Positioning data shows traders leaning into AUD strength, rebuilding CAD longs and pressing GBP shorts ahead of the BoE. USD exposure remains elevated, while NZD continues to lag with persistent net-short positioning.

View related analysis:

- US Dollar Outlook: Bullish May Seasonality Meets Volatility Risk

- Japanese Yen Intervention: Volatility Fades, But Turning Points Emerge

- FX Futures Positioning: US Dollar, EUR, JPY, CAD | COT report

- Australian Dollar Outlook: AUD/USD Bulls Eye Breakout as CPI and FOMC Loom

COT report outlook for USD, USD/JPY, GBP/USD and AUD/USD futures positioning

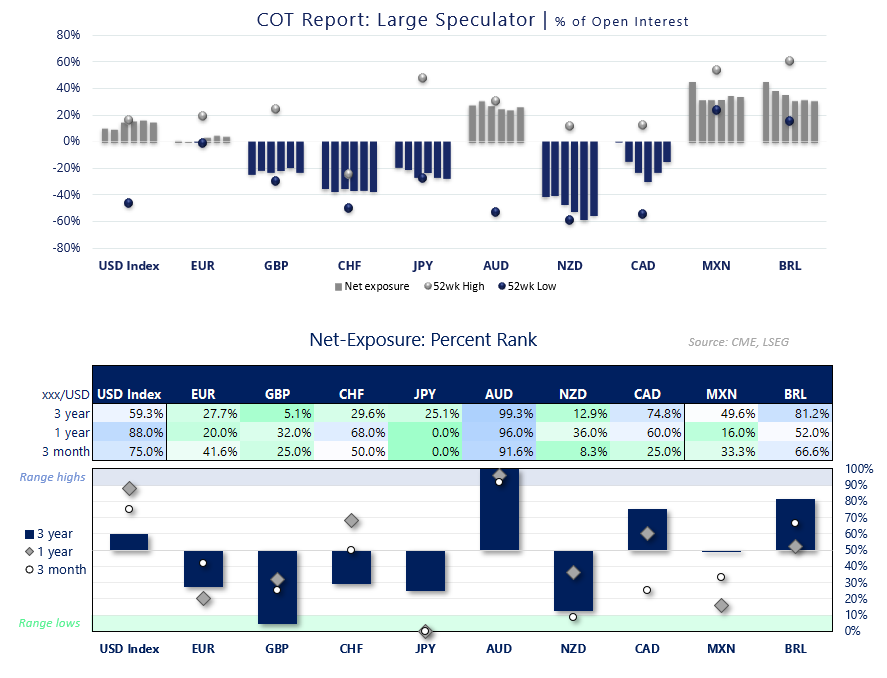

Large Speculator Positioning from the COT report

Source: CFTC (COT), LSEG

- US Dollar: Net-long exposure to the USD futures market was $11 billion, effectively flat from the prior week

