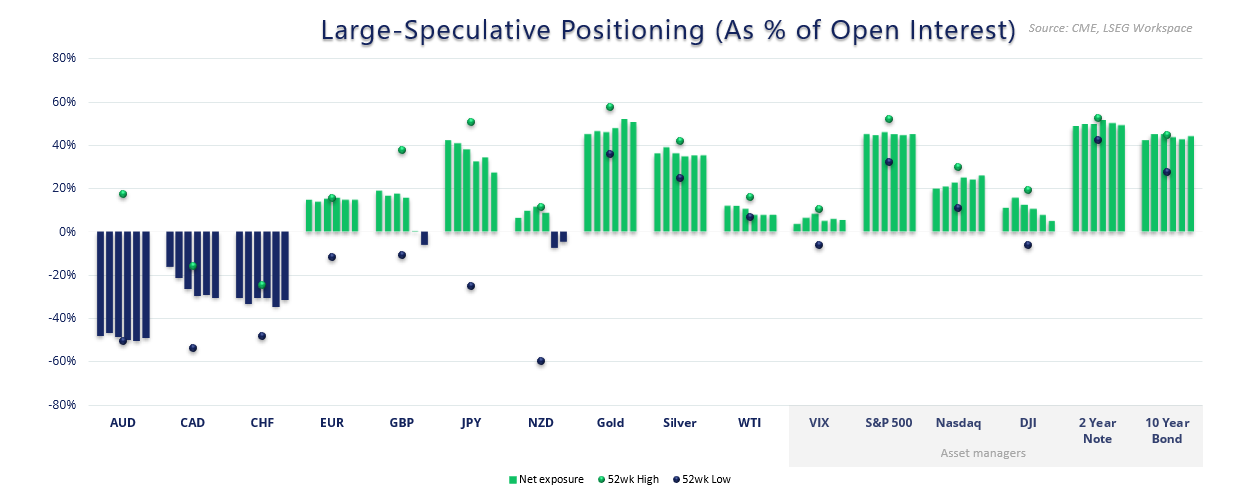

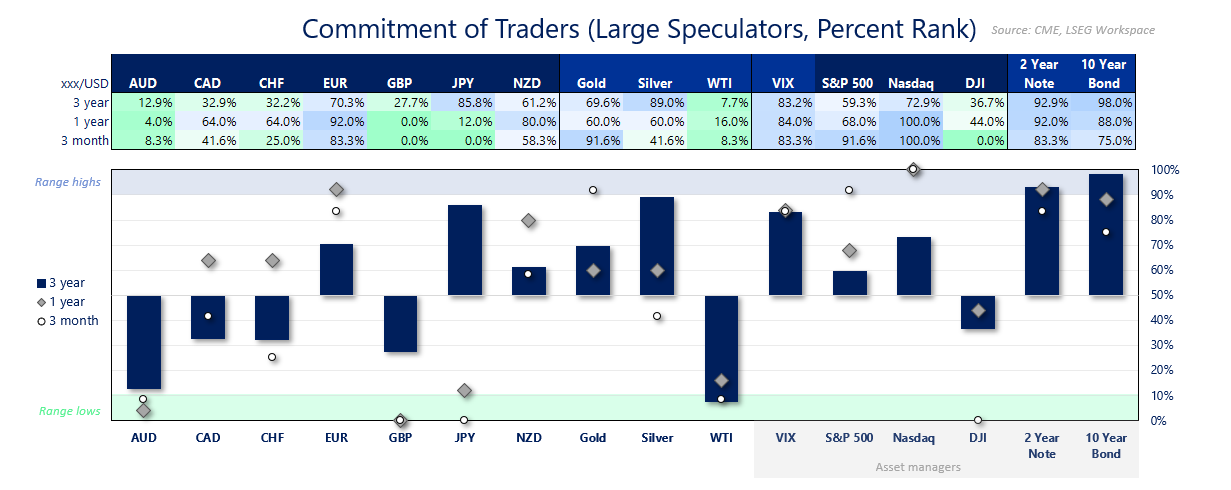

Traders continued to adjust their positioning across major futures markets last week as central bank expectations shifted further. The British pound flipped to net-short for the first time since February, large specs retreated from the Japanese yen to a 22-month low, and gold longs saw their sharpest weekly cut in four months. Meanwhile, net exposure to the US dollar index, euro, and commodity currencies reflected rising volatility around interest rate expectations—particularly the growing belief in three Fed rate cuts by year-end.

View related analysis:

- AUD/USD Weekly Outlook: Fed Bets Boost Aussie as US Data Weakens

- US Dollar, EUR/USD, USD/JPY Analysis: Weekly COT Report Highlights

- US Dollar Rally at Risk as Fed's Waller Fuels Dovish Pivot Speculation

Speculators Cut Gold, Dump Yen and Pound as Fed Cut Bets Reshape Positioning

- US Dollar (USD): Asset managers trimmed net-short exposure to the USD index for a second week to -5.9k contracts

- European dollar (EUR): Net-long exposure fell for a second week to +123.4k contracts

- British pound (GBP): Large specs flipped to net-short exposure for the first time since February

- Japanese yen (JPY): Net-long exposure fell to a 22-month low of 89.2k

- Australian dollar (AUD): Net-short exposure fell for the first week in four

- Canadian dollar (CAD): Net-long exposure rose to a seven-week high

- New Zealand dollar (NZD): Traders remained net-short for a second week at -2k contracts

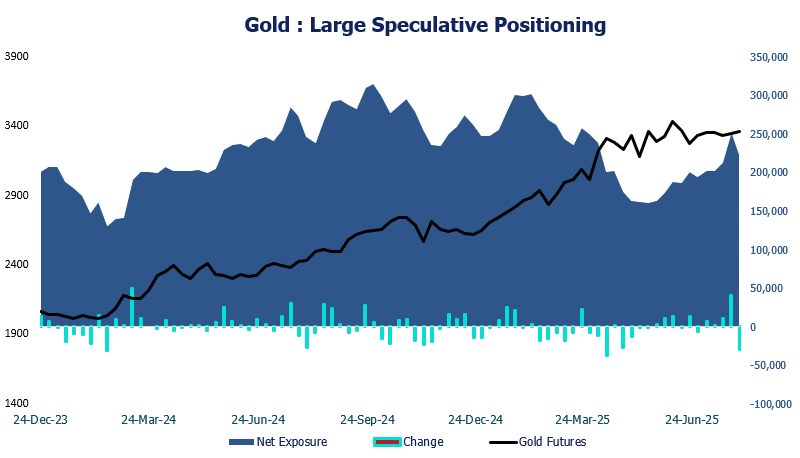

- Gold (GC): Net-long exposure fell by -29.4k contracts, its fastest weekly pace in 16

Charts prepared by Martt Simpson - Datasource: CME, LSEG

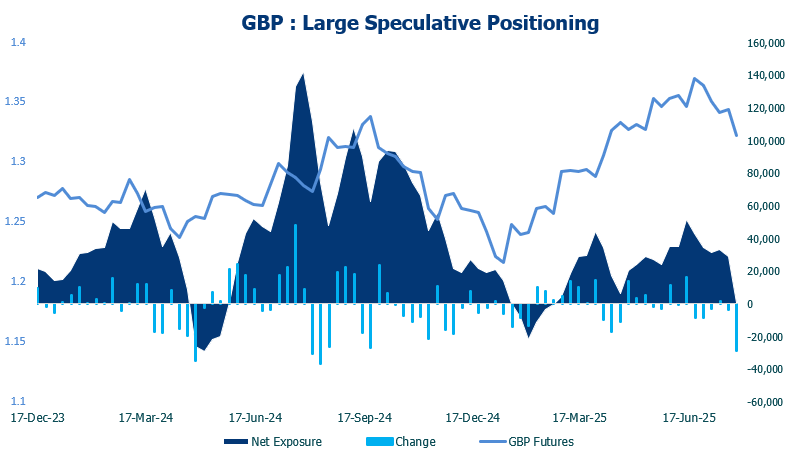

GBP/USD Positioning: British Pound Futures – Weekly COT Report

Large speculators flipped to net-short exposure to British pound futures for the first time since February. Their -12.6k week-over-week change brings the decline from net-long exposure to -45k over the past three weeks alone, as traders ramp up bets on potential Bank of England (BoE) easing.

GBP/USD had fallen as much as -4.7% from its June high to last week’s low, though renewed expectations of Fed cuts have seen it recover 1.3% from the lows.

Chart prepared by Matt Simpson – Data source: CME, LSEG

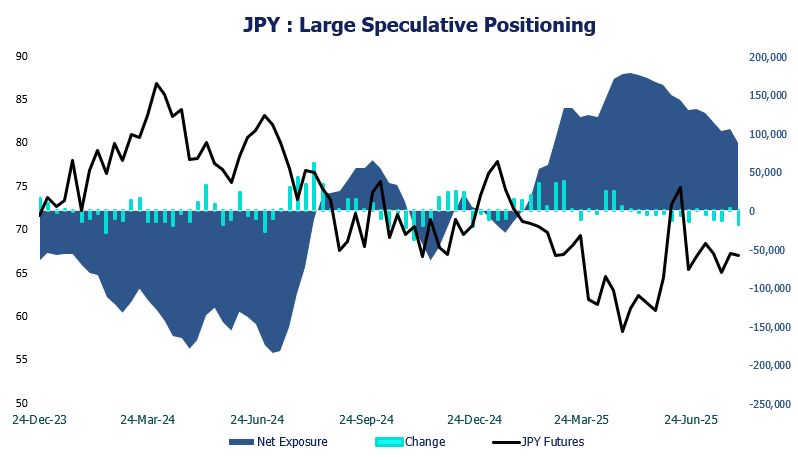

JPY/USD Positioning: Japanese Yen Futures – Weekly COT Report

Traders continued to shy away from the yen, with net-long exposure among large speculators falling to a 22-month low. The Bank of Japan (BoJ) held policy unchanged as expected and offered little indication of a shift anytime soon—sending gross short positioning by large speculators higher in recent weeks.

However, with markets now pricing in the potential for three back-to-back Fed cuts by December, the outlook for USD/JPY may start to shift. Whether that’s enough to tempt sidelined yen bulls back into the market remains debatable, especially with the BoJ also in a holding pattern. That said, the yen appears undervalued in the current environment, which could ultimately prove bearish for USD/JPY.

hart prepared by Matt Simpson – Data source: CME, LSEG

Gold Futures Positioning (GC): Weekly COT Report Analysis

Large speculators reduced their net-long exposure at their fastest weekly pace in 16 last week, though it was mostly a function of longs being covered over short initiation. Gold bulls closed -30.7k gross long contracts last week compared with a reduction of -1.3k gross shorts. But with the US dollar very much offered once more, it seems like the shakeout in gold may be short lived.

Chart prepared by Matt Simpson – Data source: CME, LSEG

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade