COT positioning suggests a shift is underway in FX markets. While the US dollar’s rally shows signs of topping, traders are rotating into EUR and GBP, with commodity currencies lagging despite recent strength. The latest futures data highlights a divergence between price action and positioning, raising questions over whether the next move is continuation—or correction.

View related analysis:

- US Dollar Index Outlook: Bullish Bounce Overshadowed by Major Top Risk

- AUD/USD Outlook: Pullback Below 0.72 Underway as Geopolitical Risks Intensify

- British Pound Price Action Setup: GBP/USD, EUR/GBP, GBP/JPY

- Japanese Yen Price Action Setups: USD/JPY, AUD/JPY, CHF/JPY

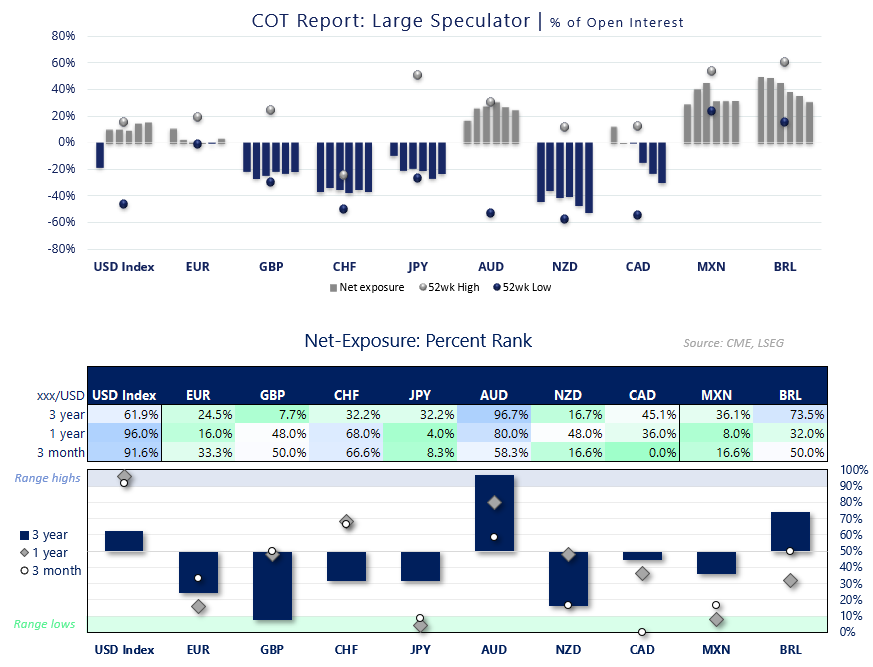

COT Report: USD Positioning Peaks as EUR and GBP Strengthen

Large Speculator Positioning from the COT report

Source: CFTC (COT), LSEG

- US Dollar: Aggregate exposure to the US dollar declined by -$2.8 billion last week to $13.9 billion, while asset managers reduced their net-long exposure to the USD Index by -5.1k contracts.

- EUR/USD: Large speculators flipped to a net-long position of 26k contracts, after a one-week stint net-short.

- GBP/USD: While British pound futures traders remained heavily net-short, asset managers increased their gross-long exposure by 40.1% (+10.4k contracts).

- USD/JPY: Futures traders remained net-short Japanese yen, although large speculators reduced their exposure by -10.5k contracts, driven by an 11.5% increase in gross longs.

- USD/CHF: Net-short exposure to the Swiss franc rose to a five-week high among large speculators, though it was effectively flat on the week among asset managers.

- USD/CAD: Large speculators increased net-short exposure to Canadian dollar futures for a fourth consecutive week, reaching a 17-week high as traders continued to favour the US dollar over commodity FX.

- AUD/USD: Net-long exposure dipped for a second week among large speculators and a third week among asset managers, although the Australian dollar went on to print a near four-year high and test 0.72 by Friday.

- NZD/USD: Net-short exposure rose to an 11-week high among both groups of traders, increasing by a combined +11k contracts on the week.

Asset Manager Positioning | COT Report

Source: CFTC (COT), LSEG

FX Futures Positioning | COT Report (IMM Data)

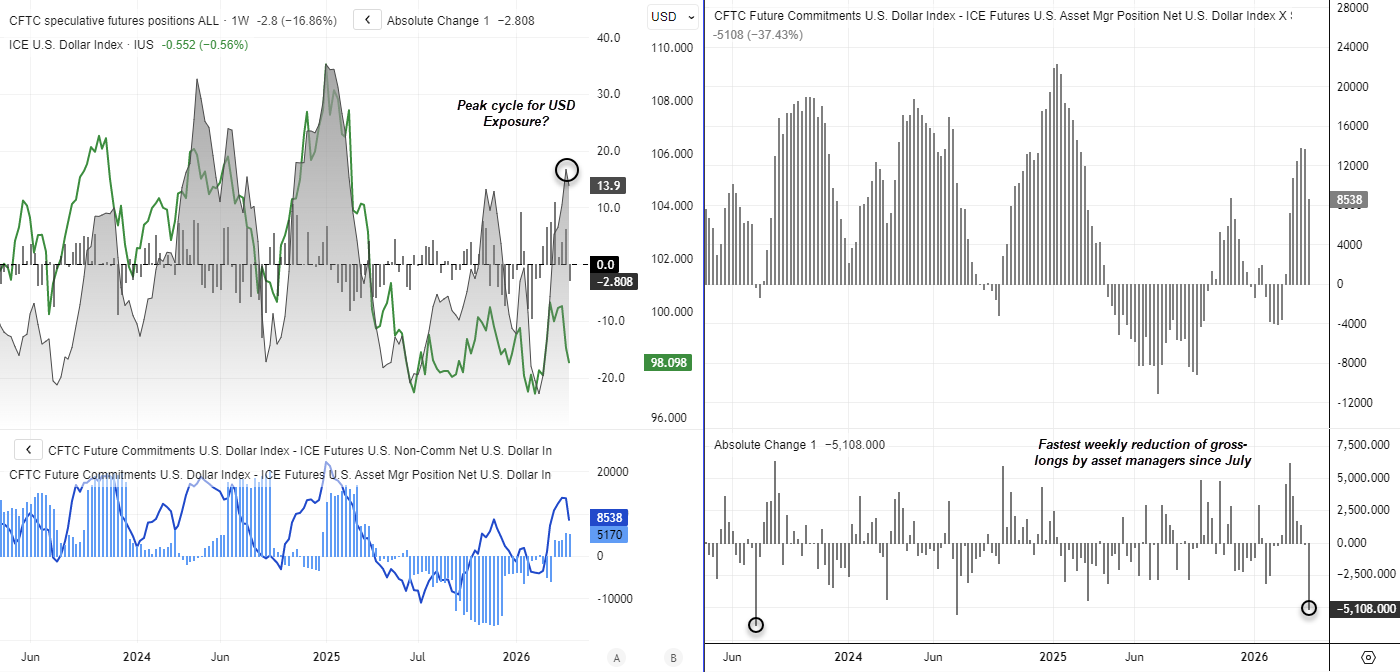

US Dollar Index (DXY) Futures Positioning | COT Report

While the -$2.8 billion reduction in aggregate US dollar exposure last week is not large, it could still prove significant. I have previously outlined my bias that the US dollar rally likely topped on 31 March. And with net-long exposure rising to a one-year high of $16.7 billion the week prior—despite the US dollar index falling for a third consecutive week—I suspect we’ve already seen a sentiment peak in dollar longs.

Of course, developments in the Middle East remain a key driver. A resolution—particularly one that sees the Strait of Hormuz reopened—would likely allow the US dollar to continue its decline. So while there are risks of a near-term bounce for the USD, I maintain the view that an important high formed in late March and that further losses lie ahead.

Note that asset managers reduced their net-long exposure by -5.1k contracts, marking their fastest weekly reduction since July. While net-long exposure among large speculators was unchanged, it remains subdued at just 5.2k contracts.

