- Price action offers little guidance as drivers shift

- Bond markets are pricing a sharper slowdown

- Risk assets pin hopes on rate cuts to offset growth risks

- Payrolls data now the key macro catalyst

- Downside risks build if growth disappoints

Summary

Regimes are shifting by the day and USD/JPY has become increasingly difficult to read. While price action remains compressed, the bond market is sending a clear warning on growth. If US labour data validates that signal, the downside risks for carry trades may start to crystallise.

An Unstable Trading Environment

Over recent weeks, USD/JPY has been anything but easy to trade. Regimes appear to be shifting by the day rather than over longer periods where it is possible to develop a clear sense of what matters and what does not. Price action has offered little guidance, and momentum signals have not helped much in assessing directional risks.

The economic calendar has not provided much clarity either. Last week’s rally was driven largely by unverified BOJ speculation leaked to the media rather than hard data or a durable shift in macro fundamentals.

For that reason, this report takes a slightly different approach.

In analysis published yesterday, I outlined why I believe the fundamental risks for USD/JPY are increasingly skewed to the downside. Signals from the US Treasury market are becoming more consistent with a sharp slowdown in growth, a dynamic that could amplify pressure on carry trades as technology leadership stalls and cyclical outperformance begins to wobble. That analysis can be found here.

With that in mind, it is worth looking at how USD/JPY has been trading beneath the noise.

Risk Appetite or Rate Differentials?

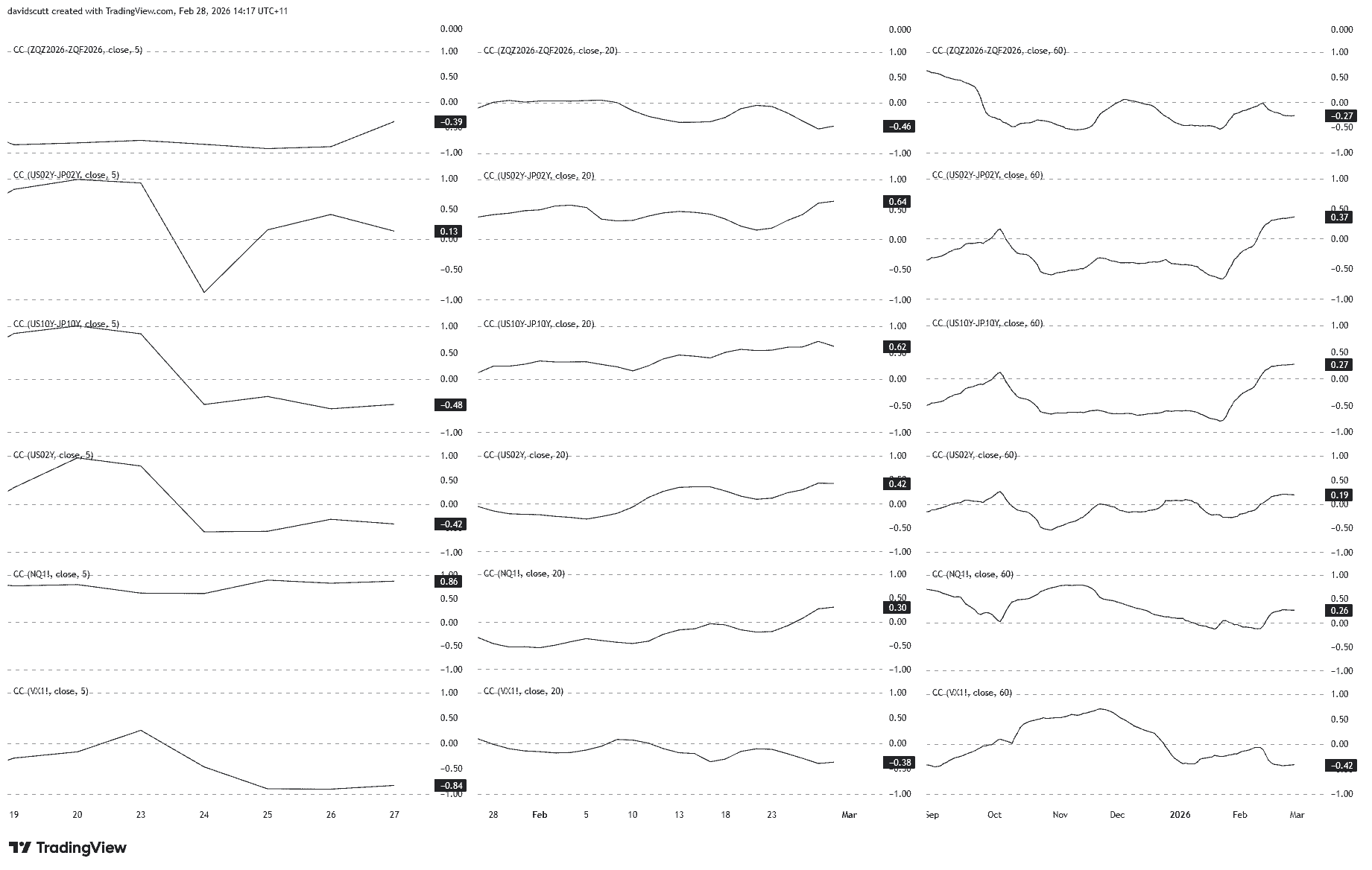

The graphic below shows rolling correlations between USD/JPY and several key macro drivers: Fed rate cut pricing for 2026, US-Japan two-year and 10-year yield spreads, US two-year yields, Nasdaq futures and VIX futures. The relationships are measured over five, 20 and 60 trading days from left to right, allowing a comparison between very recent moves and more established trends.

Source: Tradingview

The short-term picture is messy. Over the past week, the strongest correlations have been with Nasdaq futures and VIX, pointing to risk appetite as the primary driver. Yet the price action does not line up neatly with that conclusion. Nasdaq slipped and volatility rose late last week, but the yen still weakened. That is not a clean risk signal, and month-end flows may have played a role.

Stretch the horizon to 20 days and the message looks more coherent. USD/JPY shows a clearer positive relationship with US-Japan two-year spreads and US two-year yields, and a negative relationship with volatility. Front-end rate differentials and risk appetite still matter, even if the magnitude of recent swings makes the signal harder to trust.

Over 60 days, correlations soften again. The broader takeaway is not that drivers have disappeared, but that conviction in any single regime is lower than usual.

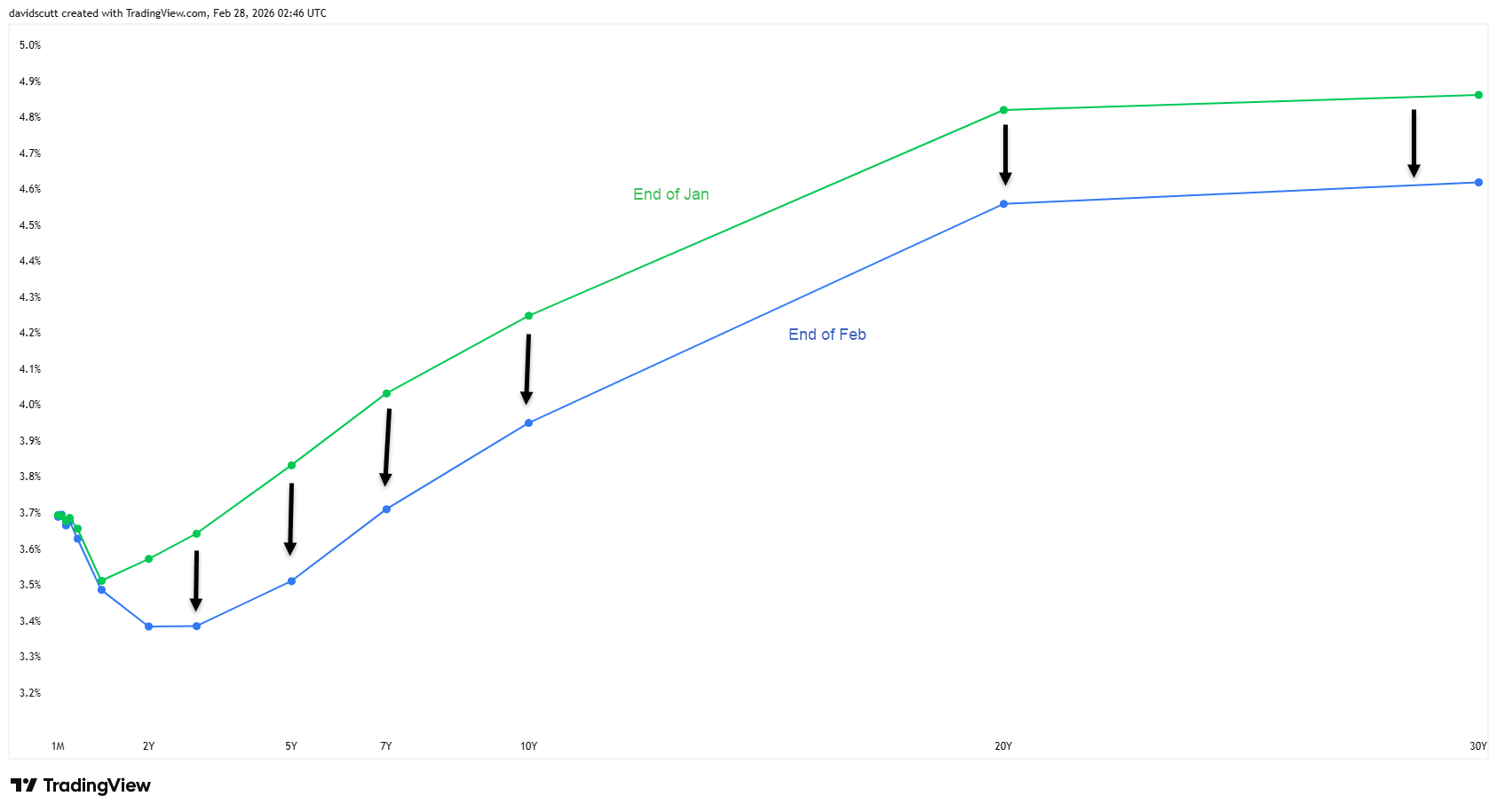

When the Curve Sends a Warning

To understand why my downside thesis for carry trades faces a meaningful test this week, it is worth looking at what has happened in the US Treasury market over the past month.

Source: TradingView

The move has been significant. The curve has bull flattened aggressively, led by a sharp decline in longer-dated yields. That type of shift is not usually associated with confidence in the growth outlook. It suggests markets are marking down medium-term nominal growth expectations rather than simply reacting to short-term volatility.

If that signal proves correct, the implications extend beyond a routine cyclical slowdown.

A cyclical soft patch can often be stabilised with rate cuts. A more structural moderation in growth is harder to address. If AI-driven efficiency gains translate into widespread job displacement rather than broad-based productivity-led income growth, the drag on demand could prove more persistent.

Source: TradingView

What is striking is that traders outside the bond market appear to be leaning on the idea that rate cuts will offset those risks. On Friday, despite a much hotter-than-expected January PPI print, rate cut pricing increased rather than declined. Markets are effectively betting that easier policy will be sufficient to cushion any slowdown. That assumption may prove optimistic if the bond market is right.

If rate cuts are being priced as the solution, this week’s activity data will determine whether that confidence is justified.

Growth in Focus, Not Inflation

Source: TradingView

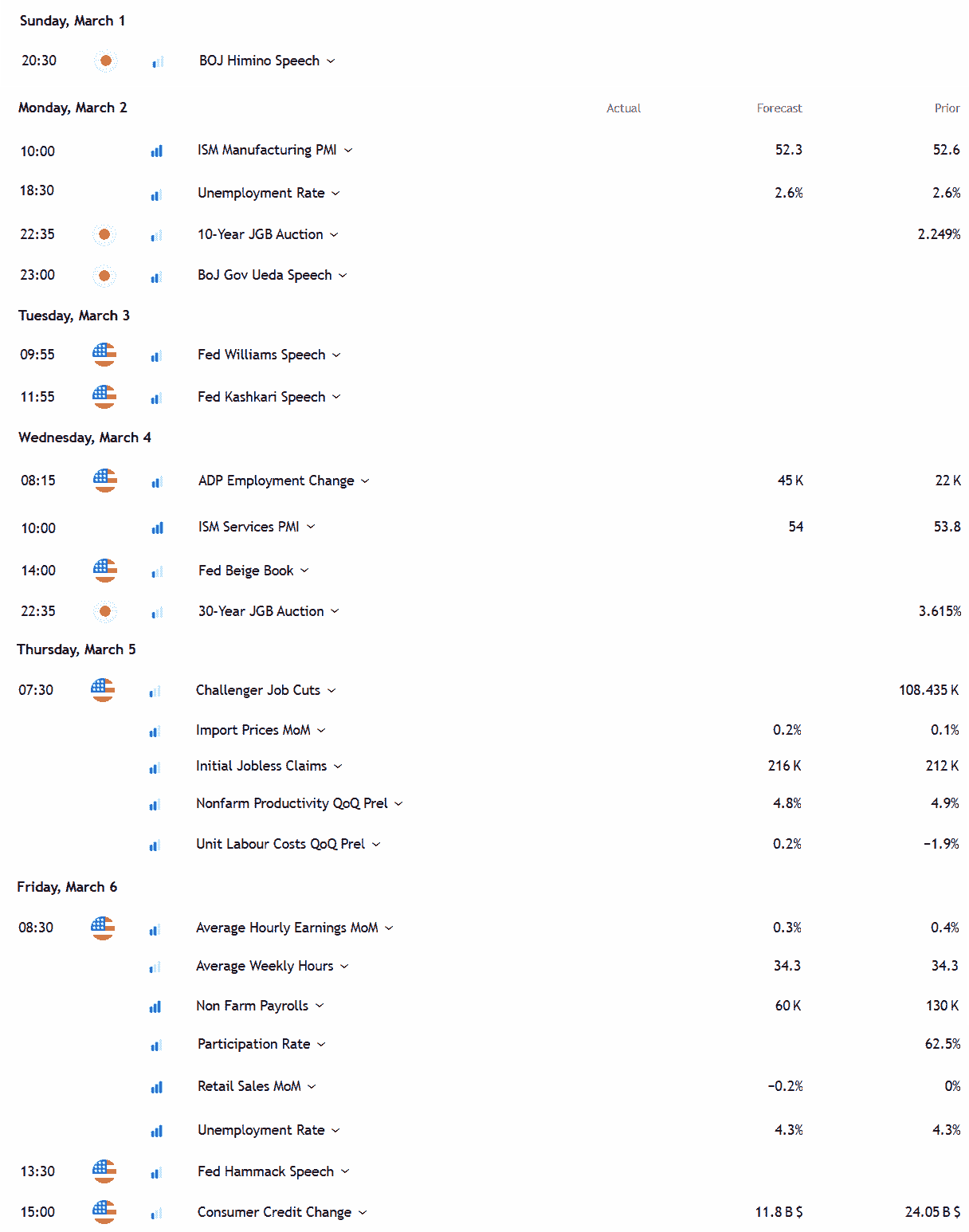

As close to a real-time read on the economy as markets get, the February ISM manufacturing and services reports may attract more attention than usual. This time, it is not the price components that matter most. It is the employment and forward orders measures. Markets are fretting about growth, not inflation. If hiring intentions soften or new orders roll over, that would reinforce the bond market’s message.

Before payrolls, ADP will be worth watching given it captures private sector employment trends. In the current environment, any evidence of job shedding at larger firms may attract particular scrutiny, especially as they are more likely to have advanced AI infrastructure already in place. Challenger job cuts will also draw attention for similar reasons.

Markets will also receive fresh information on wage pressures and nonfarm productivity. In theory, AI-led efficiencies should show up in stronger productivity. The question is whether that improvement is being driven by output gains or cost cutting.

The true test of the thesis arrives on Friday with nonfarm payrolls and retail sales. In the current macro backdrop, decent data would likely be welcomed by risk assets and could assist USD/JPY by easing slowdown concerns.

But if the data disappoints, that is where the downside thesis begins to face real validation.

Traders tend to focus on the payrolls headline, though it has been prone to revisions and noise in recent years. The unemployment rate arguably offers a cleaner read on underlying labour market conditions.

Cleveland Fed President Beth Hammack is scheduled to speak after both reports are released. If the broader Fed wishes to shape the narrative, she may be the messenger.

Japan’s calendar will likely play second fiddle on the surface. However, recent experience suggests BOJ communication cannot be dismissed entirely. Despite recent remarks from Ueda and Himino, the risk of surprise remains. Auctions of 10 and 30-year JGBs will also be watched, particularly after earlier concerns about Japan’s fiscal position contributed to yen weakness.

Iran Talks and Escalation Risk

Geopolitical risk also remains in the background. Talks between the United States and Iran are scheduled again this week, although speculation persists that military action could occur as soon as this weekend. Similar flare-ups in the past have tended to generate only limited and short-lived market reactions unless they escalated into something more sustained.

For USD/JPY, the implications are mixed. A prolonged disruption to energy supply would typically favour dollar strength and yen weakness, reflecting the United States’ energy self-sufficiency and Japan’s reliance on imports. However, a sharp deterioration in broader risk sentiment would likely trigger defensive positioning and carry trade unwinds, a backdrop that has historically supported the yen.

Unless tensions escalate materially and begin to weigh heavily on global risk appetite, the impact on USD/JPY may prove limited beyond any initial knee-jerk reaction.

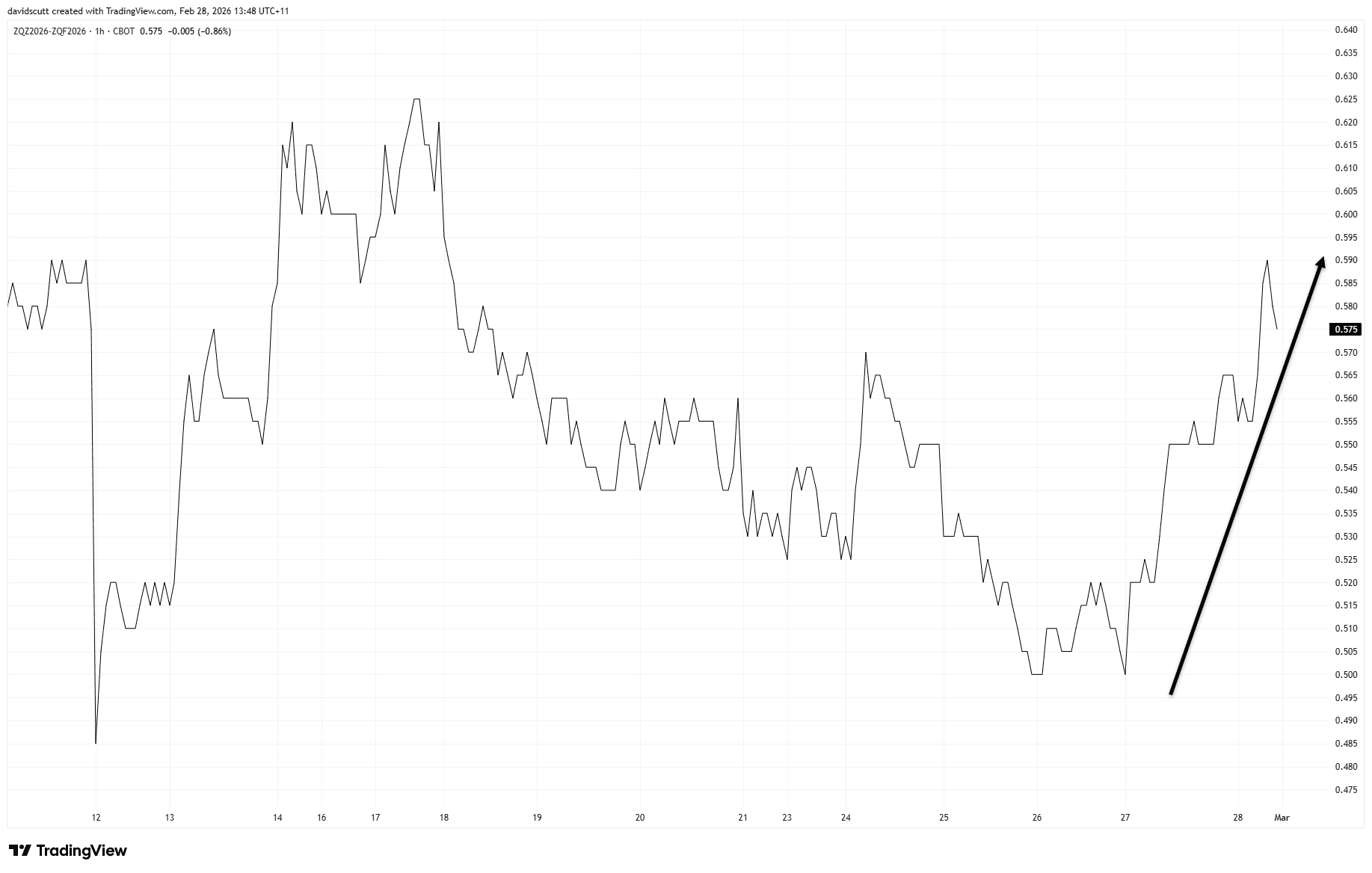

Compression Awaits Resolution

Source: TradingView

The daily chart continues to show a compressing structure of lower highs and higher lows. The market remains in a tightening range, even though the trendlines have been removed for now.

From a fundamental perspective, I suspect the eventual break is more likely to be to the downside. However, recent weeks have been a useful reminder to stay humble. Regimes have shifted quickly, and conviction has been costly. An open mind is required.

The oscillators are neutral, offering no strong directional clues.

On the topside, a break above 157.50 would end the sequence of lower highs, putting bulls back on the front foot and opening the door for a retest of the January high at 159.45.

On the downside, the price bounced on Friday from the intersection around 155.65 and uptrend support, making that the near-term zone to watch. A sustained break below would shift focus to 154.45, 154 and then 152.50, where several key trendlines converge.