- EUR/USD: Asset managers increased net-long exposure to a 6-week high

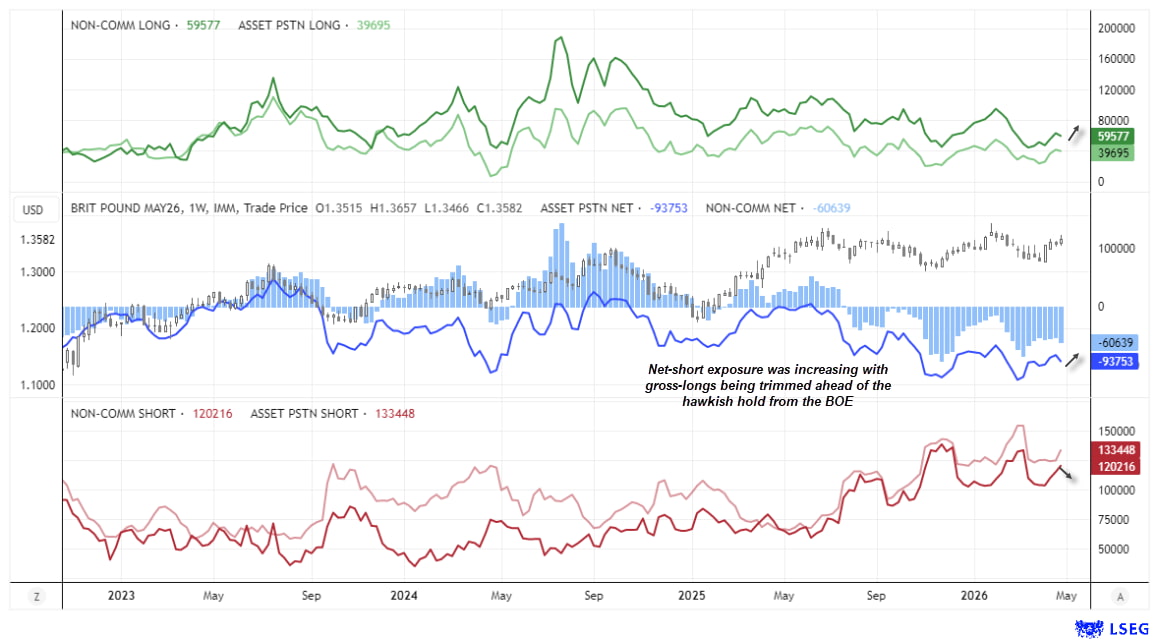

- GBP/USD: Net-short exposure to British pound futures increased by a combined 19k contracts among marge speculators and asset managers

- USD/JPY: Large speculators were their most bearish on Japanese yen futures since July 2024, and asset managers by November 2024

- USD/CHF: Swiss franc net-short exposure rose to a 7-week high among large speculators

- USD/CAD: Asset managers flipped to net-long Canadian dollar futures long exposure for the first week in four

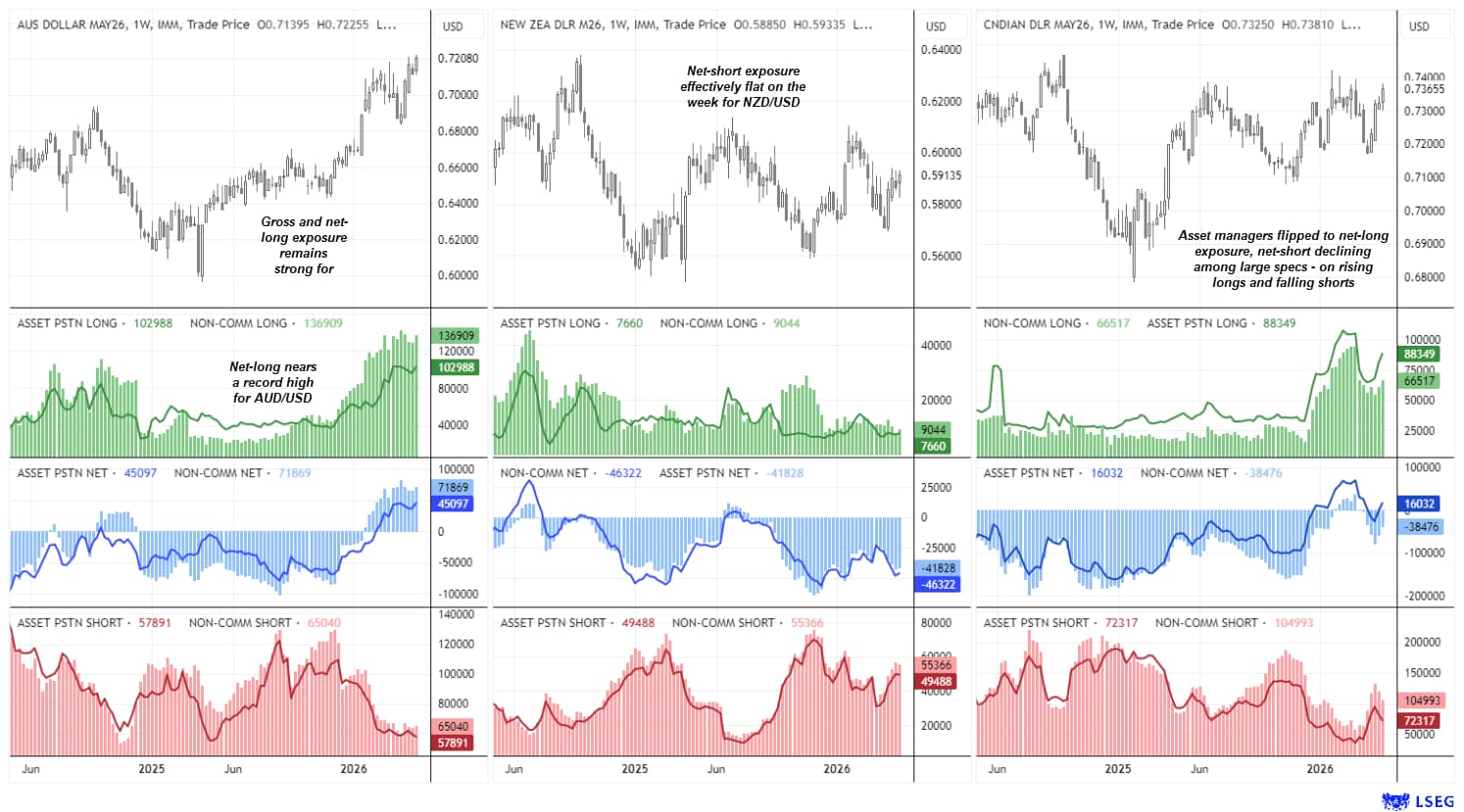

- AUD/USD: Asset managers nudged their net-long exposure to just below a record high, rose for first week in thee among large specs

- NZD/USD: Net-short exposure was trimmed marginally by -2.8k contracts among both sets of traders

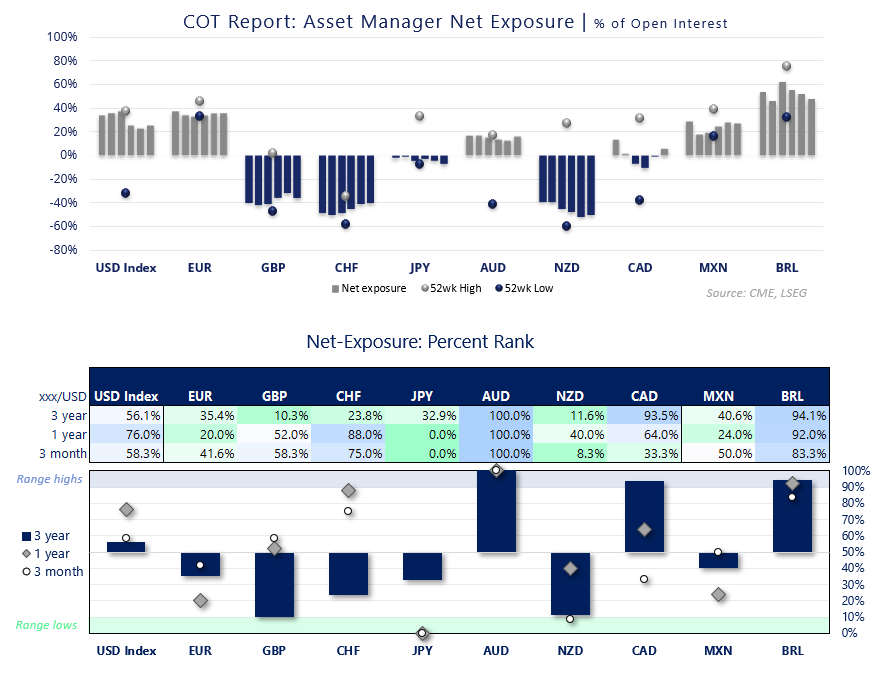

Asset Manager Positioning | COT Report

Source: CFTC (COT), LSEG

FX Futures Positioning | COT Report (IMM Data)

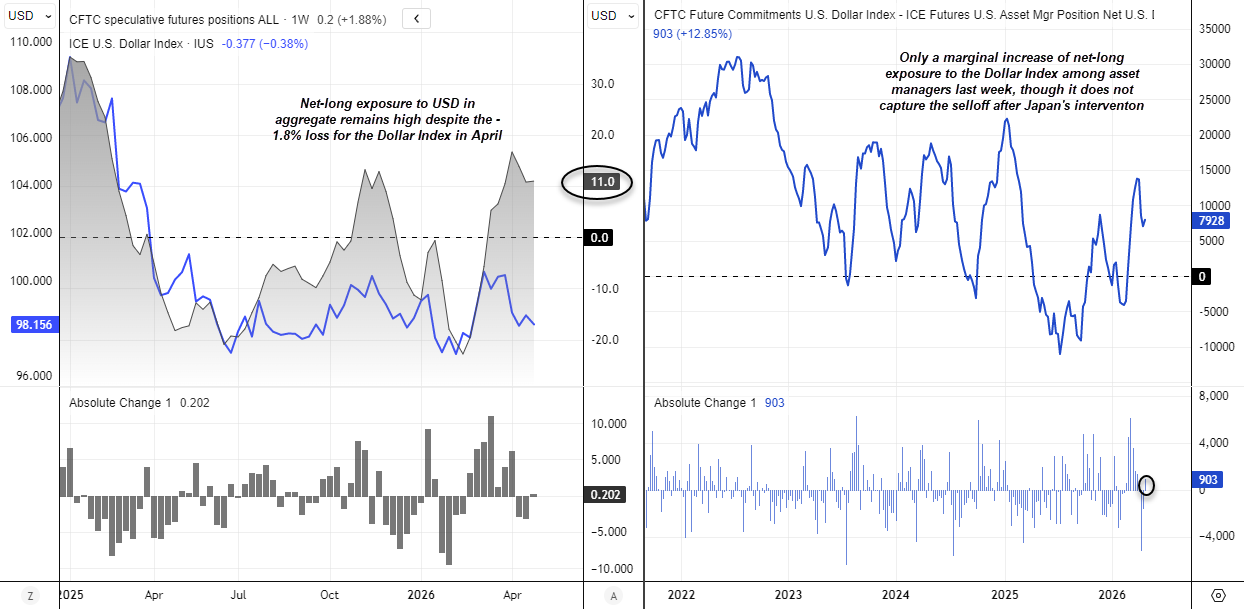

US Dollar Index (DXY) Futures Positioning | COT Report

The US dollar index fell -1.8% in May, broadly in line with its typical seasonal weakness, although slightly shy of the -2.2% average decline since 2000. Despite this, net-long positioning remains elevated, with futures traders holding around $11 billion in net-long USD exposure.

Asset managers also added to bullish bets, increasing net-long exposure by 900 contracts. While positioning was relatively unchanged on the week, it’s worth noting the data does not yet reflect the selloff triggered by Japan’s Ministry of Finance (MOF) intervention.

Even so, with the Fed unlikely to cut rates and the Strait of Hormuz still closed, downside for the US dollar may remain limited in the near term without a shift in the macro backdrop.

Source: CFTC (COT), ICE, LSEG

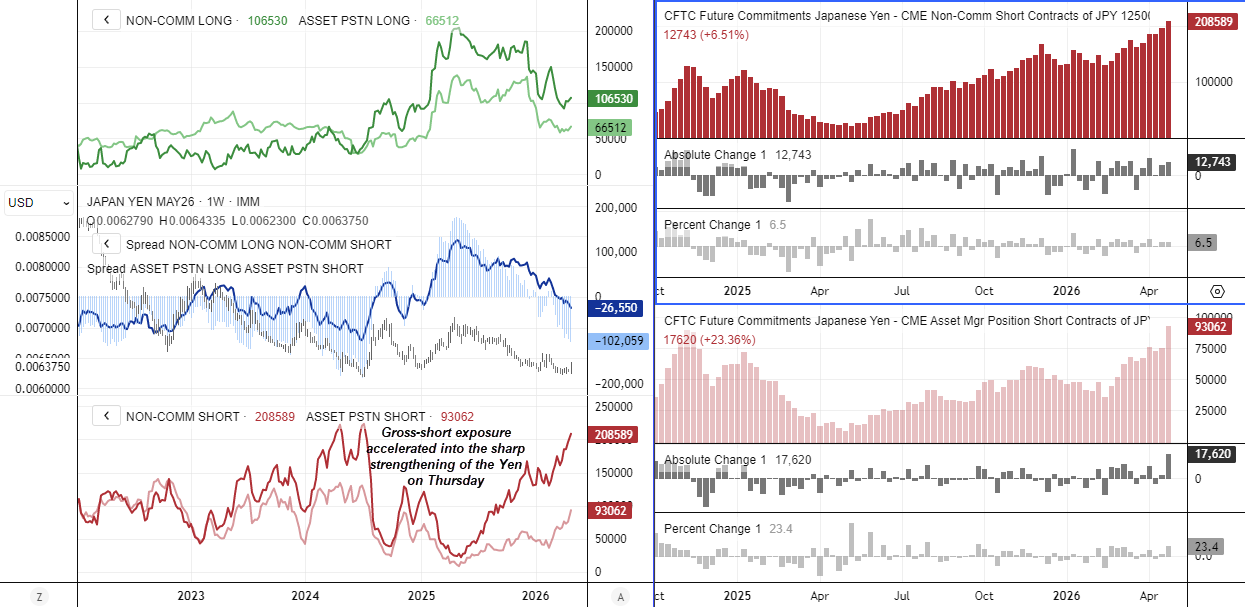

USD/JPY Futures Positioning | COT Report

Yen bears may have been caught off guard as Japan’s MOF reportedly intervened in the currency market. Gross long positioning had already been trending higher among large speculators and asset managers (bottom left), before they added a further 30.3k contracts of bearish exposure ahead of Thursday’s volatile move.

At this stage, whether intervention is officially confirmed or not matters less than the outcome — a sharp yen appreciation that likely triggered a wave of stops.

Analysis of previous yen interventions suggests USD/JPY may have formed a near-term top, with downside risks persisting for several weeks, if not months, based on historical patterns. It’s also worth noting that gross longs have picked up in recent weeks, while the Bank of Japan (BOJ) has begun to adopt a more hawkish tone.

Source: CFTC (COT), CME, LSEG

GBP/USD Futures Positioning | COT Report

Net-short exposure to British pound futures rose ahead of Thursday’s Bank of England (BoE) meeting. A combination of rising gross shorts and trimmed longs across both trader groups lifted net-short exposure by nearly 20k contracts—noticeable, but not extreme.

However, a hawkish hold from the BoE—where policymakers warned rates may still need to rise—and a lone dissent from the Chief Economist calling for a hike to 4%, helped push GBP/USD to a 10-week high by Friday’s close.

We may therefore see at least a partial reversal of these short bets, alongside a pickup in long positioning in next week’s report.

Source: CFTC (COT), CME, LSEG

Commodity FX Futures Positioning (AUD, CAD, NZD) | COT Report

The broader theme points to improving sentiment towards commodity FX—aside from the New Zealand dollar. Asset managers nudged net-long exposure in AUD futures to just shy of a record high, with gross longs rising by 8.5k and shorts trimmed by 1.6k. Combined with large speculators, net-long exposure increased by 15.5k contracts. This keeps the bullish AUD/USD narrative intact, and a breakout may not be far off.

Canadian dollar futures flipped back to net-long exposure after four weeks of net-short positioning. Here, the structure looks cleaner, with rising longs alongside falling shorts—supporting a bearish USD/CAD outlook.

NZD/USD futures remain heavily net-short, although week-on-week changes offer little in terms of directional conviction for the New Zealand dollar.

Source: CFTC (COT), CME, LSEG

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade