- Energy driving USD/JPY, moving near lockstep with crude

- Peace talks between the US and Iran key for direction this week

- Progress tils directional risks lower, deterioration higher

- Intervention risk elevated as yen weakness and JGB yields rise together

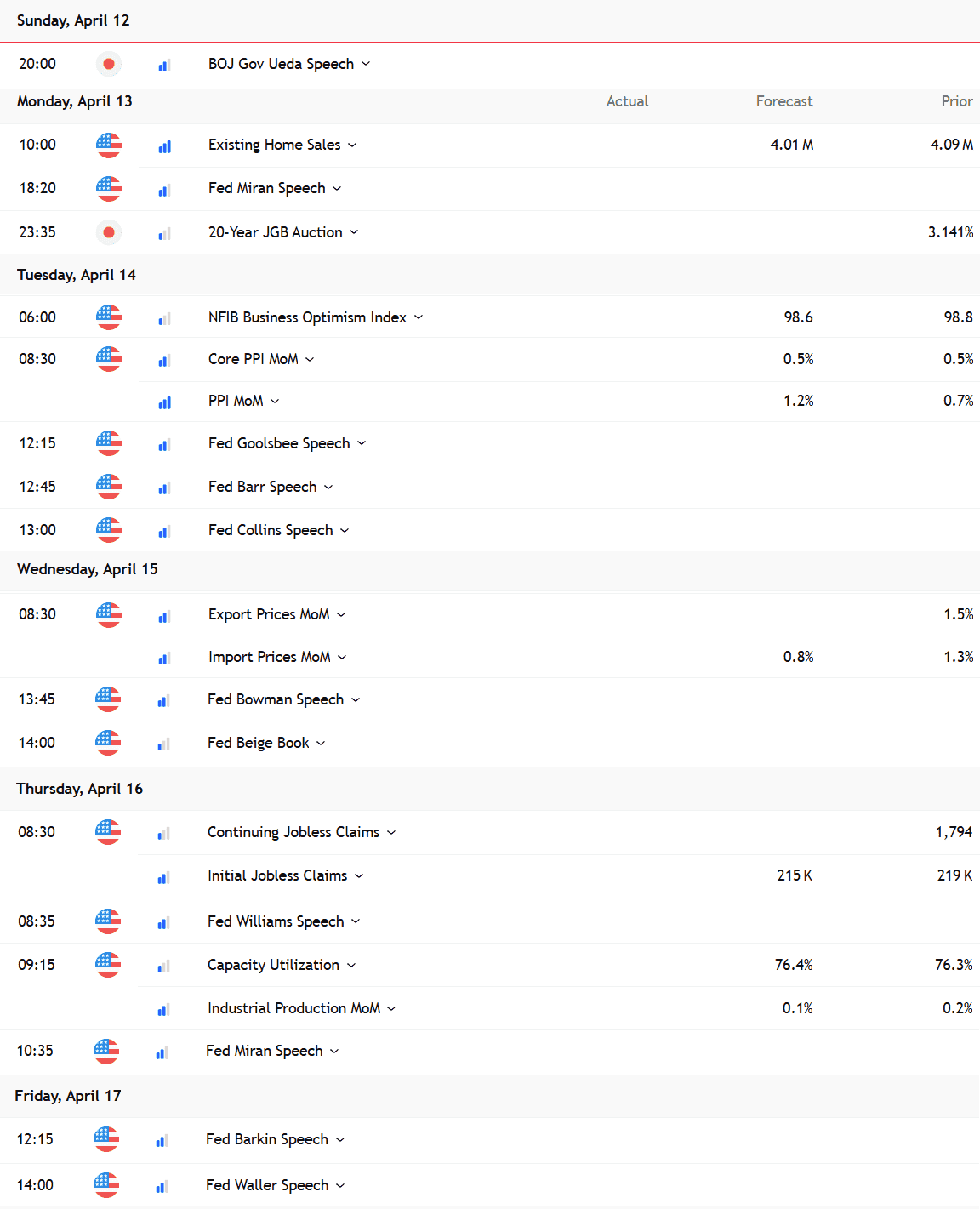

- Economic calendar largely irrelevant

Summary

USD/JPY is being driven by energy prices, not rates, with BoJ intervention risk the only meaningful counterweight as pressure builds on Japan’s bond curve. The economic calendar is largely irrelevant in this environment, leaving direction tied to developments in oil and geopolitics. The pair finds itself consolidating near the March highs, with a slight downward bias emerging within the broader long-run uptrend.

Oil now the primary signal

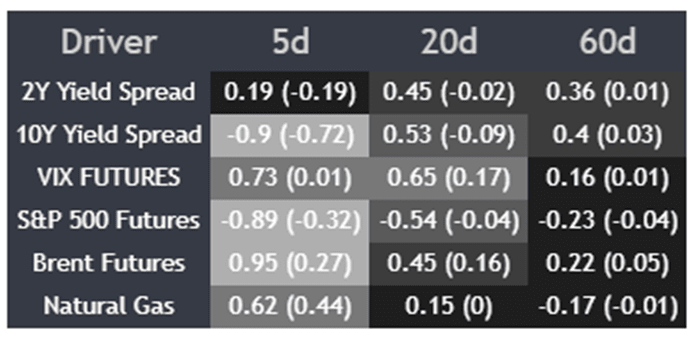

The correlation matrix below reinforces the dominance of energy markets on movements not only in USD/JPY but broader markets over the past week. A 0.95 correlation with Brent is essentially lockstep, indicating Japan’s vulnerability as a major energy importer remains the dominant theme.

Source: TradingView

The reasonably tight relationship with VIX futures is also linked back to energy, with higher oil prices often driving higher volatility lately, reflecting developments in the Persian Gulf. The same is evident in the very strong inverse relationship with S&P 500 futures, the opposite relationship to what you’d expect from a funding currency for carry trades. The yen is weakening as volatility rises and risk assets wilt, not rallying as has been the historic relationship.

The same also applies for 10-year spreads between the two nations, with the strong negative correlation the polar opposite to what you’d expect in a rates-driven regime.

The overarching message is clear: energy prices are dominating. That puts developments around peace talks between Iran and the US in Pakistan, scheduled to begin this weekend, firmly in focus as the key catalyst for USD/JPY this week. Progress should see the pair move lower, while any deterioration risks another push higher.

Intervention risk is essentially the only other thing traders should be on the lookout for.

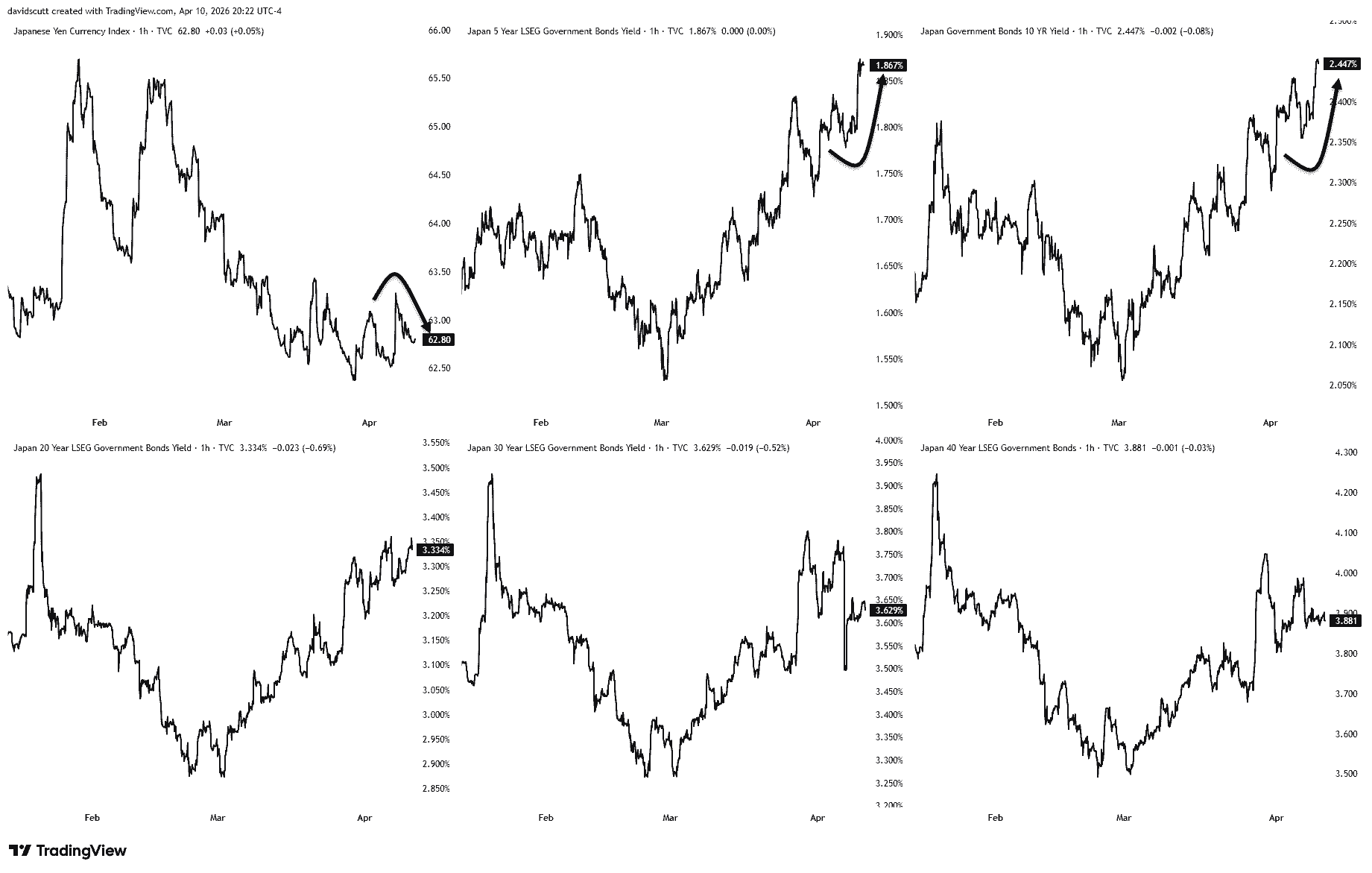

JGB curve, yen signal inflation concern

Even as sentiment towards a resolution in the Iran war improved noticeably towards the end of last week, markets continue to pressure JGBs and the yen (top right pane) simultaneously.

Source: TradingView

While the most acute weakness last week was concentrated in shorter-duration debt, indicating concerns may be shifting towards inflation rather than Japan’s economic and fiscal outlook that hammered the ultra-long end at times in March, the message is unchanged. The market is still telling policymakers that monetary policy needs to be much tighter to account for the risk of prolonged inflation, or the release valve will come through a weaker yen.

Even with April heavily favoured for a BoJ rate hike and another priced by year-end, a 1.25% overnight rate would still be deeply negative relative to the inflation outlook. You can see the pressure in the 5-year and 10-year tenors, with yields pushing to fresh highs again last week even with sharply lower energy prices.

The market is speaking and Japan’s finance minister, Satsuki Katayama, needs to listen. She was on the wires again on Friday, warning that authorities stand ready to take decisive action on “all fronts” against speculative moves across crude, oil futures and FX.

Even with the elevated threat of intervention, trying to curb yen weakness risks placing even greater upward pressure on yields than what is already being seen. If intervention comes without a shift in fundamentals, it risks looking like a band-aid solution.

Selling foreign reserves to buy yen would be far more effective in an environment where the dollar is on the back foot, so be alert to that risk if USD softens on developments in the Gulf. If intervention comes when the dollar is in demand, it risks being faded quickly.

Outside of intervention risk, as long as crude prices remain in the driving seat, it leaves the economic calendar largely redundant for anyone other than financial journalists looking for something to write about beyond the gyrations in energy markets.

Data takes a back seat

Source: TradingView

The events calendar is essentially irrelevant. If markets barely bat an eyelid to the US CPI report last Friday, it leaves the calendar this week looking meaningless for anyone seeking signal.

US PPI on Tuesday is the only release of note, offering some insight into the passthrough of higher energy and tariff rates to upstream prices. Beyond that, it’s a wall of Fed speakers, with Williams, Bowman and Waller likely to draw the most attention.

US reporting season will also get underway, with many of the big banks reporting first-quarter earnings, although history suggests these updates rarely generate major volatility for broader indices and risk appetite given the high prevalence of beats typically seen.

In Japan, BoJ Governor Ueda kicks things off on Monday in Asia, although his recent remarks have tilted towards priming the market for another hike in April. Any deviation from that view would be unusual, but given the geopolitical backdrop, it’s the environment where we should expect the unexpected.

The 20-year JGB auction also deserves passing interest given the pressure on Japanese bonds. Weak demand could add to the pressure on both JGBs and the yen.

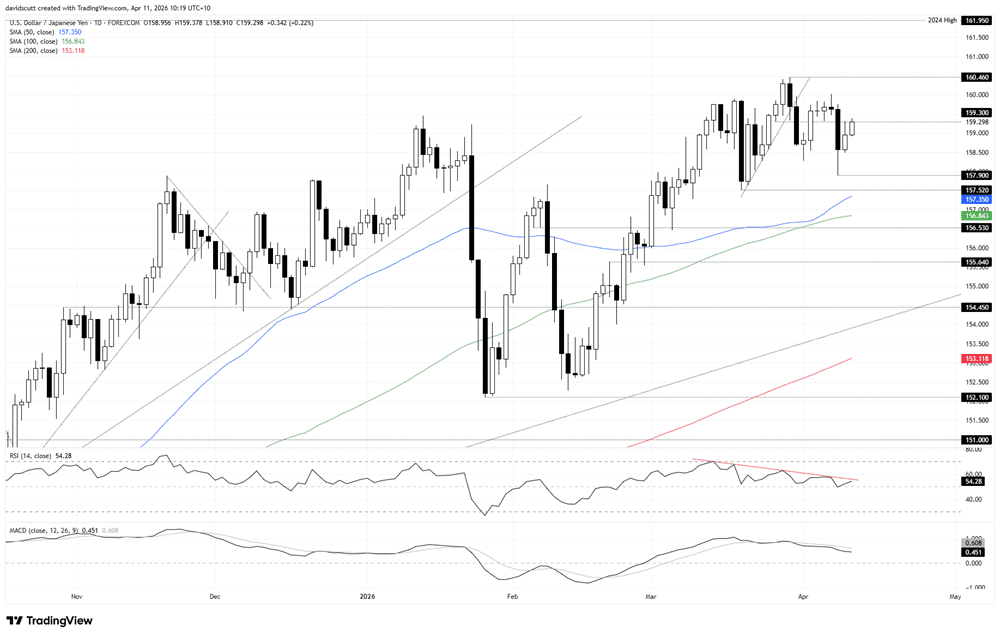

USD/JPY consolidates near highs

Source: TradingView

USD/JPY is consolidating near multi-decade highs following the breakdown of the bullish trend that began in February, likely reflecting not only the threat posed by intervention from Japanese officials but also no further deterioration in the situation in the Gulf, at least at the time of writing.

There is a slight downward bias to the price action, as seen in the lower highs and lower lows that have printed since the latter parts of March. That’s also reflected in the oscillators, with RSI (14) and MACD trending lower, pointing to a gradual easing in upside pressure, but not yet at levels that would shift the bias towards the downside.

With the key 50, 100 and 200-day moving averages still positively sloped and the longer-running uptrend firmly in place, buying dips towards 157.52 and selling rallies towards 160 remains the preferred approach for now. 159.30 sits in between as a reference level, having acted as both support and resistance recently. It looms as a level to build trades around should we not see an opening gap on Monday.

If 157.52 were to break on the downside, it would tilt directional risks lower, bringing the 50 and 100-day moving averages into focus at 156.53, along with support ahead of 155.50. On the topside, a break and hold above the March high of 160.46 would bring 161.95 into play for those willing to push aside the threat of intervention.