- Energy shock worsening Japan’s economic and fiscal outlook

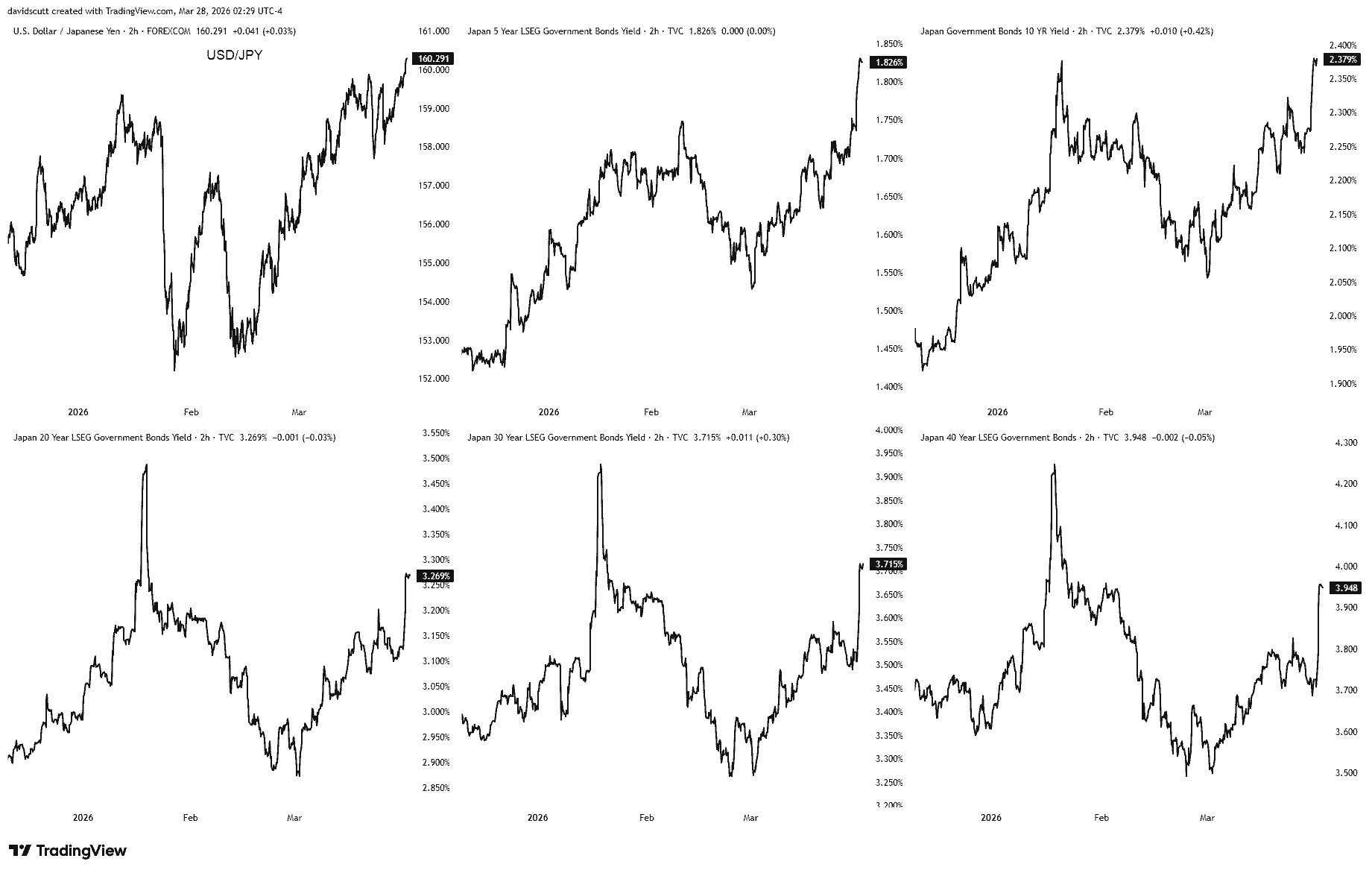

- Yen weaker and JGB yields rising as markets force adjustment

- Policymakers trapped between FX intervention and higher yields

- US rate pricing starts to roll over ahead of key data

- USD/JPY breaks to multi-year highs, but intervention risk is rising

Summary

USD/JPY continues to grind higher despite elevated intervention risk, pressuring both the yen and Japanese bonds given elevated economic and fiscal risks. Markets are pushing for a larger adjustment in yields, otherwise the yen needs to weaken further, leaving Japanese policymakers stuck in a bind where acting on one side risks destabilising the other. With markets continuing to price the risk of Fed hike and key payrolls data ahead, the trend remains higher, but so too is intervention risk.

Yen falls, JGB yields rise as policy trap deepens

The longer the Iran conflict constrains global energy supply, the greater the downside risks to Japan’s economic and fiscal outlook. As a major importer, higher oil and LNG prices worsen its terms of trade position, lifting import costs while weighing on real incomes and activity.

That’s how markets see it. Inflation rises on imported costs while growth weakens, tightening conditions as demand softens.

Fiscal risks build alongside it. Weaker activity and higher energy costs put pressure on the outlook, not just through potential support measures, but through the hit to growth itself.

Source: TradingView

The market is acting to account for those risks, and it’s doing so through both Japan’s FX and fixed income channels.

What we’re seeing is simultaneous pressure on the yen and JGBs, with USD/JPY pushing higher while yields across the curve move up, particularly at the long end. This isn’t a one-sided move. It’s the market repricing as the outlook deteriorates.

The message is clear. As those risks build, markets are saying bond yields need to rise far more to compensate investors, especially at the long end where uncertainty around inflation and fiscal sustainability sits. If yields don’t adjust enough, the yen becomes the release valve instead, weakening to account for the risks.

Right now, markets are leaning towards both, lifting yields while pushing the yen lower at the same time. And that’s a problem policymakers.

Intervening to support the yen risks shifting the pressure into bonds, pushing yields higher as markets demand greater compensation to hold JGBs. On the other hand, if the BoJ leans harder on bond purchases to contain yields, it risks accelerating yen weakness by adding liquidity and widening rate differentials.

Acting to address one doesn’t ease the pressure, it just shifts where it shows up. It’s essentially a game of whack-a-mole. Push down on one, and the other pops right back up.

With a virtual G7 meeting scheduled for March 30, it seems unlikely Japan’s Ministry of Finance (MoF) would instruct the BoJ to intervene to support the yen ahead of that. There’s also a question over whether intervening in the yen would be wise given how fragile Japanese equities and broader risk appetite already look. Nikkei futures are pointing to a sharp drop to start the week, and a stronger yen would only add to the pressure on firms with significant offshore earnings.

There’s also carry trade considerations. While there’s been little evidence of disorderly unwinds so far, borrowing costs in yen are rising and asset valuations are under pressure. A sudden move stronger in the yen risks acting as a tipping point, making it more expensive to unwind positions back into the currency, pressuring existing positions.

That leaves policymakers with a difficult decision. Despite Japanese finance minister Katayama signalling late last week a real risk of yen intervention, the safer path may be for the BoJ to step up JGB purchases to contain yields. Yes, it would likely place additional pressure on the yen, but help cushion equities and support bond prices, and may prove more effective than trying to push back against fundamentals through outright FX intervention.

Energy and US rates amplify upside pressure on USD/JPY

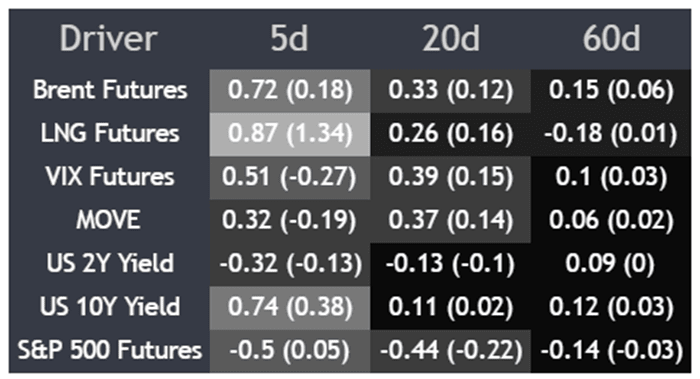

The correlation matrix below provides clear evidence of what’s driving USD/JPY higher right now. The pair remains primarily led by energy and rates, particularly over shorter horizons.

Source: TradingView

Over the past week, the relationship is strongest with energy. Brent futures show a correlation of 0.72, while LNG futures are even tighter at 0.87, pointing to a very strong positive link between higher energy prices and yen weakness. US 10-year yields are also highly correlated at 0.74, reinforcing the role of rate differentials.

At the same time, the pair is negatively correlated with equities, with S&P 500 futures at -0.50. That’s the opposite of what you’d expect if this were a pure risk-on, risk-off move. There is still a mildly positive relationship with implied US stock and bond volatility, but it’s not the dominant driver. Looking further out, those relationships moderate but remain in place.

Taken together, this is not a pure risk-driven move. Energy and rates are doing damage, especially in the near term. However, there are early signs that pressure from the US rates side may be starting to ease.

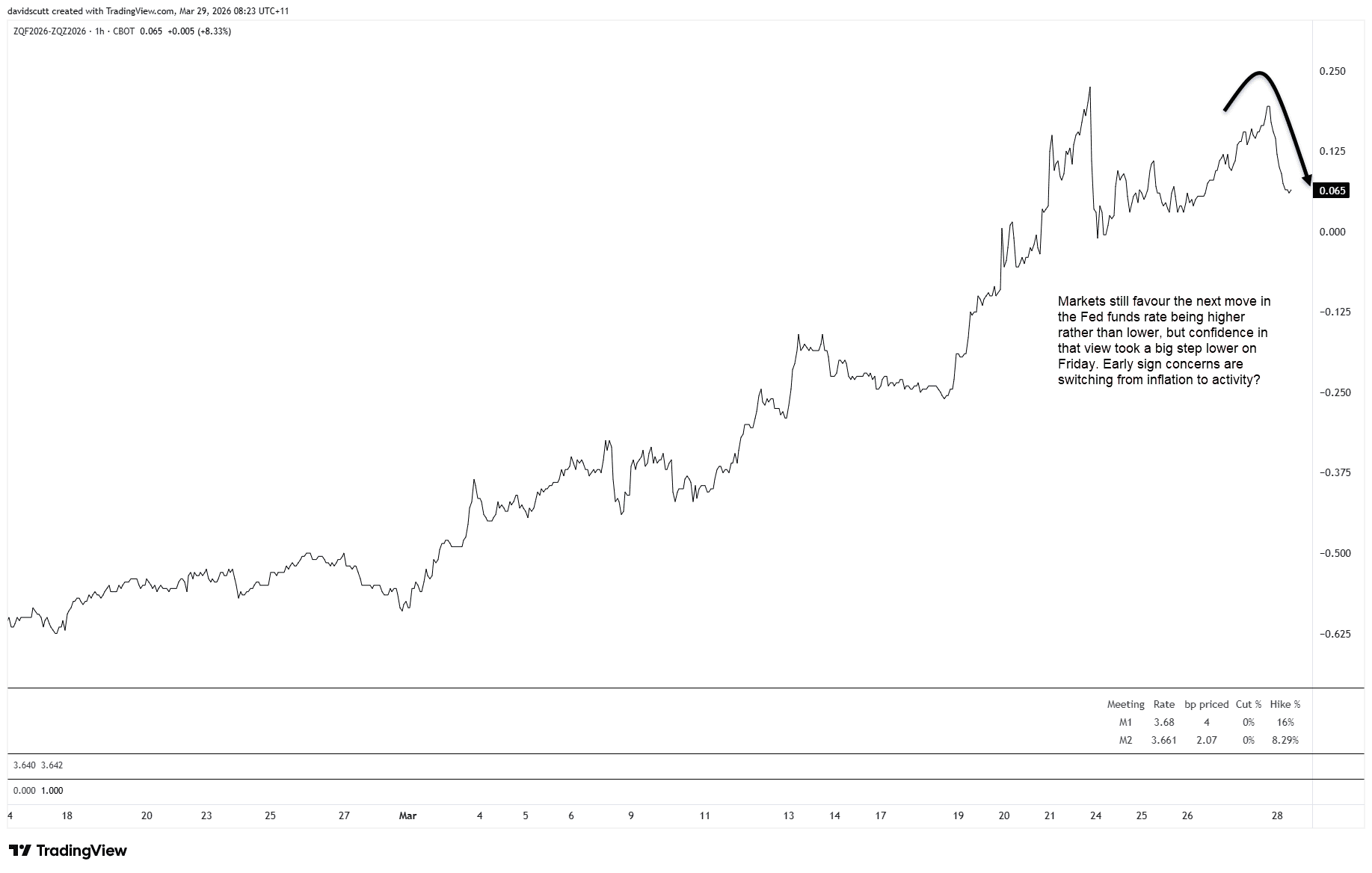

Fed hike pricing eases as growth concerns build

Source: TradingView

Fed pricing shifted sharply late last week. A full hike this year was close to being priced at one point, but that unwound hard into Friday's close, leaving just 6.5 basis points of tightening.

Set against moves in other inflation-linked markets, it suggests we may be seeing early signs that concerns are shifting away from inflation and towards demand destruction. If that shift builds, it could start to cap US yields, potentially easing some of the upward pressure on USD/JPY.

Key Payrolls, Tokyo CPI data to challenge rate outlooks

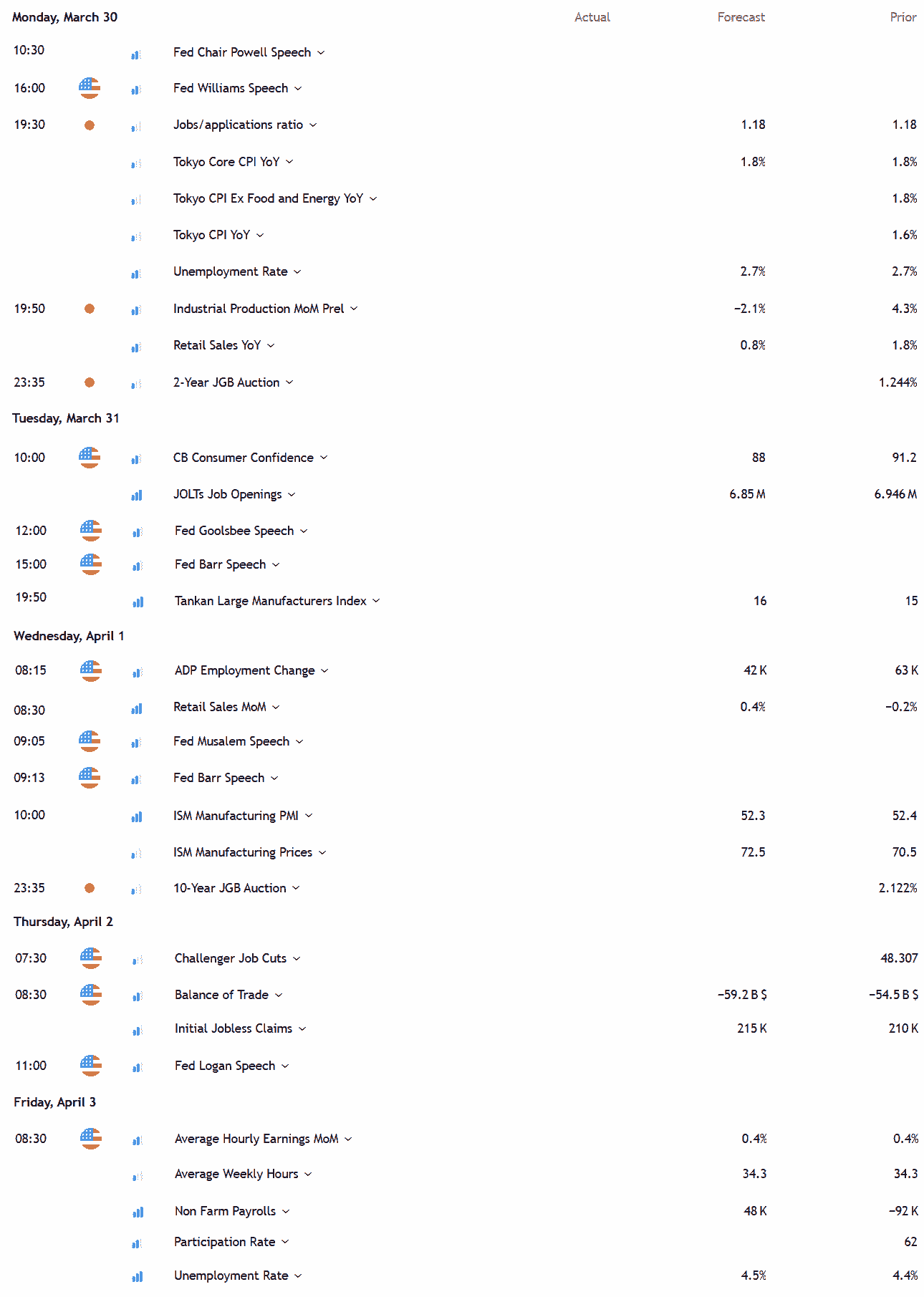

While the Iran conflict has made the policy implications from economic data near redundant, that may not be the case this week, with several key indicators scheduled that could meaningfully alter the rates outlook in both countries.

Source: TradingView

In the US, the key release is March non-farm payrolls. Strength would exacerbate inflation concerns, while weakness could see demand destruction fears take control. Retail sales will also be important in that context, along with the ISM manufacturing PMI which may offer early insight into how the war is impacting the industrial sector.

In Japan, the Tokyo CPI report is key. Being for March, it should provide the first glimpse as to whether higher energy prices are starting to feed into inflation. The 10-year JGB auction also warrants attention given the existing pressure on Japanese bonds.

USD/JPY upside bias intact despite intervention risk

Source: TradingView

If not for elevated intervention risk, the message for USD/JPY continues to be that the path of least resistance is higher.

We saw a clean bullish breakout from an ascending triangle on Friday, with the pair closing above 160.23, a level from which the BoJ was instructed to intervene in 2024. It’s the nearest focal point for traders early in the new week.

Overhead, 161.95 is the level bulls will be targeting, coinciding with the 2024 peak struck before another BoJ intervention episode. Beneath 160.23, 159.90 previously acted as resistance and may now flip to support, with the March uptrend and 157.88 other levels to watch.

With the 50, 100 and 200-day moving averages all sitting below the price and trending higher, the preference remains to buy dips over the longer term. A similar message is coming from the oscillators in the near term, with RSI (14) pushing higher above 50 but not yet overbought. MACD has also confirmed the move, staging a bullish crossover in positive territory late last week.

All favour an upside bias, absent any escalation in intervention risk.