Last week’s Commitment of Traders (COT) report revealed a widening divergence in positioning across major currencies. The US dollar extended its rally despite near-record net-short exposure from asset managers. Meanwhile, euro bulls grew more confident, and Australian dollar bears backed off following the RBA’s surprise rate hold. Positioning in JPY, CAD, and crude oil remained weak, while sentiment across risk indices like the S&P 500 and VIX remained net-long. Here’s the detailed breakdown.

Weekly Market Positioning Overview – COT Report Highlights (8 July 2025)

• US Dollar (USD): Asset managers remained near a record level of net-short exposure to the USD index (-8.2k contracts)

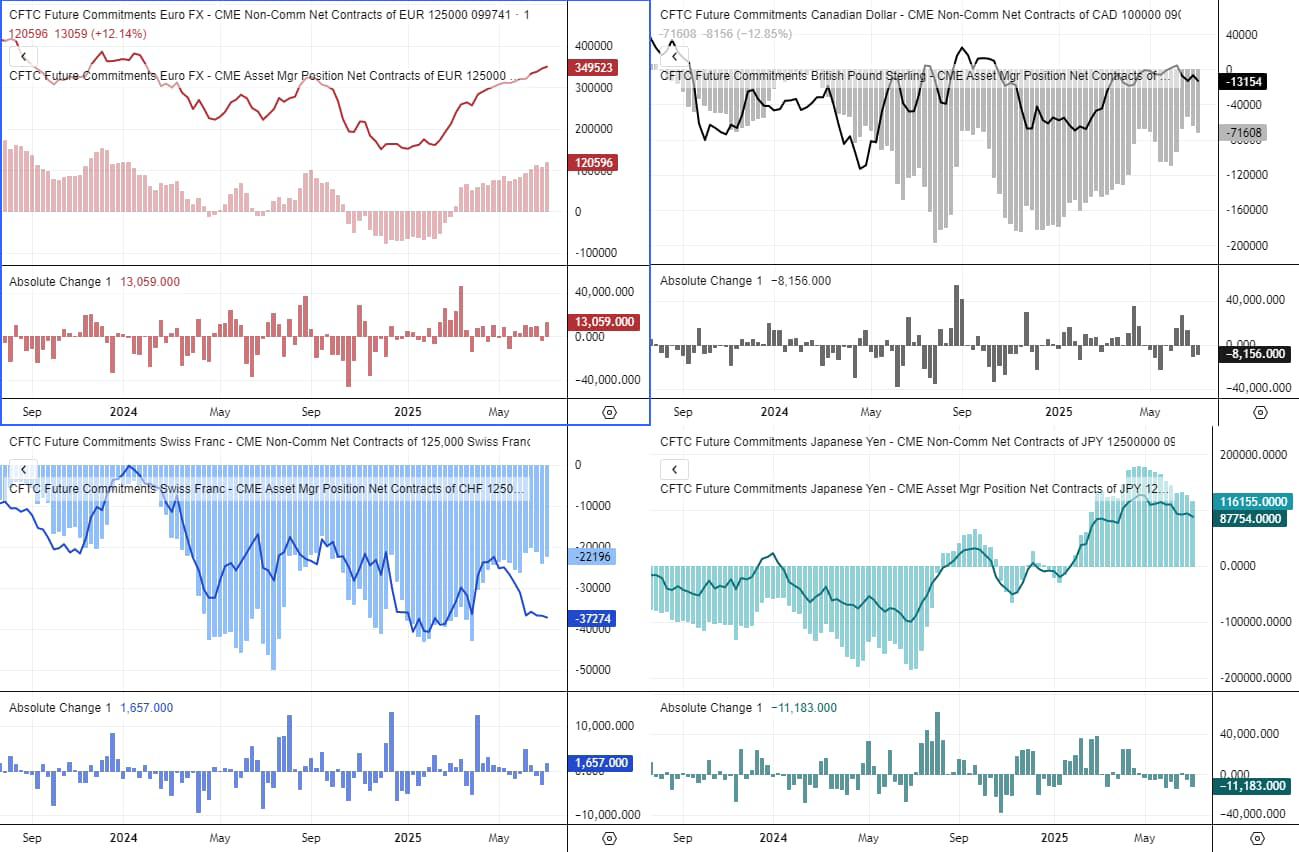

• European dollar (EUR): Large speculators increased their net-long exposure by 13.1k contracts to a 18-month high

• British pound (GBP): Large specs remained net-long around 33k contracts, yet asset managers remain net-short around -13k contracts

• Japanese yen (JPY): Net-long exposure fell to a 19-week low among large speculators

• Australian dollar (AUD): Large specs and asset managers increased net-short exposure to a 15-week high

• Canadian dollar (CAD): Traders increased net-short exposure higher for a second week (+8.2k contracts week over week)

• New Zealand dollar (NZD): Asset managers and large speculators remained marginally net long by 9.2k and 4.9k contracts respectively

• Wall Street Indices: Asset managers increased their net-long exposure to E-mini S&P 500 futures by 23.4k contracts, Nasdaq 100 E-minis by 6.3k contracts and VIC futures by 8.6k contracts

• Gold (GC):

• Silver (SI):

• Crude Oil (WTI): Net-long exposure fell by -25.3k contracts among large speculators

• Volatility Index (VIX): Asset managers pushed net-long exposure to an 8-month high

View related analysis:

- AUD/USD weekly outlook: US CPI and Aussie Jobs in Focus

- US Dollar and Canadian Dollar Under Pressure as Japanese Yen Attracts Flows

- Japanese Yen, Wall Street Bulls Remain Hesitant to Commit: COT Report

- US Dollar Rallies as Tariff Tensions Rattle Markets and Risk Appetite

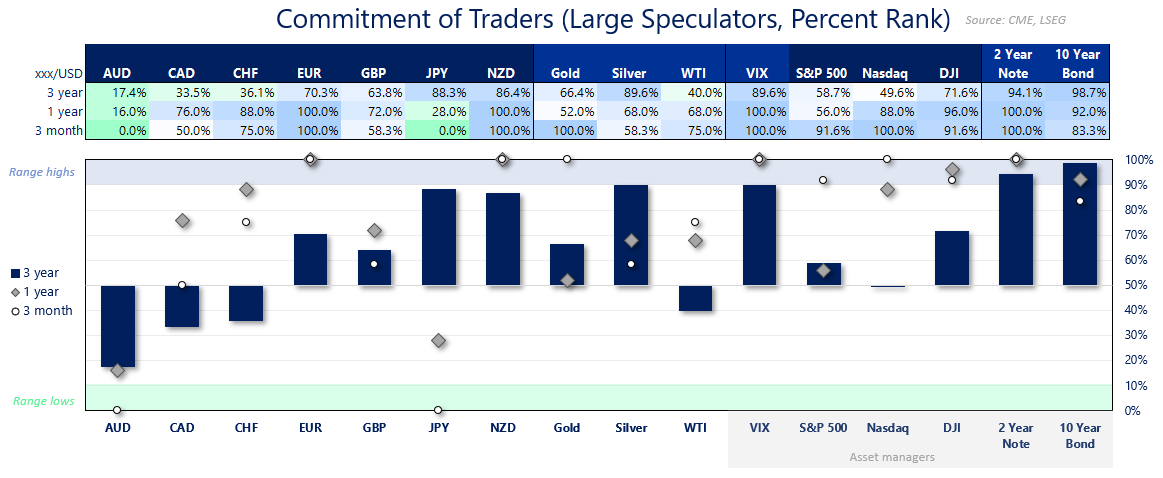

Commitment of Traders dashboard showing large speculator positioning percent rank over 3-month, 1-year, and 3-year periods across forex pairs like AUD/USD, CAD/USD, and NZD/USD, plus commodities (gold, silver, WTI), and indices (S&P 500, Nasdaq, Dow Jones). AUD and NZD are at multi-month positioning lows, while US bonds are near range highs. Useful for gauging market sentiment shifts and USD correlation trends.

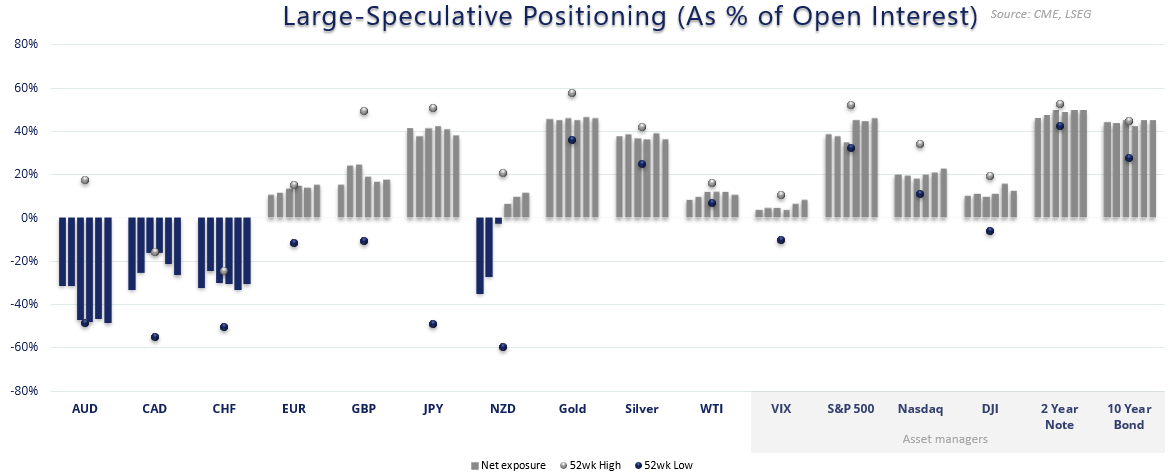

Bar chart showing large-speculative positioning as a percentage of open interest for forex, commodities, and indices. AUD, CAD, CHF, and NZD show deep net-short positions, while JPY, gold, and silver hold strong net-longs. Markers indicate 52-week highs and lows in net exposure. A tool for assessing market positioning extremes and potential reversal risks.

USD Rallies for 7 Days as Asset Managers Hold Near Record Net-Shorts

The US dollar index rose for a seventh consecutive session on Friday — its strongest winning streak since October. On the weekly chart, a pattern resembling a morning star reversal has emerged, following a false break beneath the 2023 low. This coincided with a bearish engulfing candle on EUR/USD and the euro’s failure to hold above the 1.08 handle.

Interestingly, despite the index grinding higher, asset managers remained near record net-short exposure to USD futures as of last Tuesday — though their overall position was flat on the week. Large speculators, meanwhile, reduced their net-short USD exposure for a second week. While their net-short exposure isn’t necessarily extreme on an absolute scale, it is on a relative basis. Gross-shorts are also near a 4-year high, so perhaps USD shots should tread with caution.

Euro & Pound Futures: Bullish EUR Positioning vs Cautious GBP

Notably, both asset managers and large speculators increased their net-long exposure to EUR/USD futures, reaching their most bullish stance in around 18 months. While this may suggest a potential sentiment extreme against the US dollar, it is less clear whether positioning in EUR/USD futures alone has reached such an extreme.

Meanwhile, asset managers remained net-short GBP/USD futures, and it appears a cycle high for the British pound may have formed in early June. However, stronger confirmation is needed—specifically, a reduction in large speculators' net-long exposure, followed by a potential switch to net-short positioning. Until then, any downside potential for GBP/USD may remain limited or tentative.

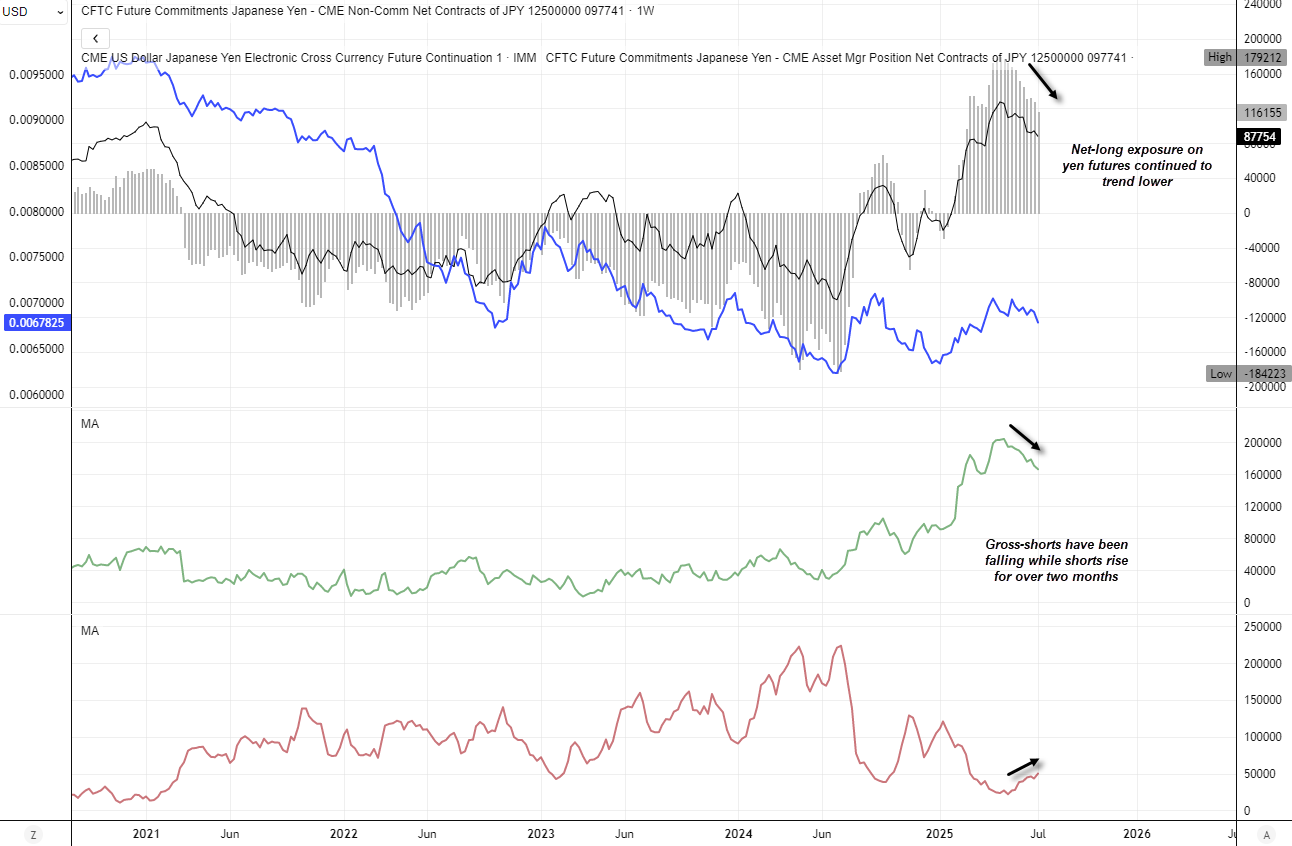

Japanese Yen Positioning: Weekly COT Report Signals Weaker JPY vs US Dollar

Net-long exposure to Japanese yen (JPY) futures continued to decline last week as Bank of Japan (BOJ) rate hike expectations fade. While traders remain predominantly net-long JPY, both asset managers and large speculators have trimmed their bullish bets by roughly one-third from the recent peak.

The decline in net-long positioning has been driven by a consistent rise in short positions and a steady reduction in longs over the past two months. If this trend persists, it suggests further downside risk for the Japanese yen and could support continued upside in USD/JPY.

Commodity FX Positioning (AUD, CAD, NZD, MXN): Weekly COT Report Overview

The divergence in speculative positioning between the antipodean currencies widened last week, as traders increased net-long exposure to Australian dollar (AUD) futures to a 15-week high, while maintaining net-long positions on New Zealand dollar (NZD) futures.

This shift is particularly notable given the Reserve Bank of Australia’s (RBA) surprise decision to hold its cash rate at 3.85% — a move contrary to market expectations. Despite the hawkish disappointment, AUD/USD went on to rally through to Friday’s close, suggesting some bearish traders may have been squeezed out of their short positions. Unless Australia posts soft employment data this week or a weak Q2 CPI print on 30 July, traders may continue to favour dip-buying above the 65c handle.

![]()

CAD/USD Positioning: Canadian Dollar Futures – Weekly COT Report

Meanwhile, large speculators and asset managers increased net-short exposure to Canadian dollar (CAD) futures for a second consecutive week, although positioning remains far from extreme. In contrast, net-longs in Mexican peso (MXN) futures edged higher, which may reflect a view that the worst of Trump’s tariff risks have passed.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade