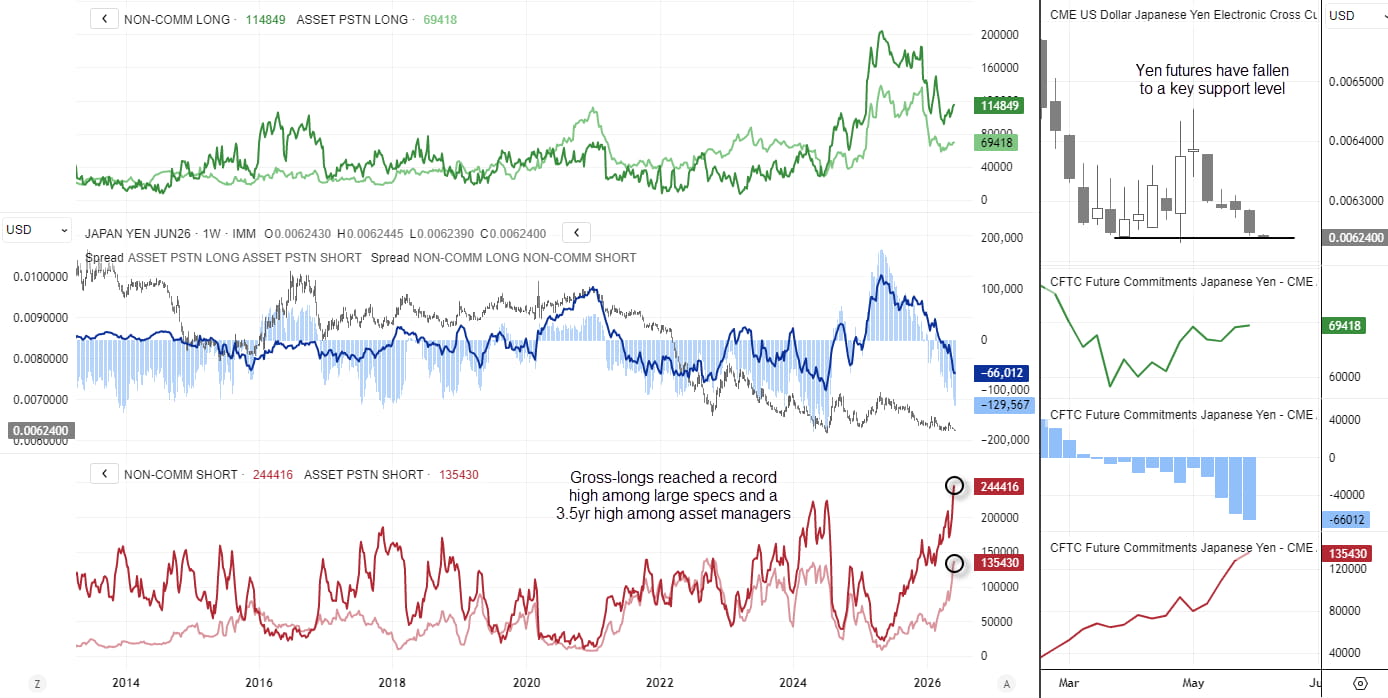

Speculative traders ramped up bearish bets against the Japanese yen to record highs as USD/JPY pushed above 160, increasing the risk of intervention from Japan's Ministry of Finance. Meanwhile, net-long exposure to the US dollar climbed to an eight-week high, reinforcing the bullish outlook for the greenback.

Elsewhere, the Australian dollar is on the verge of flipping to net-short exposure as traders unwind long positions, while bearish bets against the Canadian dollar continue to build. This week's Commitment of Traders (COT) report reveals a growing divergence in sentiment across major FX markets.

View related analysis:

- Australian Dollar Outlook: AUD/USD Bears Tighten Grip with 60s in Sight

- Japanese Yen Outlook: Volatility Perks Up Ahead of NFP for USD/JPY and AUD/JPY

- FX Futures Positioning: US Dollar Bulls Return, Yen Bears Tease MOF

- How to Read the COT Report to Track Forex Market Sentiment

- Japanese Yen Outlook: Volatility Perks Up Ahead of NFP for USD/JPY and AUD/JPY

Record Yen Shorts and Rising USD Longs Highlight Shifting FX Sentiment

Large Speculator Positioning from the COT report

Source: CFTC (COT), CME, ICE, LSEG

For traders wanting a deeper understanding of futures positioning, I’ve also published a guide on how to read and interpret weekly COT data in forex markets.

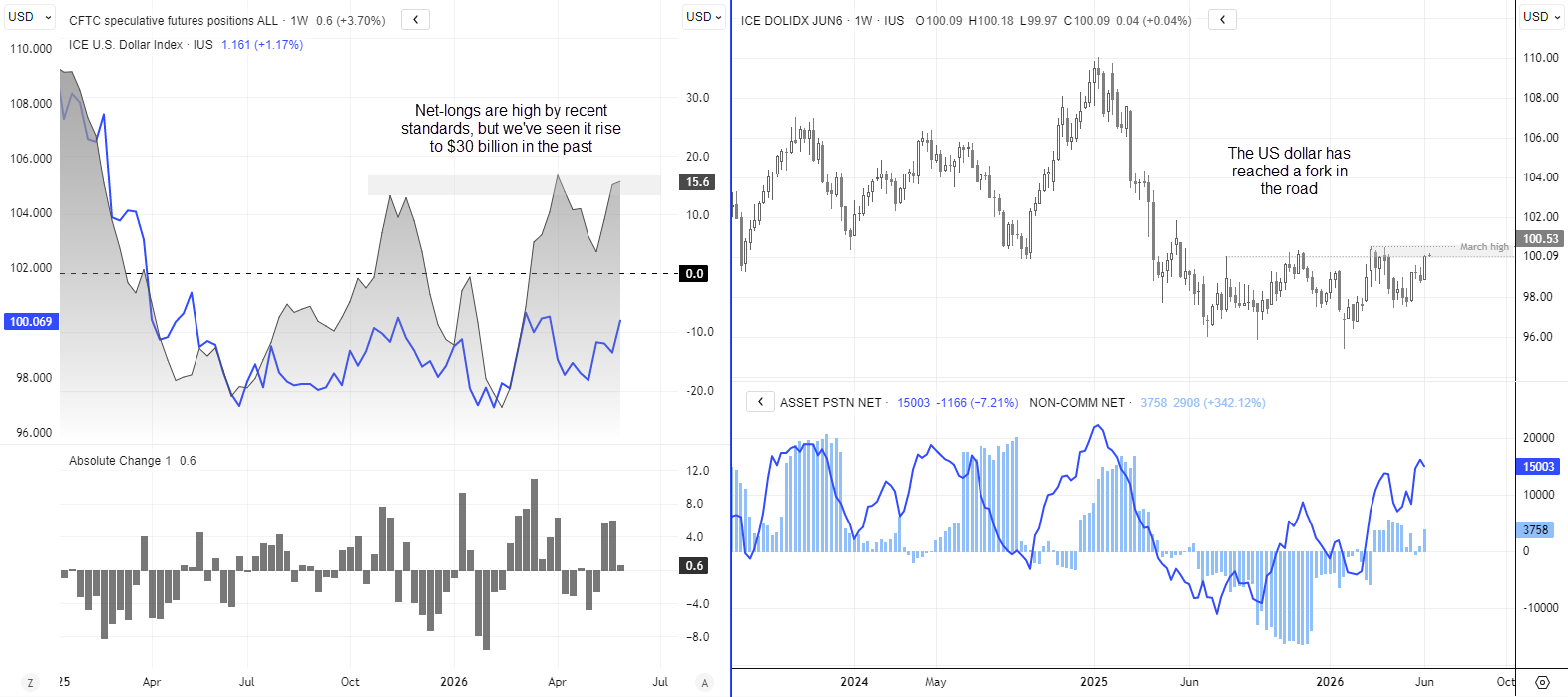

- US Dollar: Net-long exposure to the US dollar via CME futures reached an 8-week high of $15.6 billion

- EUR/USD: Large specs and asset managed increased net-long exposure by a combined 35.4k contracts

- GBP/USD: Traders remained net-short by a combined -153k contracts, with only minor adjustments from the prior week

- USD/JPY: Short bets against the Japanese yen hit a record high among large speculators and a 3.5-year high among asset managers

- USD/CHF: Asset managers reduced their net-short exposure to Swiss franc futures to a 1-year low

- USD/CAD: Net-short exposure to Canadian dollar futures rose to a 25-week high among large specs and asset managers

- AUD/USD: Large specs were on the cusp of flipping to net-short exposure, with gross longs falling -24k from the prior week

- NZD/USD: Bears were derisking with both sets of traders reducing gross-longs by a combined -17.4k contracts

Asset Manager Positioning | COT Report

Source: CFTC (COT), CME, ICE, LSEG

FX Futures Positioning | COT Report (IMM Data)

US Dollar Index (DXY) Futures Positioning | COT Report

The rush into USD longs had slowed by the time the latest COT data were collected at Tuesday's close. Yet while net-long exposure rose by just $0.6 billion, the bullish case has strengthened since the latest NFP and ISM reports. The dollar's net-long exposure of $15.6 billion may be high by recent standards, but we've seen bulls push above $30 billion if we look further back.

My assumption that the ABC correction ended in early March at 100.50 is now in doubt, which means we need to keep a close eye on how the dollar behaves around current levels. Ultimately, I am now on standby for a potential bullish breakout unless expectations for a Fed rate hike are somehow reversed, which seems unlikely for now.

Source: ICE, CFTC (COT), LSEG

USD/JPY Futures Positioning | COT Report

There is now a compelling case for Japan's Ministry of Finance (MOF) to intervene in the currency market again, given USD/JPY has broken above 160 on rising expectations of a Fed rate hike. It is therefore interesting to note that large speculators increased their net-short exposure to a record high last week, while asset managers lifted theirs to a 3.5-year high.

Note that yen futures are within a whisker of their previous intervention level. This is not to say the MOF will intervene again the moment that level is breached—assuming it is allowed to. However, with USD/JPY standing a decent chance of breaking to fresh highs, the higher it rises and the faster it moves, the greater the odds of intervention.

Source: CME, CFTC (COT), LSEG

Commodity FX Positioning (AUD, CAD, NZD) | Weekly COT Report Overview

AUD/USD: I have been calling for a deeper pullback in the Australian dollar for several weeks, and clues to its recent decline were also visible in stretched market positioning. Large speculators were on the cusp of flipping to net-short exposure last week, while asset managers' net-long exposure has more than halved from the record high reached just two weeks ago.

However, short bets remain relatively low, so I suspect this is a long liquidation event rather than a true trend reversal. Even so, the pullback could still allow for a dip into the upper 60s.

NZD/USD: A reduction in short bets against the New Zealand dollar has seen net-short exposure fall to a nine-week low on NZD/USD futures. Yet this is somewhat undermined by the bearish engulfing candle and sharp reversal lower from 60 cents last week. A rise in short bets seems likely in the next COT report.

USD/CAD: Weak GDP and employment figures have triggered another increase in short bets against the Canadian dollar. Net-short exposure rose to a 25-week high among large speculators, with an apparent reduction in gross longs also contributing to the increase in net-short CAD exposure. Note that net exposure is not at a sentiment extreme for either group of traders, and that could bode well for USD/CAD longs.

Source: CME, CFTC (COT), LSEG

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade