- Strong US data and risk appetite continue to support USD/JPY upside

- BOJ intervention threats and Hormuz hopes deliver offsetting forces

- Economic data playing increasingly unfamiliar secondary role

- JGB auctions may test Japan’s intervention resolve

- USD/JPY remains trapped beneath 158 in narrow range

Bullish Fundamentals Meet Intervention Threat

USD/JPY begins the new week in what feels like perpetual gridlock, with buoyant risk appetite, solid US economic data and an improving backdrop for global economic growth continuing to exert upside pressure on the pair. At the same time, the ongoing threat of BOJ intervention and relentless hopes for an eventual peace agreement between the US and Iran to reopen the Strait of Hormuz have delivered a near-perfect offset, keeping USD/JPY contained to a narrow sideways range just beneath multi-decade highs.

That looks unlikely to change in the near term unless we see a regime shift beyond that which has dominated since the early parts of March. Right now, economic data matters little compared to headlines relating to the Iran war, subsequent impacts on crude oil prices and whether Japanese authorities continue attempting to stall yen weakness.

While US Treasury Secretary Scott Bessent’s visit to Japan on the way to talks in China later in the week creates obvious headline risk, he’s highly unlikely to explicitly disendorse recent intervention measures, making it difficult to see the trip leaving a lasting imprint on the pair unless his rhetoric shifts materially from what markets have become accustomed to hearing in recent months.

Markets will be paying close attention to whether Bessent, who is also scheduled to meet BOJ Governor Ueda alongside Finance Minister Katayama and Prime Minister Takaichi, repeats previous remarks that higher Japanese interest rates may prove a more effective response to yen weakness than intervention alone.

Traditional Market Relationships Breaking Down

The extent to which traditional relationships have broken down was perfectly illustrated following last Friday’s April non-farm payrolls report. Looking across markets, you would barely have known payrolls growth came in close to double expectations, normally the type of upside surprise that would spark a sharp repricing in Fed expectations, Treasury yields and the US dollar.

While the underlying detail was softer than the headline suggested, with unemployment edging higher on an unrounded basis, participation falling to multi-year lows and household employment declining for a fourth consecutive month, it remains telling that markets barely batted an eyelid. Fed pricing moved little, Treasury yields struggled to gain traction and USD/JPY remained trapped within the same range that has dominated for weeks. If a blowout payrolls report cannot sustainably shift markets, what hope do lower-tier releases have?

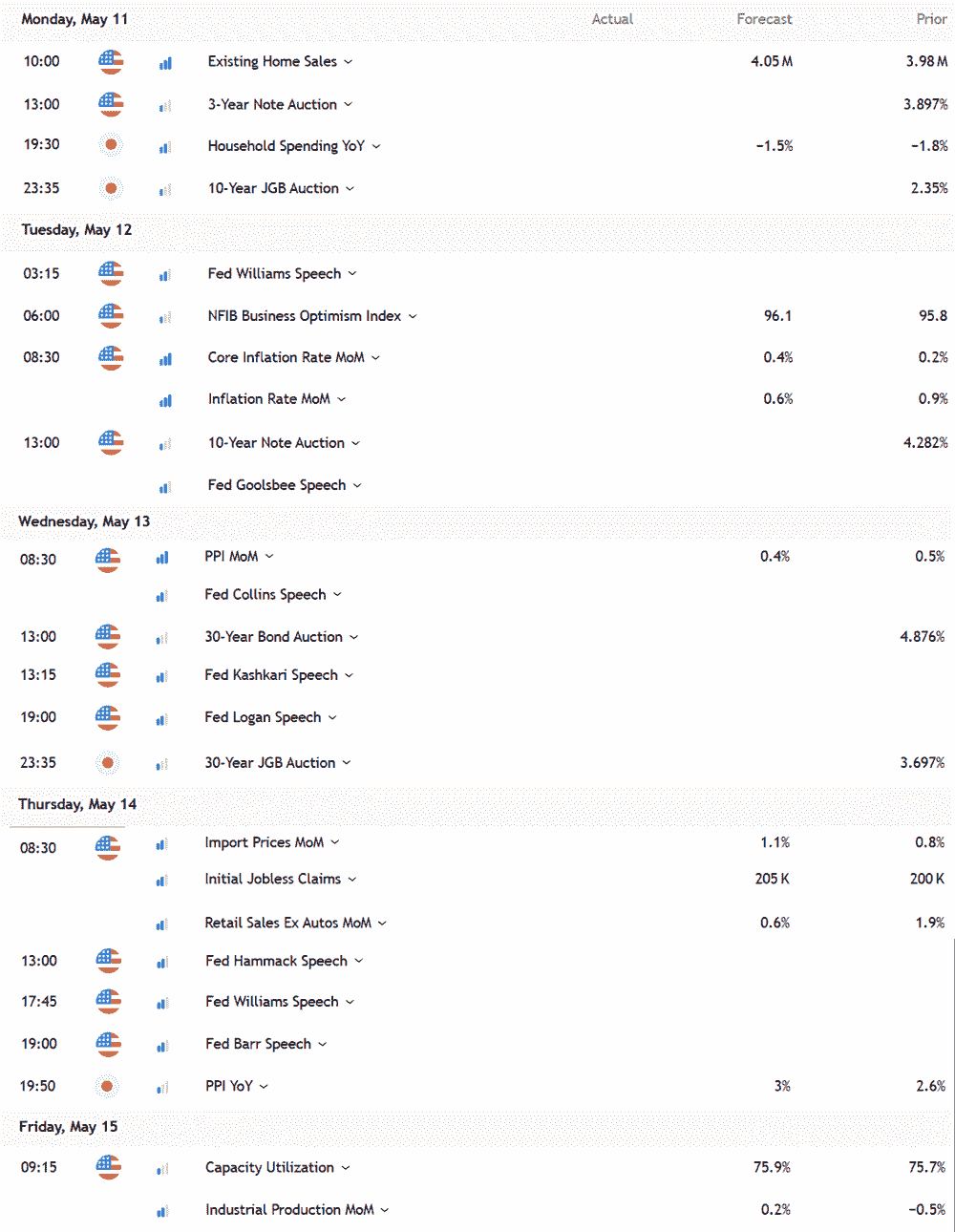

Japan’s Bond Market Back in Focus

Source: TradingView

That may help explain why this week’s Japanese government bond auctions could prove more influential for USD/JPY than the US economic calendar, especially in the ultra-long end of the curve. Well before the Iran war and recent intervention measures, markets were telling Japanese policymakers in no uncertain terms that interest rates needed to move higher to compensate for the nominal growth outlook along with economic and fiscal uncertainties tied to Japan’s enormous public debt burden. Otherwise, the yen needed to weaken to compensate.

By intervening in the currency, authorities have effectively redirected that pressure back onto the JGB market. It’s telling yields have barely retraced from recent highs, raising questions as to whether sustained efforts to suppress yen weakness may begin to hinder buyer appetite, especially for longer-dated debt. That leaves this week’s 10 and 30-year JGB auctions as potentially important events, with weak demand likely to heap additional pressure on long-dated yields and test the resolve of the Ministry of Finance to continue counteracting market forces via intervening in the yen.

Source: TradingView (US Eastern Daylight Time)

US Inflation Data Still Matters at the Margin

As for the US calendar, headline and core CPI are expected to lift 0.6% and 0.3% respectively in April, both monthly increases that annualise well above anything remotely consistent with the Fed’s supposed 2% inflation target. But the energy price spike may prove temporary, and with labour market conditions stable rather than running hot, it will allow the Fed, collectively, to look through the inflationary impulse for now.

Instead, concern is more likely to emerge if inflation pressures begin feeding through more aggressively into core services prices ex-housing given the stronger relationship with wage pressures. Regarding PPI, attention will likely focus on those components that feed directly into the Fed’s preferred underlying inflation measure, the core PCE deflator released later in the month.

Turning to retail sales, after impressive numbers in March, the key question is whether spending strength extended into April, especially outside of auto categories. In the current environment, if there is one component likely to carry greater market influence than the rest, it may prove to be the control group sales figure that feeds directly into GDP calculations.

Source: TradingView

The Fed speaker calendar will also add colour, but with markets pricing no movement in the funds rate this year, it’s hard to see any official making a convincing case as to why rates need to be cut or lifted right now. There literally is none.

Intervention Distorting Technical Signals

From a technical perspective, I’m not even bothering to evaluate the message from oscillators right now as suspected intervention has completely morphed the signalling. While intervention ensured USD/JPY did not venture back into the narrow trading range it occupied over the prior two months last week, it also failed to meaningfully alter the broader technical picture, merely shunting the pair into a new sideways range immediately beneath.

Source: TradingView

Strong offers emerging on pushes towards the bottom of the former range around 158 have capped upside attempts, while a wall of bids beneath 155.65 has repeatedly soaked up supply whenever abrupt downside moves have taken place. They remain the two immediate levels traders should focus on this week, alongside the 100-day moving average located in the upper half of the range.

Either side, a sustained break back above 158 would place the 50-day moving average and 159.00 into focus before the far more important 160 level comes into view. On the downside, it’s notable the last suspected intervention episode on Wednesday during the final day of Japan’s extended holiday period stalled just ahead of the uptrend running from the Liberation Day low established in April last year.

While it has not been tested for some time, the trendline did attract several touches soon after being established, making it, 154.45 support and the 200-day moving average the key downside levels to watch should the prevailing sideways range eventually break lower.

My suspicion is the range may continue to hold this week, but if there is a directional risk I cling to right now, it’s probably still skewed modestly higher rather than lower.