- USD/JPY once again tracking front-end US-Japan rate spreads

- Hot US inflation sees markets abandon Fed cut expectations

- Suspected intervention slowing yen weakness, not reversing it

- Traders eye Hormuz headlines for inflation and yield implications

Summary

USD/JPY is once again trading like a rates differential story, particularly at the front-end of the curve. The relationship reasserted itself aggressively following the latest hot US inflation data, helping to explain why the pair is once again pressing up against levels where suspected intervention from Japan’s Ministry of Finance took place in recent weeks.

But with markets starting to price the risk of Fed rate hikes as US inflation pressures reaccelerate and broaden, the bigger question now is whether Japanese authorities are willing to continue pushing back against fundamental forces that are arguing for a weaker yen.

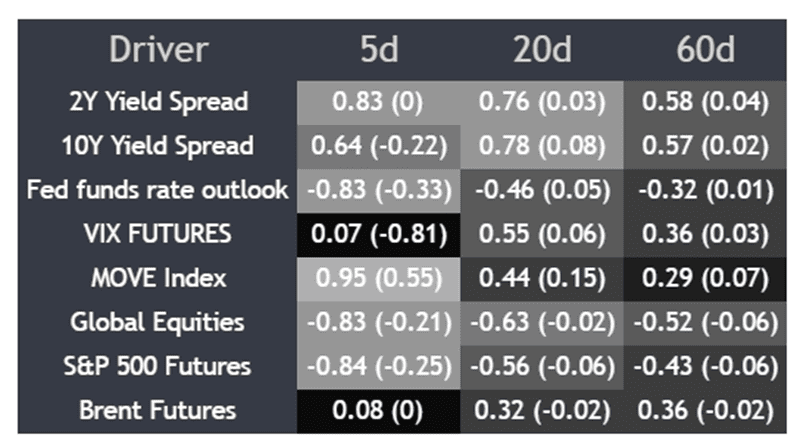

Rates Regain Control

The shift back towards rate differentials as the dominant driver of USD/JPY is visible in the correlation matrix below. Relationships between the pair and US-Japan front-end yield spreads have strengthened notably across short and medium-term rolling windows, with the relationship against two-year spreads especially firm over the past month.

Source: TradingView

At the same time, the relationship between USD/JPY and broader risk sentiment gauges such as the VIX has weakened sharply, reinforcing the view that rates, rather than haven demand, energy prices, or broader market volatility, are once again driving directional price action.

Importantly, correlations over shorter rolling windows may actually understate the strength of the relationship given suspected intervention episodes from Japan’s Ministry of Finance in recent weeks likely interrupted what otherwise may have been an even tighter alignment between widening US-Japan spreads and USD/JPY upside.

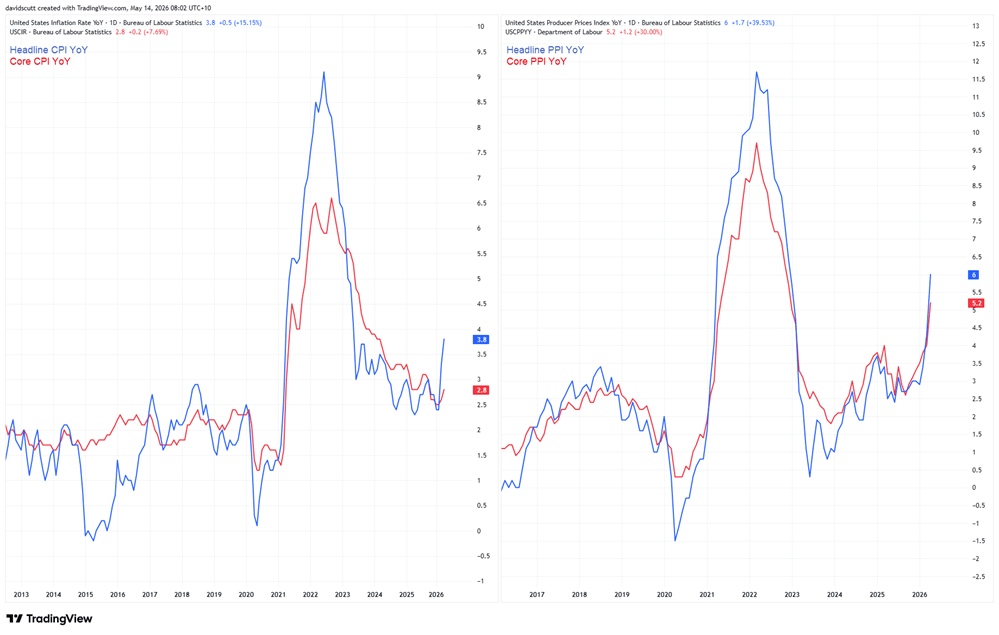

US Inflation Pulse Broadens

That shift in correlations comes as markets rapidly reassess the US rates outlook following another hot round of inflation data. Producer prices surged 1.4% in April, the largest monthly increase since March 2022, pushing the annual rate to 6.0%, the highest since December 2022.

Source: TradingView

Importantly, the inflation pulse was not confined to energy. Services prices jumped 1.2%, the biggest increase in four years, while core goods prices excluding food and energy rose 0.7% on the month and 4.6% from a year earlier, pointing to broadening upstream price pressures across the economy.

Fed Hike Risks Grow

With US consumers continuing to spend aggressively and businesses increasingly passing through higher input costs, markets are beginning to price the risk that the next move from the Fed may eventually need to be a rate hike rather than a cut.

Source: TradingView

Markets have responded by abandoning expectations for Fed rate cuts altogether, with futures now pricing around 8 basis points of tightening by year-end. More notably, the implied Fed funds rate by the end of 2027 now sits above the current effective funds rate, signaling no move in rates this year or next.

While trading volumes that far out the curve remain relatively thin, it suggests incoming Fed chair Kevin Warsh may have his work cut out convincing fellow FOMC members that easier policy is warranted, especially with inflation pressures broadening and economic growth continuing to hum along thanks in part to enormous AI-related capital expenditure.

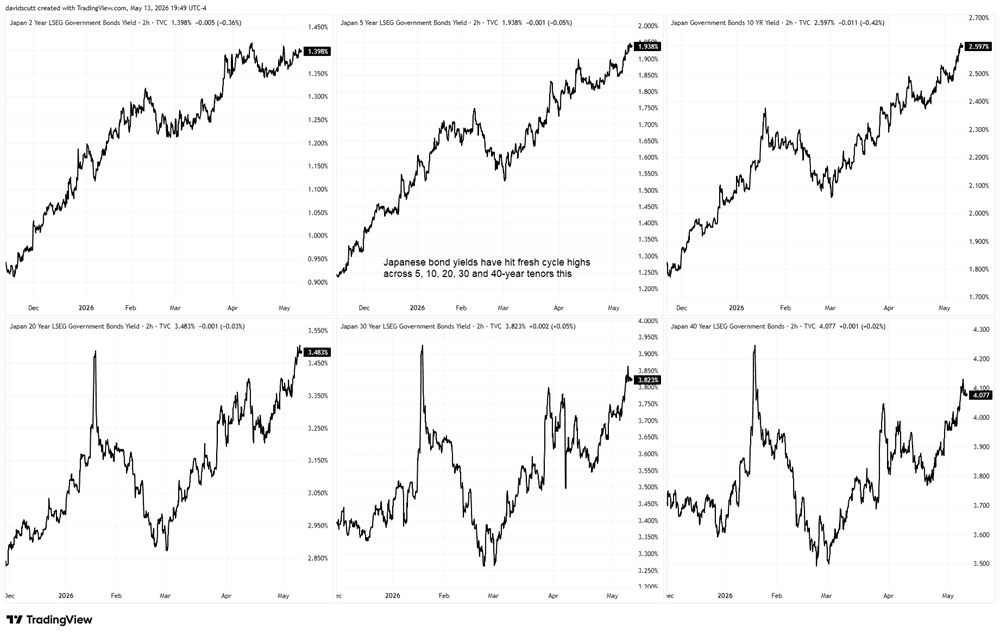

Intervention Meets Macro Reality

The repricing in Fed expectations, alongside ongoing disruption through the Strait of Hormuz and heavy corporate debt issuance, has continued to place upward pressure on Treasury yields across the curve, helping to fuel renewed dollar strength against the yen.

Source: TradingView

At the same time, as discussed previously, markets continue to demand higher yields in Japan to compensate for perceived fiscal and economic risks. Without that adjustment, the alternative mechanism remains further yen weakness.

That leaves Japanese authorities in an increasingly uncomfortable position. While suspected intervention episodes may have temporarily slowed the pace of yen depreciation, continuing to lean against widening rate differentials risks becoming increasingly difficult and costly if US inflation pressures continue to broaden and Treasury yields keep heading higher.

Traders Eye Beijing Headlines

Attention will now turn to the meeting between Donald Trump and Xi Jinping in Beijing later on Thursday. While markets clearly anticipate optimistic headlines surrounding technology and investment, for USD/JPY traders it may be any developments tied to the war with Iran and the potential reopening of the Strait of Hormuz that matter most.

With the energy shock continuing to feed directly into US inflation pressures and Treasury yields, any attempts towards de-escalation that ease supply disruptions could temper the widening divergence between the energy haves and have nots that is underpinning dollar strength against the yen.

Intervention Zone Back Under Pressure

Source: TradingView

From a technical perspective, USD/JPY finds itself wedged beneath 157.92 resistance ahead of this key event, a level where the BoJ was likely instructed to intervene earlier this month.

A break above may signal a reluctance from Japan’s Ministry of Finance to continue pushing back against fundamentals for now, potentially allowing for a run higher towards the 50-day moving average or 159 resistance. Anyone contemplating longs on a break should ensure risk management is in place to limit capital risk should the BoJ go bang again.

If USD/JPY remains capped beneath 157.92, the option exists to initiate shorts with a tight stop above for protection, targeting 156.00 where the pair found plenty of willing buyers during other suspected intervention episodes. The 157 figure also remains notable given the price spent considerable time trading either side of the level in recent weeks.

But if considering shorts, traders are effectively relying upon the BoJ to wade back in with the bazooka because fundamentals continue to argue for further upside in USD/JPY. Potentially a lot more.

While I'm placing far less weight on indicators than usual given the current backdrop, downside momentum that had been building following prior intervention episodes is already petering out, with RSI (14) and MACD now generating increasingly neutral signals on directional risks.