Magnificent Seven, Nasdaq 100 Key Points

- For the Magnificent Seven, the AI capex cycle is increasingly colliding with the real world: debt markets, power grids, and regulation.

- This earnings season is no longer about whether AI is real, but whether the AI boom is entering a phase where these real world constraints will weigh on growth.

- time.

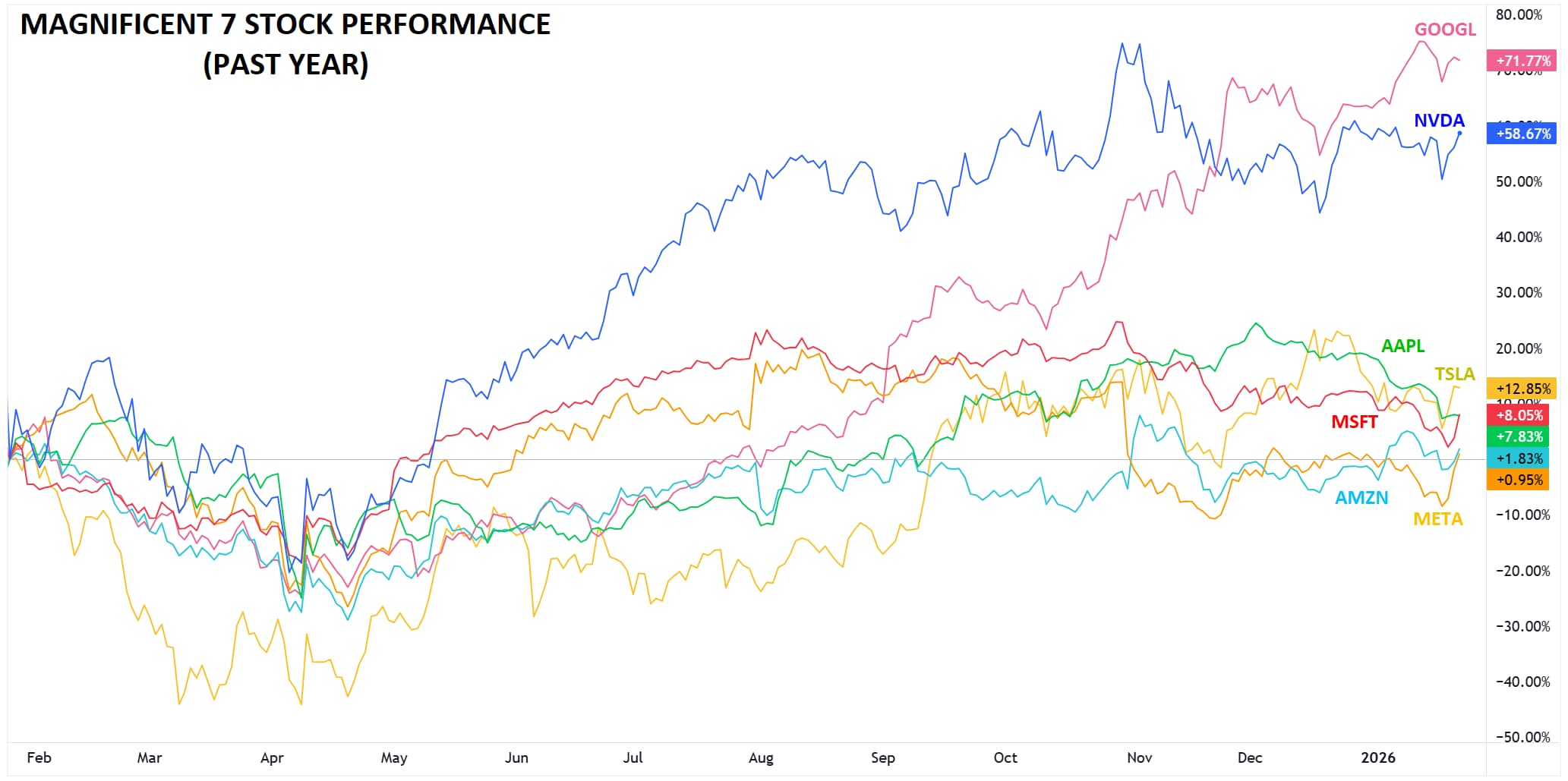

Over the last few years, the “Magnificent Seven” (Microsoft, Apple, Nvidia, Alphabet/Google, Meta/Facebook, and Tesla) largely marched together.

Entering the current reporting window, however, differences matter again: AI and cloud-attached firms are being rewarded for infrastructure and monetization momentum, while consumer-sensitive and ad-exposed companies are more dependent on demand resilience and margin leverage.

Source: TradingView, StoneX

Magnificent 7 Earnings “Cheat Sheet”

Below is a compact, sourced “cheat sheet” with the expected report dates (company announcements / calendars) and the commonly-quoted consensus EPS figures available publicly right now:

|

COMPANY |

Report date (local) |

Consensus EPS Estimate |

|

Microsoft (MSFT) |

Jan 28, 2026 |

~$3.86 EPS |

|

Apple (AAPL) |

Jan 29, 2026 |

~$1.73 EPS |

|

Meta Platforms (META) |

Jan 28, 2026 |

~$8.16 EPS |

|

Tesla (TSLA) |

Jan 28, 2026 |

~$0.44 EPS |

|

Alphabet / Google (GOOGL) |

Feb 4, 2026 (expected) |

~$2.30–2.58 EPS |

|

Amazon (AMZN) |

Feb 5, 2026 (expected) |

~$1.97 EPS |

|

NVIDIA (NVDA) |

Feb 25, 2026 (estimated) |

~$1.20–1.30 EPS |

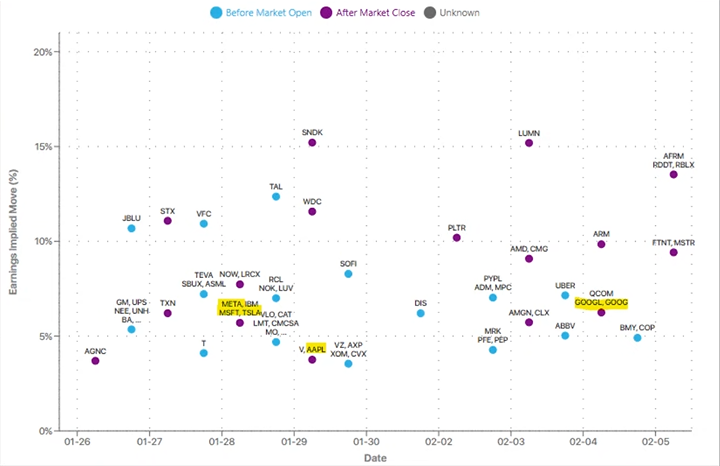

Options Implied Earnings Moves

“Magnificent Seven” Themes to Watch this Earnings Season

- The Ongoing AI Infrastructure Buildout

The first and biggest evolution is that the AI capex cycle is increasingly colliding with the real world: debt markets, power grids, and regulation. 2026 capex estimates for the largest “hyperscalers” is widely forecast to hit the $600B+ range, driven primarily by AI infrastructure. At the same time, major tech firms have leaned more heavily into debt issuance to fund the infrastructure race. This matters for earnings because the market’s attention is moving from “who spends the most” to “who can sustain the spend without eroding free cash flow,” especially if AI monetization takes longer than expected.

That financing story runs straight into the second constraint: power. Datacenter development is increasingly bottlenecked by grid interconnections, equipment lead times, and local permitting. In some markets, datacenters face multi-year grid connection delays, and energy dynamics are already becoming a political and economic story in their own right. In practical terms, this makes AI capacity a more delicate operational issue than the market may assume, particularly for the largest cloud platforms.

This is where Microsoft, Amazon, Alphabet and Meta will be pressed most directly. Azure in particular is under a microscope, with traders hyper-focused on whether growth is decelerating and how much of that is demand versus capacity. Amazon has signaled that capex is likely to remain elevated into 2026 as it expands cloud capacity, and that’s the type of forward guidance that can swing sentiment sharply depending on how confident management sounds about payback. For Meta, the advertising engine remains healthy (more below), but the company has openly framed 2026 as another year of heavy AI infrastructure investment, which keeps the “ROI debate” front and center.

- Digital Advertising

While AI infrastructure dominates the top of the agenda, digital advertising is quietly setting up as the second major swing factor. According to Dentsu, global ad spending is expected to rise 5.1% and surpass $1 trillion in 2026 for the first time, with algorithm-driven advertising comprising roughly 71.6% of total spend.

That’s supportive for Alphabet and Meta broadly, but the details will matter. Meta, for example, has emphasized the scale of short-form consumption and monetization progress, but it will also need to justify the investment surge supporting ad delivery systems. Amazon’s ad business remains the wild card and could again be the biggest advertising story inside the Mag 7 if spending holds up.

- Enterprise & AI Spending vs. Consumer Softness

A third theme is the omnipresent “two-speed economy,” with the dividing line between AI-accelerated enterprise demand versus discretionary hardware and autos.

Apple may have a difficult time spinning a strong narrative this quarter because the market is weighing strong iPhone cycle demand against margin questions from rising component costs. Tesla sits at the other end of the consumer sensitivity spectrum, with the market still focused on delivery momentum and the durability of automotive margins against intensifying competition. As usual, these companies’ guidance, more than what they report over the past quarter, will likely determine whether the market rewards their stocks this earnings season.

- Policy, Regulation & Geopolitical Overhang

Finally, regulatory and geopolitical risks continue to hover in the background. In addition to antitrust risks for Alphabet and Apple, Nvidia faces immense geopolitical risks. China-bound shipments of advanced AI chips face new complications every day, underscoring risks to its revenue. Any commentary on regional demand mix, export pathways, or customer behavior in response to restrictions could shape expectations for 2026.

Across the Magnificent Seven, this earnings season is no longer about whether AI is real, but more about whether the AI boom is entering a phase where capital discipline, power availability, and policy constraints will weigh on growth. Unlike past years, the companies that sound like they’re still in “build first, explain later” mode may find themselves in trouble as investors increasingly demand bottom-line profits rather than stories about the future.

Nasdaq 100 Technical Analysis: NDX Daily Chart

Source: Tradingview, StoneX

Ahead of earnings season, the tech-heavy Nasdaq 100 (of which the Magnificent 7 makes up more than 41% of the current market capitalization) continues to consolidate below 26,000. While other major US indices are on the verge of record highs, the NDX has lagged slightly behind in recent months, a notable change from the prior few years.

After forming a large “bullish engulfing candle” on the daily chart on Wednesday’s NATO tariff reversal by President Trump, the index has continued built on its gains to close the week in the mid-25,000 range. As long as this week’s low holds, it keeps the trend of “higher lows” intact and tilts the probabilities toward another test of the year-to-date highs just below 26,000, and potentially the record highs near 26,250 in time. Only a break below the 100-day MA (currently around 25,100) would shift the medium-term bias back to neutral.

-- Written by Matt Weller, Global Head of Research

Check out Matt’s Daily Market Update videos on YouTube and be sure to follow Matt on Twitter: @MWellerFX