Microsoft (MSFT) earnings expectations are focused less on headline beats and more on execution across cloud growth, AI monetisation and margins. Consensus forecasts look achievable, but valuation sensitivity and crowded positioning leave the bar for a sustained positive reaction high.

MSFT is flirting with technical bear-market territory, but has yet to break the 20% drawdown threshold from its record high. That leaves scope for a near-term relief rally if earnings surprise to the upside, though a durable rebound likely requires clear evidence of Azure stabilisation alongside credible progress on AI monetisation.

View related analysis:

- Tesla (TSLA) Earnings Preview: Q4 Margins in Focus

- Apple (AAPL) Q4 Earnings Preview: Services in Focus as iPhone Growth Slows

- Meta (META) Q4 Earnings Preview: Facebook and Instagram Ads in Focus

- Trade to Watch 2026: Nasdaq 100 Correction Risk Before New Highs

Azure remains the core driver of the earnings narrative, but the debate has shifted from resilience to re-acceleration. Management commentary on AI monetisation, capex intensity and margin sustainability will therefore be closely scrutinised, particularly as markets grow more sensitive to capex-heavy, “spend now, payoff later” strategies.

Ultimately, investors are less interested in backward-looking EPS beats and more focused on whether Microsoft can justify its premium valuation as cloud growth moderates and AI investment accelerates.

With positioning crowded and implied volatility elevated, this earnings report has the potential to set the tone not just for MSFT shares, but for the broader Nasdaq and AI-exposed trade into the next quarter.

Microsoft (MSFT) Earnings Preview: What the Market Is Watching

- Cloud revenue growth, with Azure judged on stabilisation or re-acceleration

- AI monetisation, including Copilot uptake and evidence of billable demand

- Margins and costs, as cloud efficiency is weighed against AI and data-centre spend

- Productivity and PC demand, offering signals on enterprise and consumer conditions

- Guidance and outlook, particularly around Azure growth and AI revenue framing

- Capex intensity, and tolerance for ongoing “spend now, payoff later” investment

Revenue Growth — Cloud Still the Core Driver

Azure will determine the earnings reaction. The market is less concerned with whether Microsoft beats consensus and more focused on whether cloud growth has stabilised or is starting to re-accelerate versus the prior quarter.

The key question is whether demand is improving as optimisation cycles fade, or simply holding up. Commercial bookings and remaining performance obligations will be watched for forward-looking confirmation. FX effects are secondary — constant-currency Azure trends are what matter for price.

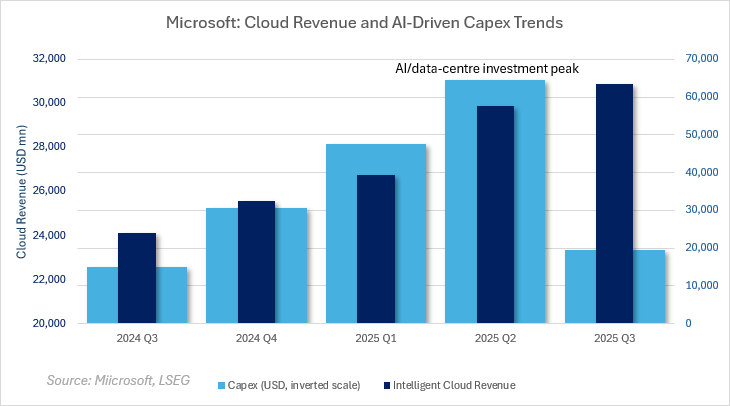

Source: Microsoft, LSEG

AI Monetisation — Signal vs Storytelling

AI remains central to Microsoft’s valuation, but the market now wants proof it is generating revenue. The focus is on whether AI is adding incremental sales and billable Azure demand, not just supporting product positioning.

Attention will centre on Copilot uptake across enterprise and consumer segments, whether adoption is paid or bundled, and whether AI workloads are showing up in Azure billing. Any early signs of margin pressure from AI-related capex will also be closely watched.

Margins — Cloud Efficiency vs Rising Costs

Margins remain a key sensitivity as Microsoft ramps AI and data-centre investment. The market will compare operating margins with the prior quarter to see whether cloud efficiency gains are offsetting higher compute, energy and infrastructure costs.

Investors will also benchmark Microsoft’s margin trajectory against peers. Any guidance on the timing of margin stabilisation or normalisation could matter given the stock’s premium valuation.

Productivity & More Personal Computing

Beyond cloud and AI, Microsoft’s productivity and PC segments provide signals on underlying demand. Office and Microsoft 365 pricing power will be watched for signs of enterprise resilience, while Windows OEM demand may indicate whether the PC cycle is stabilising.

LinkedIn results will be used as a read on hiring and advertising conditions. Gaming and Xbox remain secondary for near-term price action but relevant to the longer-term shift toward services.

Guidance and Outlook — The Real Catalyst

Guidance is likely to drive the post-earnings reaction. The market will focus on the tone of Q1 and full-year guidance, particularly around cloud demand and spending trends.

Investors will watch whether management explicitly addresses the Azure growth outlook and whether AI revenue expectations are framed quantitatively or remain qualitative. Confident guidance would support a more constructive reaction, while cautious language risks reinforcing concerns around growth durability.

Capex and Investment Spend

Capex guidance will be closely scrutinised as Microsoft continues to scale AI and data-centre investment. Markets remain sensitive to “spend now, profits later” narratives, particularly in a higher-for-longer rate environment.

Any indication that elevated capex intensity will persist longer than expected could weigh on sentiment, especially among multiple-focused investors. Clearer framing around returns on investment may help offset near-term margin concerns.

Microsoft (MSFT) Share Price Technical Analysis

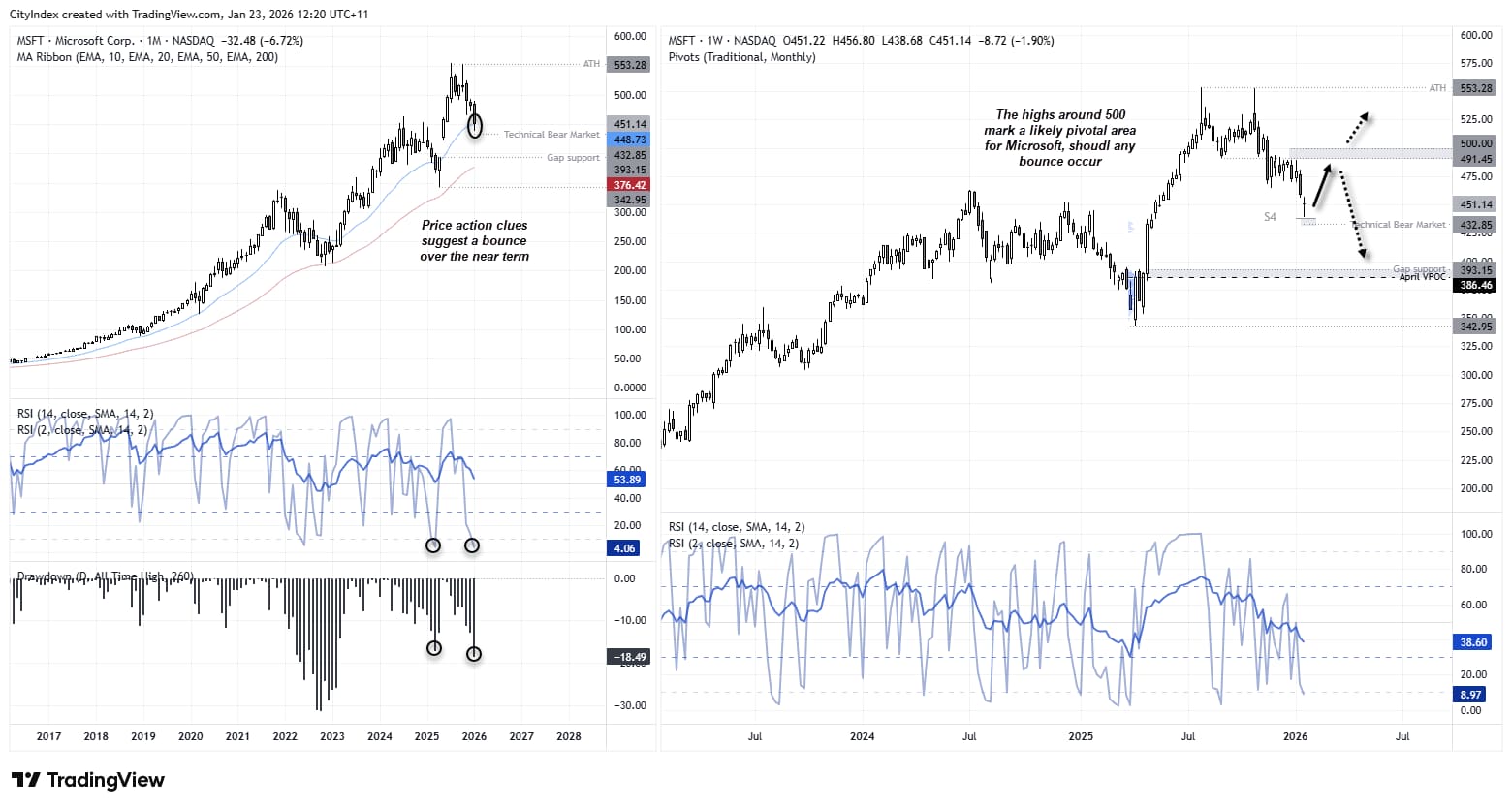

It has been six months since MSFT last reached a record high, marking the start of its current correction. The broader bullish trend remains intact while price holds above the 342.95 swing low, which still allows for meaningful downside without confirming a trend reversal. That said, there are early signs the stock may be due a near-term bounce.

On the higher timeframe, the monthly candle is attempting to hold above the 20-month EMA, while the monthly RSI (2) sits at an extremely oversold 4.06. The current pullback of -18.5% is also broadly in line with the -16.5% correction seen in March. With this week’s candle shaping up as a spinning-top doji, and its low precisely respecting the monthly S1 pivot — a level rarely tested — conditions are consistent with a short-term rebound. Prices are also approaching the technical bear-market threshold at 432.85, which may act as near-term support.

A more durable bounce, however, would likely require a clear earnings-driven upside surprise. Without that, any recovery risks stalling.

Source: Microsoft, TradingView

The bigger question is whether bulls can reclaim the 500 level. Failure to do so would leave MSFT vulnerable to another leg lower, with downside focus shifting to the 500 handle, 393.15 gap support, and the 386.46 VPOC. Reaching these lower levels would likely require a broader tech-led selloff alongside disappointing earnings from Microsoft.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade