1k net-long contracts — their least bullish level in just over a year.

Gross longs fell by 52.8k contracts (-20%), while shorts rose by 31.2k (+19%), suggesting bearish pressure is building despite the recent pullback.

Given this shift occurred before President Trump’s two-day warning to Iran to reopen the Strait of Hormuz, positioning may have already flipped to net-short exposure since.

Source: CFTC (COT), ICE, LSEG

USD/JPY Futures Positioning | COT Report

The bullish case for the Japanese yen continues to unravel, with its safe-haven appeal largely ignored. Asset managers flipped to net-short exposure for the first time in over a year last week, while net-short exposure among large speculators rose to a 20-month high.

Long positions also continued to trend lower across both groups, reinforcing the shift in sentiment against the yen.

Source: CFTC (COT), ICE, LSEG

USD/CHF Futures Positioning | COT Report

Short bets against the Swiss franc saw a record outflow last week, with asset managers cutting gross shorts by around 20k contracts (-33%). With gross longs little changed, this drove a sharp reduction in net-short exposure at a record weekly pace.

This suggests real money accounts were reducing downside exposure to the franc, likely as part of a broader move to cut risk and raise cash during a more volatile macro backdrop.

There was also clear evidence of deleveraging among large speculators. Net-short exposure nearly halved as longs fell by 3.9k (-32%) and shorts dropped by 19.8k (-37%).

Source: CFTC (COT), ICE, LSEG

AUD/USD, USD/CAD, NZD/USD Futures Positioning | COT Report

Australian dollar futures

We’re seeing a divergence among the major commodity currencies in terms of positioning. Net-long exposure in Australian dollar futures has continued to rise, with asset managers pushing theirs to a record high and large speculators reaching a nine-year high.

However, with the percent rank at 100% across the 3-month, 1-year and 3-year timeframes for both groups — and prices now pulling back — a sentiment extreme may already be in place.

Canadian dollar futures

Meanwhile, large speculators were on the cusp of flipping to net-short exposure on CAD futures, while asset managers reduced their net-long exposure by more than 50%.

The move appears to be driven primarily by a sharp closure of longs rather than a build-up of shorts, suggesting it may reflect caution around oil prices and Middle East tensions, rather than a firm shift towards expectations of further BoC rate cuts.

New Zealand dollar futures

At the other end of the spectrum, net-short exposure to New Zealand dollar futures has continued to decline. Large speculators and asset managers have reduced net-short positions to a six-month low of around -22k contracts.

Traders appear increasingly convinced that the RBNZ’s cutting cycle is over, although expectations for rate hikes remain limited.

Source: CFTC (COT), ICE, LSEG

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade