The final GDP release rarely moves markets, but Thursday’s Q2 US growth figures proved an exception — much to the delight of US dollar bulls. GDP was revised up to 3.8% y/y from 3.3%, its strongest pace since Q3 2023. Consumer spending rose to 2.5% from 1.6%, while sales were revised up to 7.5% from 6.8%. Inflation also ticked higher in Q2, with PCE prices revised to 2.1%, core PCE at 2.6%, and super-core at 2.4%.

This has traders questioning the Fed’s rate-cut path. Fed funds futures still price an 85% chance of a November cut, but that’s down from near-certainty earlier this week. The odds of a December cut have slipped to 60%, while expectations of further cuts into 2026 have faded. Yields pushed higher across the curve, with the 2-year rising 7.3bp to 3.6% (more than double its 1-year daily average move of 3.5bp). The 10-year climbed 9.3bp and the 30-year added 9.5bp.

View related analysis:

- AUD/USD, AUD/JPY: Australian Dollar Diverges Against US Dollar and Yen

- US Dollar, Japanese Yen, New Zealand Dollar: COT Report Analysis

- Australian Dollar Outlook: AUD/USD Under Pressure Ahead of CPI and PMIs

Chart analysis by Matt Simpson - data source: TradingView

US Dollar Rally Fueled by Rising Yields and Short Covering

The US dollar was the strongest major, driven by a mix of short-covering and fresh long positions.

- The Japanese yen weakened for a second day, allowing USD/JPY to finally break out of its 38-day range, with bulls eyeing a move above 150

- USD/CHF rose for a second day, nearing 0.80. While the SNB kept rates on hold and is unlikely to return to negative rates, it reiterated its willingness to intervene in FX markets, providing support for USD/CHF

- EUR/USD slid back below 1.17, logging a second straight ~0.6% loss

- GBP/USD underperformed the euro, sending sterling to a 36-day low and EUR/GBP to a 44-day high

- The New Zealand dollar was the weakest major, with NZD/USD breaking below 0.58 to a 5-month low as RBNZ cut expectations resurfaced

- AUD/USD fell in line with my bearish bias from yesterday, hitting the 50-day averages. A break lower would bring 0.65 into play for bears

- USD/CAD gained for a fourth day, reaching an 18-week high

US Dollar Index (DXY) Technical Analysis

The 96 handle continues to provide solid demand for the US dollar index, having produced a key low in 2023 and twice again in 2025. A countertrend move now looks underway, but the question is how far it can extend. With the Fed unlikely to consider hikes at this stage, a full 6% rebound seems unlikely. Still, with traders net-short, the US dollar has scope for further upside in the near term.

A multi-week bullish divergence on the RSI (2) signalled the potential bounce, with two gravestone doji candles marking a double bottom around 96. While the RSI (2) has already pushed into overbought territory, bulls may prefer tighter stops, though the RSI (14) is curling higher and supports the case for a move towards the 50-week EMA (99.87).

A 100% projection of wave a from wave b lands near the recent cycle high and the 50-week EMA, creating a resistance cluster just below 100. A break higher would expose the 50-week SMA and the 138.2% Fibonacci projection near 102.

Given political pressure from the Trump administration for cuts, and the Fed’s reluctance to entertain hikes, the base case remains that any dollar gains are corrective rather than the start of a new uptrend.

Chart analysis by Matt Simpson - data source: TradingView U.S. Dollar Index Futures

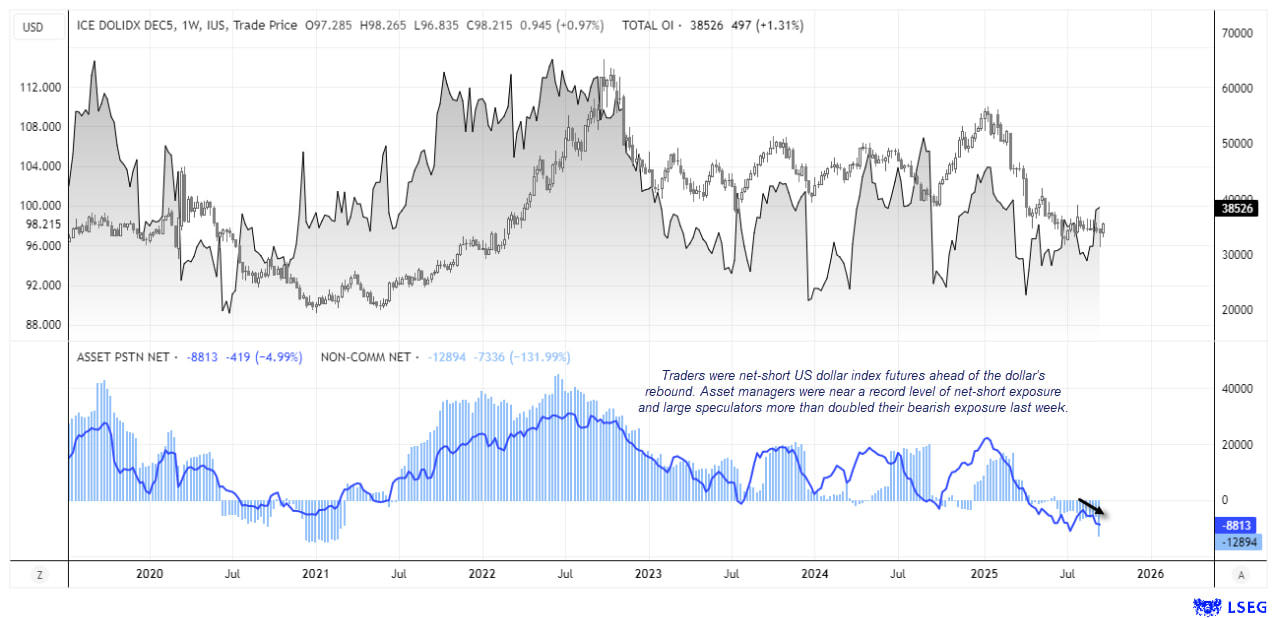

US Dollar Positioning (IMM Data): Weekly COT Report Analysis

The latest Commitment of Traders (COT) report shows that traders remain net-short on US dollar index (DXY) futures. Large speculators more than doubled their net-short exposure last week, largely due to heavy long liquidation, taking bearish positioning to a four-year high. Asset managers were also net-short by -8.8k contracts, close to a record level. Both groups appear on the wrong side of the trade, with Fed cut expectations being pared back and the US dollar staging a countertrend rebound.

Chart analysis by Matt Simpson - data source: IMM, CME, LSEG

Key Economic Events for Traders (AEST / GMT+10)

09:30 JPY CPI, Tokyo Core CPI, Tokyo CPI, CPI Tokyo Ex Food and Energy, Unemployment Rate (Sep) (USD/JPY, EUR/JPY, Nikkei 225)

09:50 JPY Foreign Bonds Buying, Foreign Investments in Japanese Stocks (USD/JPY, EUR/JPY, Nikkei 225)

15:00 SGD Industrial Production (Aug) (USD/SGD, EUR/SGD, STI Index)

15:30 JPY BoJ Board Member Noguchi Speaks (USD/JPY, EUR/JPY, Nikkei 225)

17:00 EUR Spanish GDP (Q2) (EUR/USD, EUR/GBP, DAX)

19:30 EUR ECB President Lagarde Speaks (EUR/USD, EUR/JPY, DAX)

20:00 EUR France Jobseekers Total (Aug) (EUR/USD, EUR/GBP, CAC 40)

22:30 USD Core PCE Price Index, PCE Price Index, Personal Income, Personal Spending, Real Personal Consumption (Aug) (S&P 500, Nasdaq 100, USD/JPY, Gold, Crude Oil)

22:30 CAD GDP, Wholesale Sales (Jul/Aug) (USD/CAD, EUR/CAD, CAD/JPY)

23:00 USD Dallas Fed PCE (Aug), FOMC Member Barkin Speaks (S&P 500, Nasdaq 100, USD/JPY)

00:00 USD Michigan 1-Year Inflation Expectations, Michigan 5-Year Inflation Expectations, Michigan Consumer Expectations, Michigan Consumer Sentiment, Michigan Current Conditions (Sep) (S&P 500, Nasdaq 100, USD/JPY)

01:00 CAD Budget Balance (Jul) (USD/CAD, EUR/CAD, CAD/JPY)

01:30 USD Atlanta Fed GDPNow (Q3) (S&P 500, Nasdaq 100, USD/JPY)

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade