Q1 Recap:

GBP/USD started the year strongly with the pound benefiting from a softer U.S. dollar, resilient UK data, and optimism that the Bank of England would remain relatively cautious on rate cuts, pushing the pair up toward the mid-to-upper 1.36s in late January. Through February, the rally lost momentum and the pair largely consolidated around the mid-1.35 area as markets reassessed the BoE-Fed policy gap and questioned how durable UK growth would be.

By March, sentiment shifted more clearly back in favour of the U.S. dollar as rising geopolitical tensions, higher oil prices, and broader safe-haven demand weighed on sterling, especially given the UK’s sensitivity to energy-driven inflation shocks. As a result, GBP/USD gave back part of its earlier gains and ended the quarter closer to the low-to-mid 1.33s, leaving Q1 best characterised as a quarter of early sterling strength followed by a late-quarter dollar recovery.

But where could the UK economy and GBP go from here, and will the USD continue to benefit from safe haven demand?

Q2 GBP Outlook:

- Inflation

The UK economic outlook now depends heavily on two variables: how long the Iran conflict persists and how high oil prices could rise. Those two interrelated factors will determine the scale and persistence of the energy shock now feeding into the UK economy.

The UK is particularly vulnerable to higher oil and gas prices given its reliance on imported energy. In the March BoE meeting, the central bank lifted its inflation forecast to 3.5% by Q3. The OECD has warned that the UK is among the more exposed major economies to a global energy shock and now expects UK inflation to rise to around 4% this year, which would leave it among the highest in the G7.

Markets are increasingly bracing for inflation to peak somewhere in the 3.5%–4.0% range. However, the eventual high will depend largely on the duration of the conflict and the extent of any sustained disruption to energy supply.

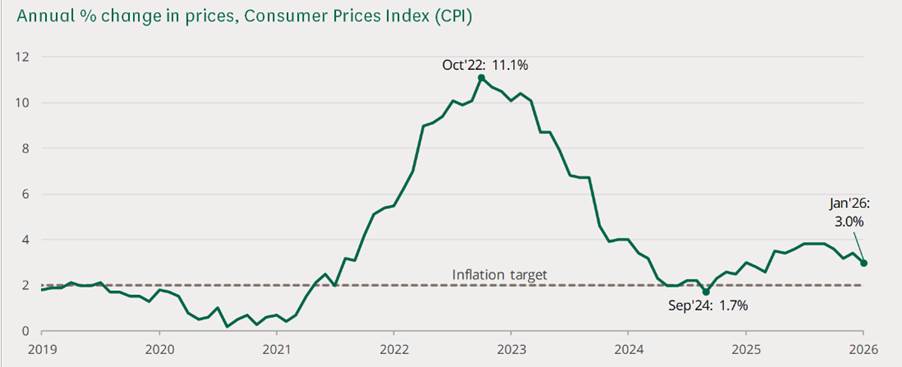

Put simply, the longer the conflict lasts, the longer energy prices remain elevated, and the broader the inflation pass-through becomes. Higher fuel and energy costs raise transport, production, and input costs, feeding into prices for goods and services across the economy. This is particularly concerning because UK inflation was already proving sticky before the conflict intensified. In February, headline CPI stood at 3.0%, while core inflation at 3.2% and services inflation at 4.3% still well above the Bank of England’s 2% target. In other words, this is not an inflation shock hitting a clean disinflation backdrop; it is arriving while underlying domestic price pressures are already above target.

Source: ONS

- Growth

At the same time, the growth outlook is weakening. Higher energy costs will act as a headwind on households and firms, squeezing real incomes, margins, and demand. That comes at a poor time for the UK economy, which was already losing momentum before the conflict. Monthly GDP was flat in January (0% MoM). The OECD has revised down its 2026 UK growth forecast to 0.7% from 1.2% previously, representing one of the sharpest downgrades in its latest interim outlook.

The UK is therefore facing a more difficult macro mix of slower growth and higher inflation — stagflation. This is a challenging backdrop for the BoE, given the different policy responses required for high inflation and slow growth.

- BoE Outlook

This leaves the Bank of England in a difficult position. At its final Q1 meeting, the BoE signalled a willingness to respond if inflation expectations become unanchored. Still, policymakers are unlikely to react to an externally driven oil shock unless it begins to generate clearer second-round effects through wages, service inflation, and inflation expectations.

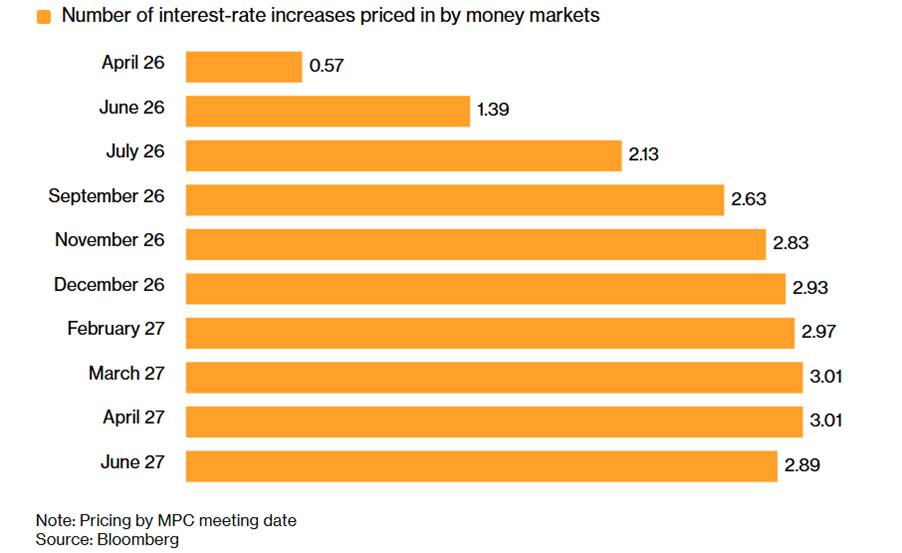

BoE expectations have moved aggressively in response to the conflict. Before the escalation, investors were largely pricing in one, possibly two, rate cuts across 2026. That has now reversed sharply, with markets pricing in two full rate hikes and a meaningful probability of a third. However, that repricing looks vulnerable to reversal.

The key point is that this energy shock is serious. Brent is on track to book its sharpest monthly price increase on record, up over 55% since the war started.

Unlike in 2022, the UK economy today is not running as hot, and while inflation remains sticky, the broader macro backdrop is weaker, unemployment is higher, and demand is softer. During the Russia–Ukraine shock, economies were still absorbing the after-effects of pandemic-era fiscal stimulus, supply-chain dislocations, and reopening demand.

- Policy & Sterling Implications

Expectations are for UK inflation to rise toward 3.5%–4.0% this year, roughly 1.5% above pre-war expectations, while growth weakens further. That is clearly uncomfortable for the BoE, but it does not automatically justify the degree of hawkish repricing currently visible in rates markets.

Instead, the more plausible policy response is for the Bank of England to pause rather than hike, choosing to look through the initial oil shock while focusing on whether medium-term inflation expectations and domestic inflation dynamics worsen materially. That would leave the BoE less hawkish than markets are currently pricing in, particularly if activity data continues to soften.

This matters for sterling. In the near term, higher inflation and rate-hike expectations can offer some support to the pound. However, if markets conclude that the BoE is unlikely to hike in line with market expectations and if growth continues to deteriorate, sterling could struggle. In that sense, the outlook for the pound is mixed: near-term inflation may provide temporary support, but a softer growth backdrop and a central bank reluctant to overreact to an external energy shock could ultimately prove pound-negative.

That said, further tightening cannot be ruled out, particularly if oil remains above $100 for months or even rises further. But for now, the more likely scenario is pause over panic — and that means markets may be running ahead of the BoE. The situation remains very fluid and could change dramatically over the course of three months.

- Domestic politics

While PM Kier Starmer’s position looked shaky at the start of the year, the war in the Middle East has deflected attention away from it. No one wants a leadership change amid soaring geopolitical uncertainty. That said, attention will also turn to the UK local elections in May, where the ruling Labour Party is behind the populist Reform and Green Parties in the polls. Disastrous local elections could once again raise questions over Kier Starmer’s ability to lead.

USD Q2 Outlook

The USD is entering Q2 on a firmer footing, supported by a combination of safe-haven demand, higher oil prices, and reduced expectations for Federal Reserve rate cuts. The main shift from earlier in the year is that the dollar is no longer trading solely on the interest rate outlook; it is increasingly being driven by geopolitical risk and relative US economic resilience.

- Safe haven demand

The biggest support for the dollar in Q2 is likely to come from the Middle East conflict and the associated rise in energy prices. As long as the Iran war continues and concerns around the Strait of Hormuz persist, risk sentiment will likely remain weak. In that environment, the dollar tends to benefit from its role as a safe-haven currency. At the same time, the U.S. economy is seen as less vulnerable to an energy shock than major energy-importing economies such as the eurozone, the UK, and Japan, given that it is a net oil exporter, which gives the dollar a relative advantage.

- Inflation

A second key pillar for the dollar is the Federal Reserve outlook. Before the Iran war, markets were pricing in around two rate cuts this year. However, the recent rise in oil prices has lifted inflation risks and boosted Treasury yields. As a result, investors have priced out rate cuts and consider that rates may need to stay higher for longer, supporting the USD.

That said, the dollar’s outlook is not one-way bullish. A lot of the recent strength has been driven by event risk, which means it could reverse quickly if there is a ceasefire, de-escalation in the Middle East, or a sharp fall in oil prices. In that scenario, safe-haven demand would likely fade, and markets could return to pricing Fed cuts later in the year, reducing one of the dollar’s main supports.

- Growth

There is also a second-stage risk for Q2. If oil remains high for too long, the market may shift focus from inflation to the potential damage to the US economy, which could eventually weaken dollar demand later in the quarter.

Overall, the most likely Q2 outcome is that the dollar remains firm to moderately strong, especially in the early part of the quarter. The bias remains USD-positive but is likely to stay highly headline-driven and sensitive to geopolitical developments.

GBP/USD technical analysis (weekly chart)

After breaking out of its symmetrical triangle pattern by rising above the falling trendline dating back to 2015, GBP/USD has been consolidating. The price has been capped on the upside at 1.38 and by 1.30 on the downside. More recently, the price has fallen below its 50 SMA, 1.34, which, combined with the RSI below 50, could keep sellers hopeful of further downside.

Sellers will need to take out support at 1.30, the round number and the rising trendline support. A break below here exposes the 200 SMA at 1.27. Below here, 1.21 comes back into focus, the 2025 low.

Should buyers push the price back above the 50 SMA, 1.38 would be the next resistance. A rise above here creates a higher high.