- Front-end US yields retake control of USD/JPY

- Fed pricing flips from cuts to tightening

- Markets price 80% chance of June BOJ hike

- JGB bear steepening signals BOJ credibility fears

- USD/JPY closes back in on 160

BOJ intervention noise fades

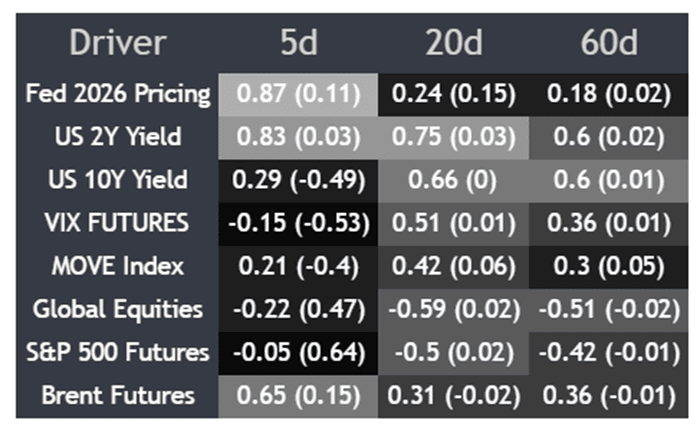

After suspected intervention activity from Japanese authorities created havoc with traditional market relationships the prior week, USD/JPY reverted to trading primarily off moves in the front-end of the US Treasury curve over the past five trading days. As shown in the rolling correlation matrix below, short-dated US yields once again emerged as the standout driver of the pair, providing a far better read on what matters and what does not heading into the new week.

Source: TradingView

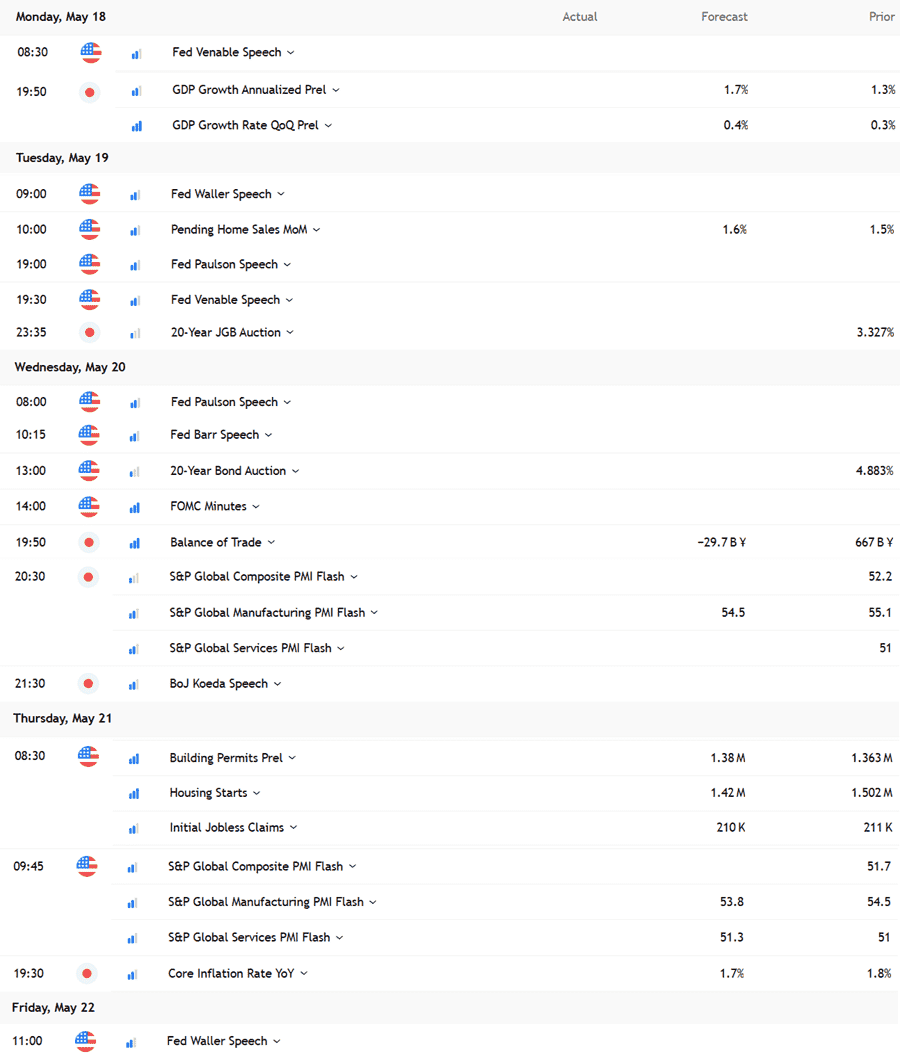

Fed speakers back in focus

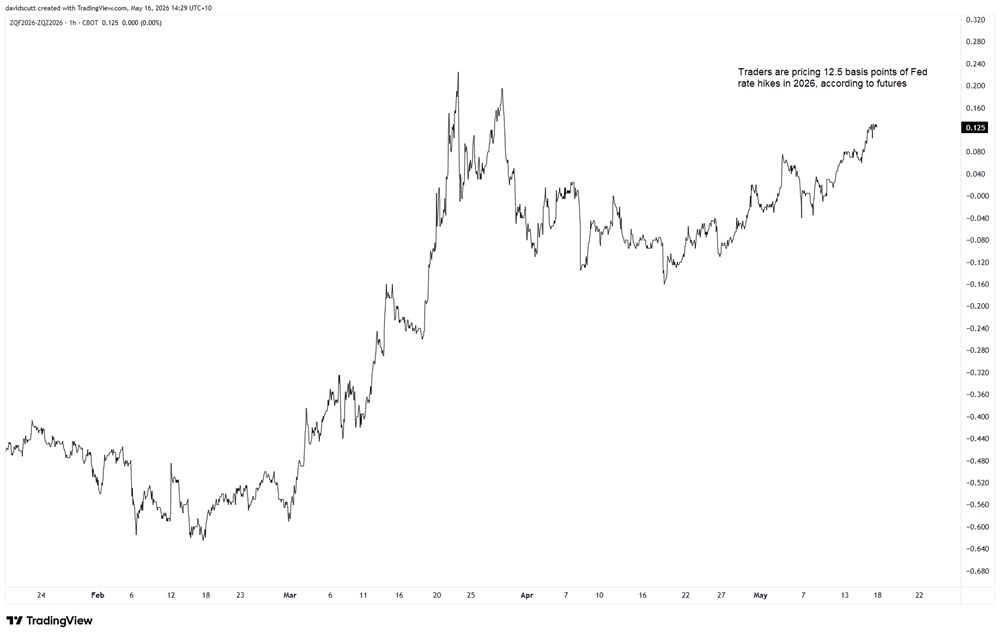

With no top-tier US economic data scheduled, attention is likely to fall heavily on speeches from Fed policymakers as markets reassess how officials may respond now there's clear evidence the inflationary pulse from the Iran war has spread beyond energy into both goods and services inflation.

Source: TradingView

Given his track record for moving markets, remarks from Fed Governor Christopher Waller loom large, especially with traders increasingly questioning whether the Fed can continue entertaining rate cuts in the current environment. Traders now have around 12.5 basis points of tightening priced by year-end, marking a massive hawkish recalibration from immediately before the Iran war began when futures markets were pricing more than two rate cuts this year.

Aside from Waller, remarks from Anna Paulson may also be of interest given she's a voting member on this year's FOMC. Venable may not be a voter this year, but having only recently started as Atlanta Fed president, her views may also be noteworthy when it comes to assessing the direction for policy next year.

Source: TradingView

Koeda takes centre stage

In Japan, there's a more spice to the calendar with Q1 GDP and nationwide CPI data for April, along with a speech from BOJ board member Koeda.

While GDP can sometimes move the yen, the report risks coming across as ancient history given how rapidly the macro environment has shifted in recent weeks. The domestic demand components may be more interesting than the headline figures themselves, particularly household spending and private investment. The GDP deflator will also provide useful insights into economy-wide inflationary pressures before the impact from higher energy prices really began to bite.

As for the nationwide CPI report, it's now been well and truly superseded by the Tokyo version that arrives three weeks earlier, meaning it rarely surprises markets nowadays, let alone moves them.

That leaves Koeda as the potentially more interesting event risk given pressure that's emerged on both the yen and JGBs since the BOJ last met in late April. While she voted to keep policy settings unchanged at that meeting, Koeda has previously been viewed as leaning towards the more hawkish side of the spectrum when it comes to policy settings.

With markets pricing around 20 basis points of tightening in June, implying roughly an 80% probability of a hike, any signs of reluctance to resume policy normalisation in what is clearly an inflationary environment will only amplify concerns about whether the BOJ is taking its job seriously when it comes to taming inflation, as demonstrated by the backing up of JGB yields last week.

Japan's policy dilemma deepens

The yield curve comparison graphic below is important when it comes to understanding what's driving Japanese yields higher. Since the Iran war began, there's been a huge bear steepening in the JGB curve, most of which has occurred since the BOJ last met on April 28. Since then, 10-year yields have risen 25 basis points, 20-year yields 38 basis points and 30-year yields 44 basis points. Pretending there's no inflation has consequences.

Source: TradingView

If the move was genuinely being driven by rising expectations for BOJ rate hikes as some media reports were suggesting late last week, the curve would likely be bear flattening or twist flattening where short-end yields rise while longer-dated yields move lower. Instead, the opposite has occurred.

The aggressive bear steepening suggests the BOJ is viewed as being well behind the curve in bond traders' minds, with investors increasingly demanding additional compensation to hold longer-dated Japanese debt as inflation pressures build and fiscal risks grow.

The longer the disruption to energy markets persists, the uglier the backdrop risks becoming for Japanese policymakers. Japan remains particularly vulnerable given its enormous public debt loading, rapidly ageing demographics and near-total reliance on imported energy to power the economy.

With markets rapidly scaling back Fed easing expectations while the USD surges higher, it's becoming an increasingly difficult combination for Japanese authorities to digest. It therefore comes as little surprise that we've seen no meaningful evidence of follow-up intervention from Japanese authorities after the suspected activity earlier this month.

Leaning against USD/JPY strength while macro forces simultaneously demand either a weaker yen and/or higher JGB yields to compensate for rising inflation and fiscal risks is totally counterproductive.

USD/JPY eyes 160 again

Source: TradingView

With no intervention to slow its ascent and front-end US rates shifting hawkish, USD/JPY resumed its ascent last week, making short work of the 100-day moving average and 157.92, two levels that had capped the pair during periods of suspected BOJ intervention activity earlier this month.

Sitting in an established uptrend, it feels almost inevitable under this rates-driven regime that the pair may soon retest the key 160 level, with only the 50-day moving average and minor resistance at 159.00 located in between. As seen in the insert on the left-hand side showing the weekly candles, last week also saw the completion of a morning star bullish reversal pattern, only reinforcing the view that the path of least resistance remains higher.

The spurious messaging from the oscillators due to intervention activity has also quickly passed, with RSI (14) trending higher above 50 while MACD has crossed the signal line and looks set to flip positive imminently. Be it the price action, shifting momentum or reversal pattern on the weeklies, without the threat of intervention one wonders just how much higher the pair would now be trading given prevailing macro conditions.

If, for whatever reason, downside does emerge, be it from renewed intervention threats, actual intervention activity or concrete positive news on the outlook for Middle East energy flows, the levels to watch include the May uptrend and 157.92 which may now flip to providing support, along with 157 and 155.65 where buyers fell over one another to absorb offers earlier this month.