- Markets have all but priced a BOJ hike to 1% next week

- Nikkei reports officials may slow or pause QT

- Investors demand greater yield compensation for Japan's risks

- A cheaper yen may be filling the compensation gap

- US CPI, PPI key for USD/JPY ahead of Fed, BoJ

The Real Decision Facing the BOJ

Markets have all but settled on the Bank of Japan raising rates by 25 basis points to 1% next week, with overnight index swaps pricing around 50 basis points of tightening in total this year. But the real question is what the BOJ decides to do with the pace of quantitative tightening after Nikkei reported policymakers are considering slowing or even pausing the runoff of their bond holdings.

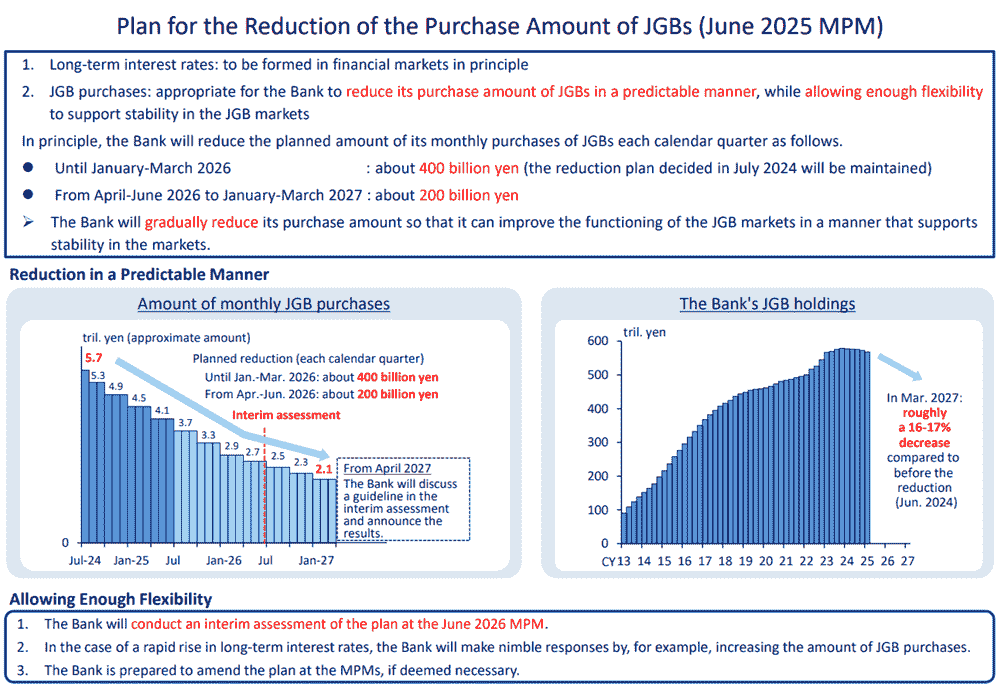

Under the plan unveiled last June, the BOJ reduced monthly JGB purchases from around ¥5.7 trillion to ¥2.9 trillion by early 2026 through quarterly reductions of ¥400 billion. The expectation had been that purchases would continue to decline towards roughly ¥2.1 trillion a month. The latest speculation suggests that path may no longer be set in stone.

Source: BoJ

That's what makes next week's decision so important. By buying fewer government bonds than are maturing in recent years, the BOJ has gradually withdrawn one of the largest sources of demand from the JGB market just as borrowing costs have risen around the world. Private investors have been forced to absorb more public debt supply, helping explain why long-dated JGB yields have climbed so aggressively.

I've long argued that, when forced to choose between saving the yen or JGB market, the BOJ will eventually be pressured into choosing the bond market. If it decides to slow the pace of runoff next week, it may reinforce that view, leaving the yen exposed to renewed weakness even as policymakers continue to raise interest rates.

Despite fluctuations in energy markets and wobbles in risk assets, the consistent trend has been yen and JGB weakness. This is a structural story. As long as US yields remain elevated and US economic exceptionalism persists, Japanese policymakers may have to accept they cannot have both stable, low yields and stability in the yen. They either need to let yields rise to compensate investors for fiscal, inflation and geopolitical risks, or let the currency weaken further as a pressure relief valve.

Trying to simultaneously cap yields and yen weakness is a bit like having one's cake and eating it too. It may work for a while, but it cannot be done forever, especially in a world where higher borrowing costs have created a more competitive marketplace for capital.

If that's right, next week's BOJ decision may end up being far more about the future pace of QT than a hike that’s largely factored in.

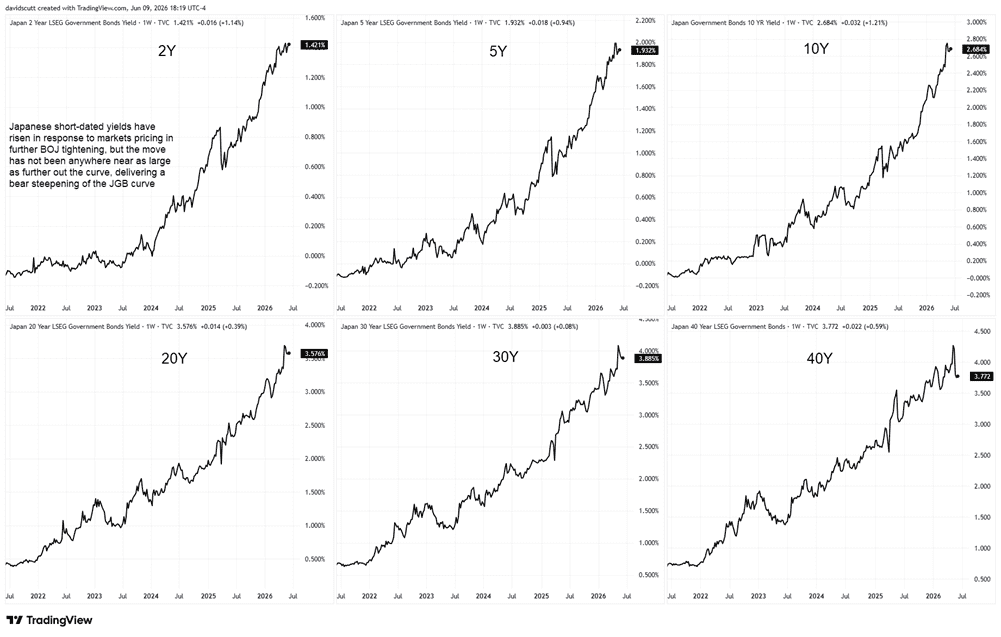

What the JGB Curve Is Really Saying

Source: TradingView

Front end JGB yields have continued moving higher as markets price further BOJ tightening, but not to the extent one might expect given inflation has spent years running above target once temporary subsidies are removed. Instead, it remains anchored by the view that the BOJ will likely proceed cautiously, increasing the risk it may fall behind the curve.

That's why back-end yields have backed up so dramatically. Investors are already demanding greater compensation to hold longer-dated Japanese government debt, lifting term premia to reflect what they perceive to be growing fiscal, inflation and geopolitical risks. In effect, the market is saying it wants the BOJ to do more to minimise those risks than it expects policymakers will be prepared to deliver.

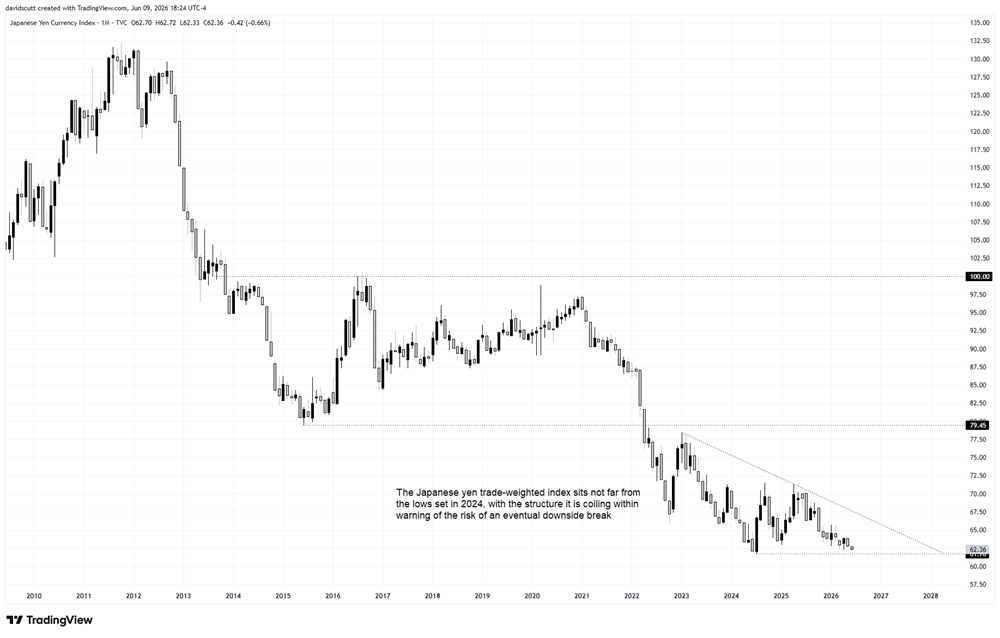

Compensation Through the Currency

Source: TradingView

If that compensation isn't delivered through higher rates and yields, it may have to come elsewhere. Despite record intervention from Japanese authorities, swings in energy prices and bouts of broader market volatility, the persistent trend has been yen weakness.

If investors don't believe the BOJ will deliver sufficient compensation to offset the risks they see building, one way of making Japanese assets more appealing is through a cheaper currency.

Intervention Hasn't Changed the Trend

The price action on the daily USD/JPY chart speaks for itself, with the pair grinding higher in another uptrend after a record amount of intervention from the MoF only slowed the ascent rather than reversing it. Just look at the sequential run of higher lows over recent weeks, with lengthy lower wicks underlining that bulls remain in control, ramming the price higher whenever there's even the slightest dip.

Source: TradingView

Energy prices may be lower and the threat of intervention remains, but that has barely mattered judging by the price action. Upside momentum is building, as demonstrated by RSI (14), which continues to drift higher above 50 without yet entering overbought territory. The constructive message for bulls is complemented by MACD, which has already crossed above the signal line before moving back into positive territory.

The recovery in both indicators and the price underlines that the MoF instructing the BOJ to intervene against yen weakness merely handed bulls better levels to buy. For now, they'll be eyeing a retest of the 2026 high at 160.73. Should that give way, attention will naturally shift to the 2024 multi-year high at 161.95.

On the downside, buyers have repeatedly emerged on dips below 160 down towards 158.80, making that the zone to watch immediately. If it were to give way, the May uptrend and 50-day moving average would present the next hurdles to sustained downside.

The US inflation reports are important, but unless the underlying message materially shifts a Fed outlook that now has markets pricing close to two full rate hikes over the next year, it's doubtful either will spark meaningful downside in USD/JPY. If anything, the risks may be skewed the other way. Should the data suggest second-round inflation effects from higher energy prices are beginning to emerge in areas such as core services ex-housing, it could turbocharge the dollar, amplifying yen vulnerabilities ahead of next week's Fed and BOJ meetings.