Source: CFTC (COT), ICE, LSEG

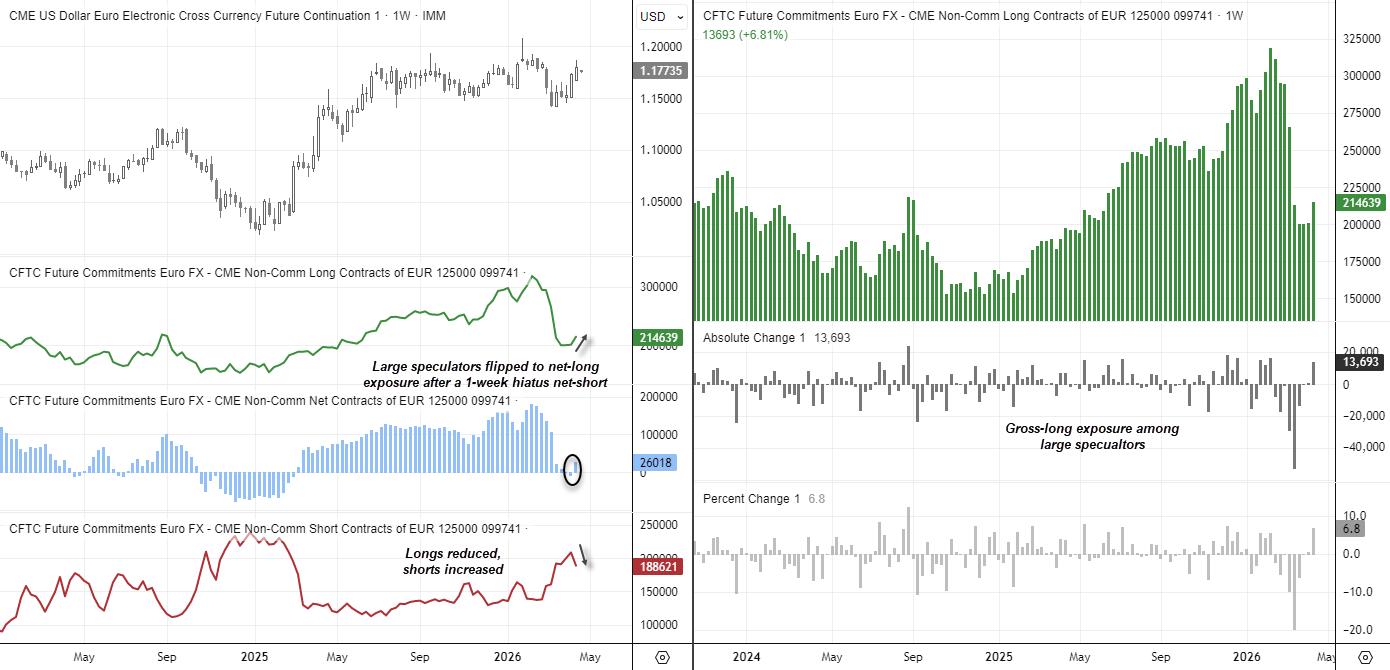

EUR/USD Futures Positioning | COT Report

The surge into euro longs alongside a reduction in net-long USD exposure in the same week strengthens the case for a top in the US dollar and a likely low for EUR/USD. That said, Middle East developments will remain the key driver in determining whether this view holds.

Large speculators flipped back to a net-long position last week after a one-week stint net-short. Both sides of the ledger supported the move, with longs increasing and shorts being reduced. Gross longs rose by 13.7k contracts (6.8%).

Source: CFTC (COT), CME, LSEG

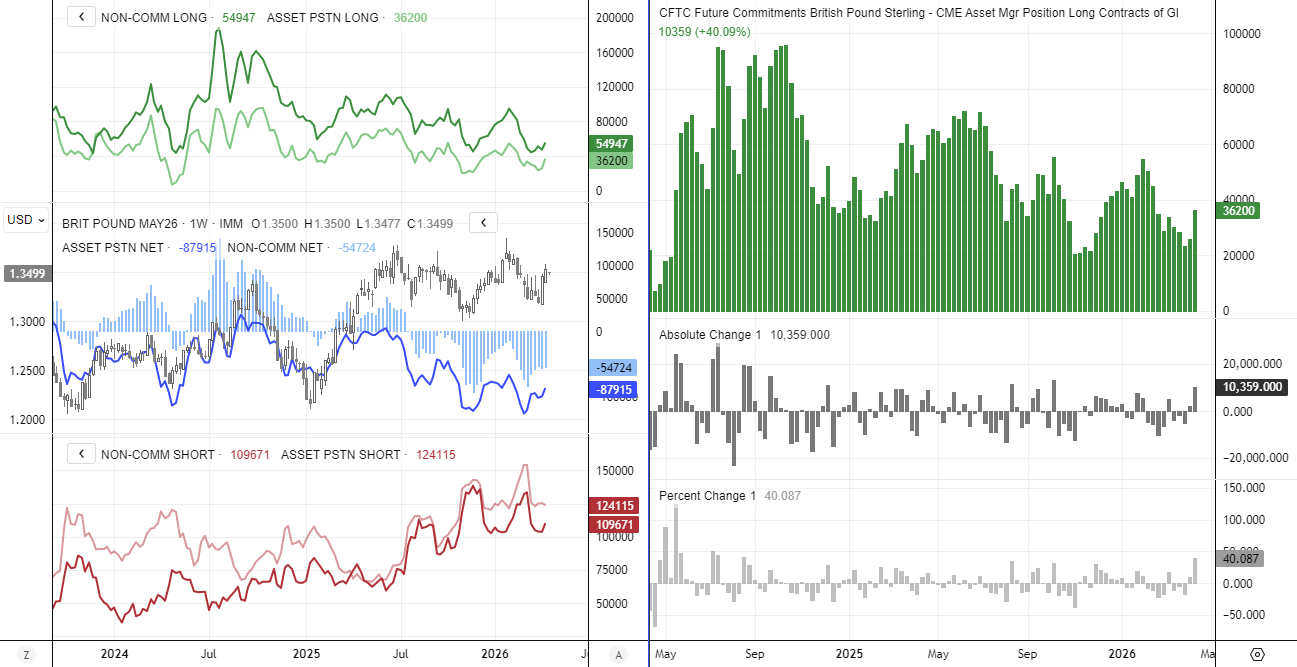

GBP/USD Futures Positioning | COT Report

The standout development for the British pound is that asset managers increased their gross-long exposure by 40.1% (+10.4k contracts). It marks the fastest increase in longs since July 2024, and the largest rise in absolute terms in six months.

This helped reduce net-short exposure to GBP/USD futures to an eight-week low among asset managers. Futures prices then rose for a second consecutive week, reaching an eight-week high.

Source: CFTC (COT), CME, LSEG

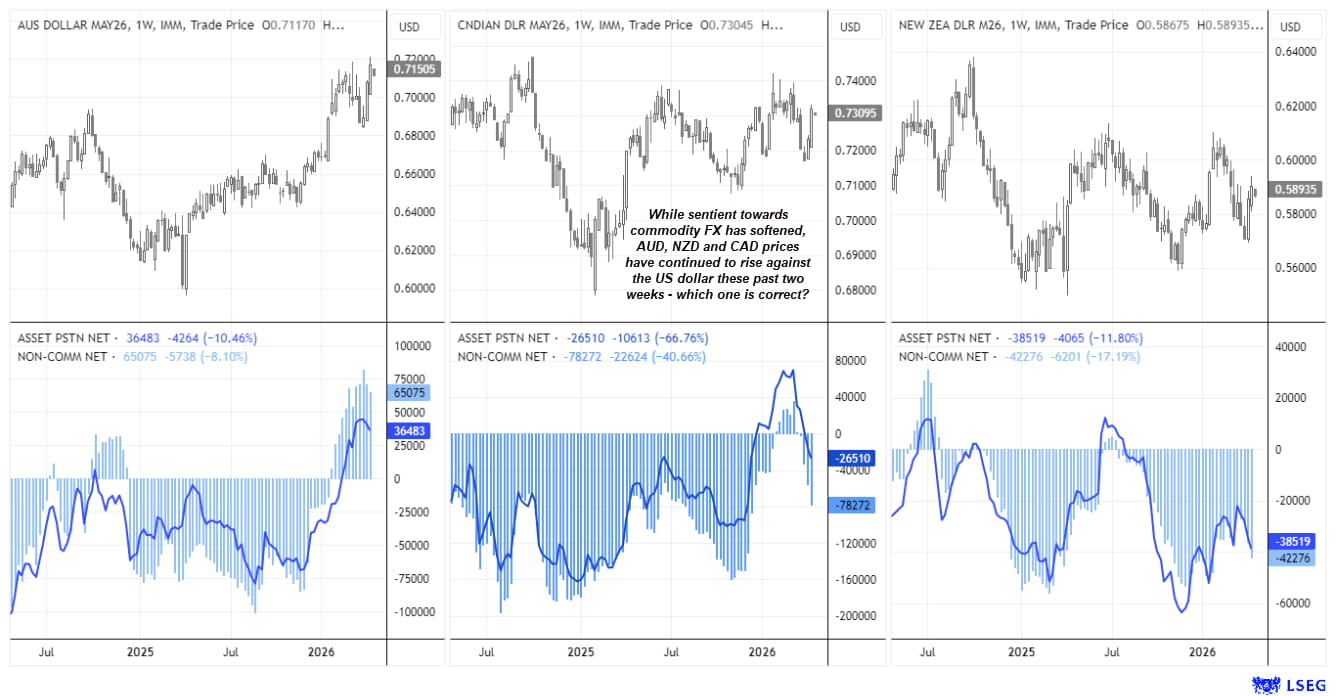

AUD/USD, USD/CAD, NZD/USD Futures Positioning | COT Report

Bets that the worst of the conflict is behind us have helped commodity currencies rally against the US dollar over the past two weeks. Yet market positioning has not fully supported the move.

- Net-long exposure to the Australian dollar declined for a second week among large speculators and a third week among asset managers.

- Net-short exposure to the Canadian dollar rose to a 17-week high among both groups of traders.

- Net-short exposure to the New Zealand dollar also increased for a fourth consecutive week among large speculators and asset managers.

If the conflict persists, it suggests positioning may be correct and that spot prices could come under pressure. However, as noted above, I remain cautiously optimistic that the worst may be behind us—even if the resolution is drawn out. That scenario could help sustain a ‘buy the dip’ mentality for risk and, by extension, AUD, CAD and NZD.

Source: CFTC (COT), CME, LSEG

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

How to trade with City Index

You can trade with City Index by following these four easy steps:

- Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade